Live preview mode. Wire is not yet published.

Assessing the sovereign risk of Australia vs USA

Greg Goodsell, Global Equity Strategist at 4 Dimensions Infrastructure, compares the sovereign risk of investing in Australia versus the United States.

4 Dimensions is a Bennelong Funds Management boutique.

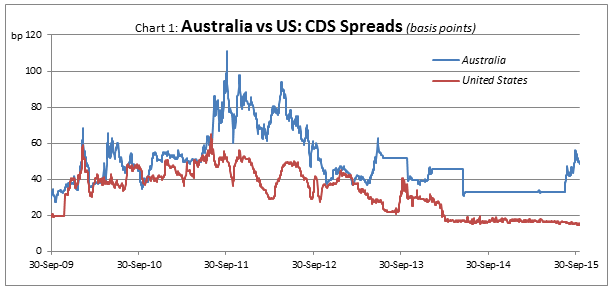

Australia and the US remain attractive investment destinations

Australia and the USA remain stable, attractive investment destinations. The low EIU political risk scores reflect established, long lived, effective democracies. The CDS spreads suggest credit markets are comfortable with each nation’s sovereign risk, and that the market remains open and receptive to further debt issuance by each country.

Nevertheless the deterioration in Australia’s CDS spread is a concern and is something to continue to monitor. It is currently around 48bp, but was as low as 32bp back in August 2015. This compares with an average CDS spread for the other five AAA rated sovereigns with CDS markets of around 16bp. The spread deterioration may reflect the unstable political environment that has gripped Australia over the past few months, and the inability to deliver effective fiscal management. The deterioration could also reflect concerns regarding the economic slowdown in China and its possible impact on a large commodity exporter like Australia.

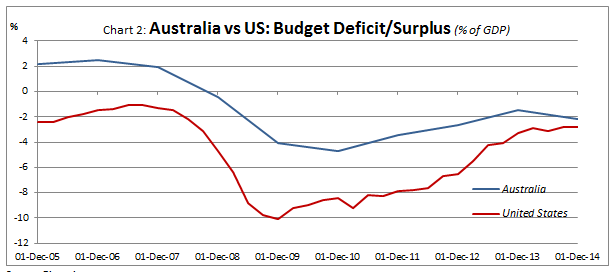

Both countries show improved fiscal positions

Both fiscal positions show improvement but reflect long running, somewhat structural, deficits. In the case of Australia the deficits reflect an inability to move the budget to balance, or even surplus, during a period of unprecedented mining sector wealth (and tax revenue) generation. A significant missed opportunity

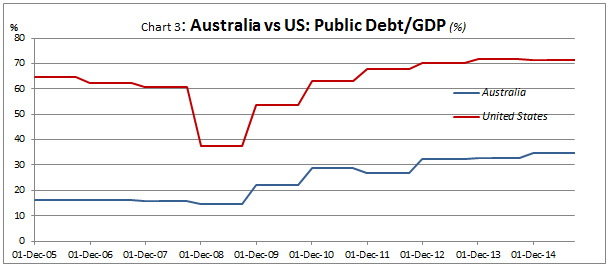

Australia enjoys a lower level of public debt, but it is rising rapidly

The public debt/GDP positions are quite different with the US at 71% (arguably 100%+ if you include all public debt on issue). The Australian position, at 35% and climbing, reflects the strong financial legacy left by the Howard government (of $0 net public debt in 2006) combined with poor fiscal discipline since.

Global deflation would be unwelcome

More broadly, and more importantly, the large and growing debt positions reflect the need for policy makers to engineer some global inflation, and work very very hard to avoid deflation. Deflation not only acts as a deterrent to current expenditure (as it encourages spending tomorrow, rather than today - as everything will be cheaper tomorrow) but, as nominal GDP could be falling (or at least growing more slowly) the debt service burden, as a percentage of GDP, can become larger. Conversely, inflation helps to reduce the debt burden as the debt is mostly fixed interest, and hence nominal in nature. As GDP grows, outstanding debt as a % of GDP declines, as does the servicing obligation.

Sovereign debt levels are a global issue

The growing sovereign debt burdens exhibited by Australia and the US are not unique. A feature of the post GFC world is that, while many countries are making very credible and successful efforts to get their economies up and growing again and reducing unemployment, many retain substantial residual sovereign debt burdens. The country list is topped by Japan at a Public Debt/GDP ratio of almost 230%.

General level of sovereign indebtedness globally are a concern, particularly in a low inflation/potentially deflationary environment.

For the full article click the (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bennelong Funds Management develops and distributes active funds locally and around the globe, offering high-grade investment solutions to institutions, financial advisers and direct investors.

1 topic

Fund Manager

Bennelong Funds Management develops and distributes active funds locally and around the globe, offering high-grade investment solutions to institutions, financial advisers and direct investors.

Expertise

No areas of expertise

Fund Manager

Bennelong Funds Management develops and distributes active funds locally and around the globe, offering high-grade investment solutions to institutions, financial advisers and direct investors.

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment