Live preview mode. Wire is not yet published.

Give investors what they want

•

Sponsored

Print Wire

When Jeff Bezos launched Amazon as a one-man operation from his garage in 1995, part of his mission statement was to be “Earth’s most customer-centric company.” A quarter-century later, it seems like his obsession over the needs of the customer may have been a smart business strategy.

Most investment products unfortunately put the business first, not the customer. Funds typically design products to be scalable, cheap to run, and easy to sell - because this drives margins for the business.

In stark contrast, we have tailored Lucerne Alternative Investments Fund (LAIF) specifically to provide what most investors really want for their core portfolio - a prudently and professionally run diversified portfolio that delivers consistent high absolute returns with low risk of large losses.

Delivering on expectations in a tough year

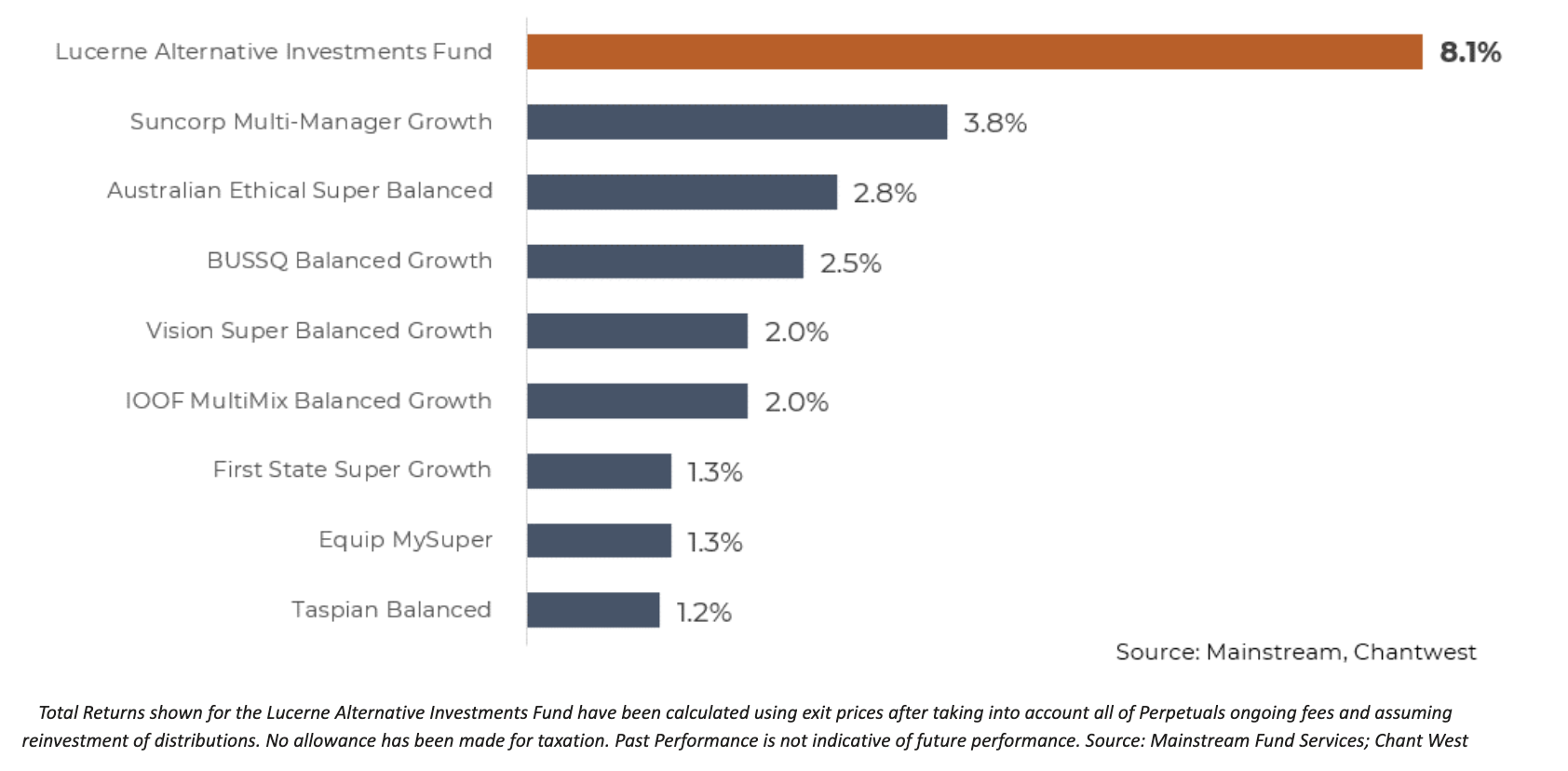

We seek to provide 6% or more above the RBA cash rate. In my first year managing the fund, we delivered 8.1%, thus performing as per expectation and outperforming the market significantly.

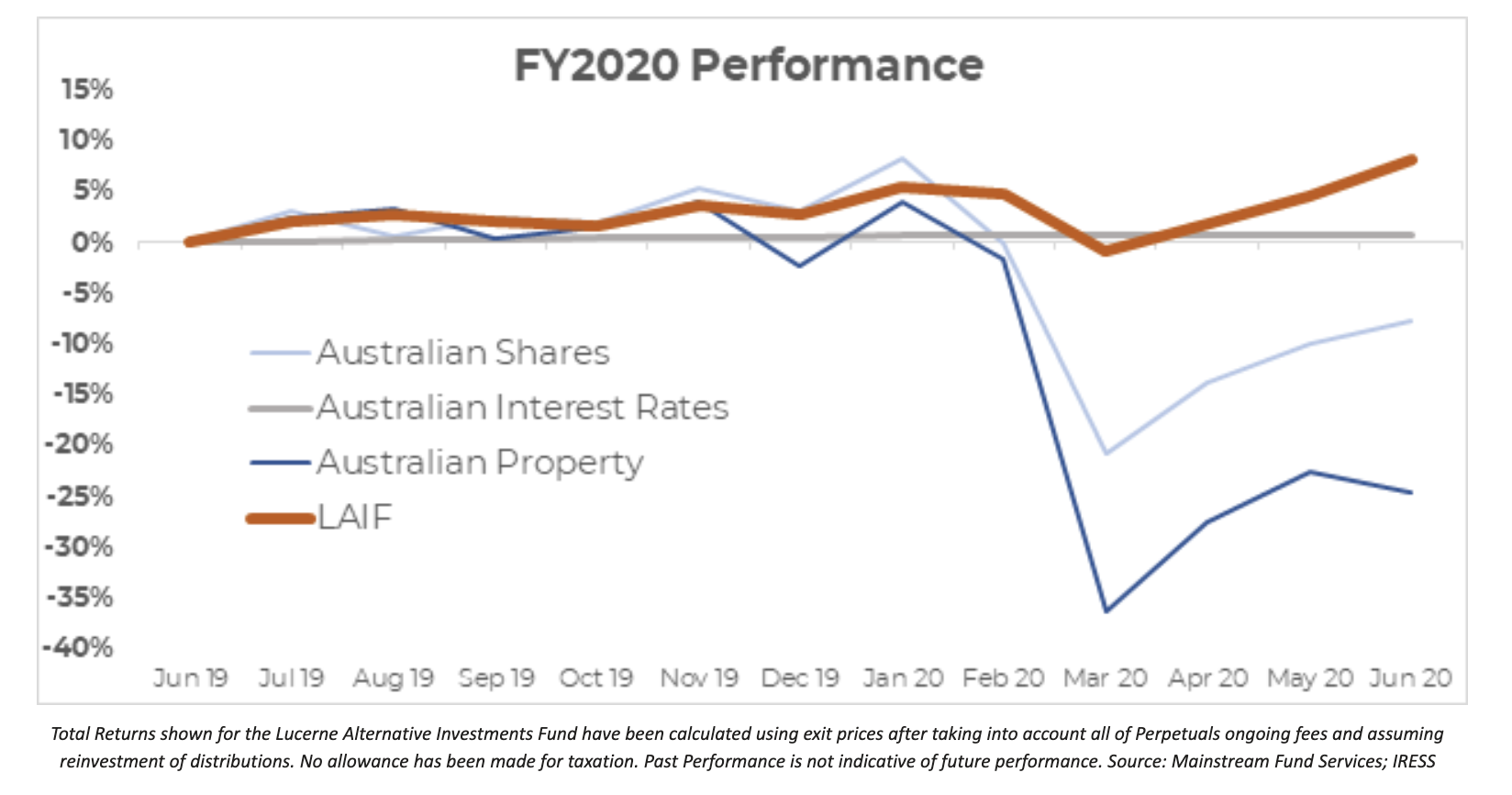

Lucerne Alternative Investments Fund: Up +8.1% in FY20

While super funds are well promoted as being customer-centric, they simply are not, as their recent returns testify. In fact, last year to the best of our knowledge, the Lucerne Alternative Investments Fund outperformed every diversified super fund, in most cases by a very large amount.

LAIF versus some of the super industry’s top performers in FY20

The main role of a super fund is as an investment manager - to grow and protect your assets so that you may live comfortably in retirement. In the financial year just passed, super funds didn’t do this.

Australian super funds are market performers or index trackers who follow the fortunes of markets up and down. Now that markets have become choppier and more challenged, large super funds are demonstrating complacency and status quo bias in their asset allocations, and are unable to change their large illiquid portfolios. Valuations are opaque and not reflective of typical mark-to-market valuations or market pricing mechanisms. Market-based valuations would probably have shown significantly worse returns for last year for many super funds. Returns are lacklustre regardless, even with the opaque valuations.

Protecting investors during down markets

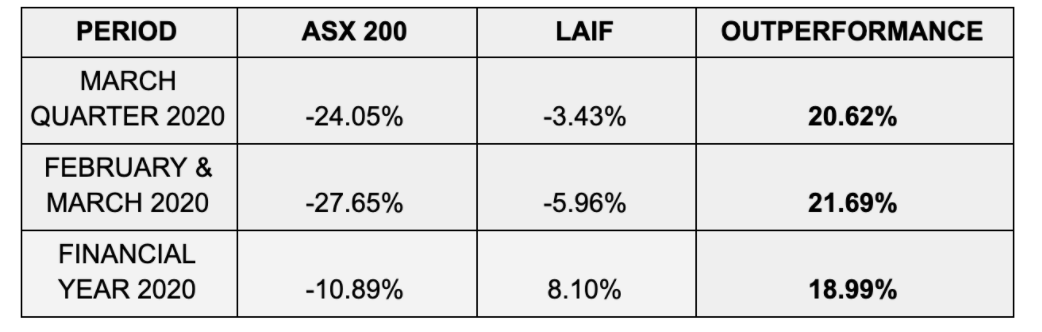

The Australian market experienced its worst quarter since 1987 during the March 2020 quarter. The ASX200 lost 24.05% during this period, nearly a quarter of its value. This kind of severe drawdown, particularly the dramatic fall during the late-February to late-March period, puts investors under extreme psychological stress. Our investors only experienced a fraction of the market’s drawdown, or related stress, seeing a pullback of just 3.43% over the March quarter.

The market crash happened within the February-March period, and taking that two-month period in isolation, the stats tell the same story. LAIF fell by only 5.96%, versus the market falling 27.65% during this time. A relatively small drawdown like this is easy to recover from, whereas a large double-digit loss is not.

LAIF versus the market during the crash and over the financial year

Source: ASX and LAIF performance data

Our decisive active management and asset allocation changes helped investors avoid the vast majority of the fall, with the fund experiencing just a fraction of the sharp pullback. Our superior alpha generation and active management through time have consistently added value to our fund’s investors.

It is exactly this kind of protection from volatility that we sought to achieve for our investors, and the March quarter provided one of history’s greatest ever ‘stress tests’ to demonstrate that the fund can perform true-to-label when required.

We fully expect there to be further challenges and extreme volatility in the near future and LAIF will aim to keep successfully defending investors’ capital, whatever lies ahead.

Active Management is key

Our passionate belief in the role of active management is central to our results. Active management has faced enormous criticism in recent years, as the seemingly inexorable flow of capital into passive funds demonstrates.

But the world is changing rapidly and drastically, and if you’re investing in a strategy that hardly ever changes its positioning, you’re going to suffer. This is sadly what most funds do. They stick with obsolete portfolio theory while the world changes around them, hoping in vain that 20th-century ideas will withstand 21st-century challenges.

While some funds may have slightly trimmed their asset allocations through the March quarter, we massively changed our weightings to our underlying investments through this time. This courage and insight is what is needed to manage the drawdown risk of a portfolio as a whole in response to real-time risks, and maximise prospective return for risk.

We do this with a detailed understanding of markets, of what we were doing, and why we do it. We research and follow markets and their prospects intently, and we identify and manage prospective risk in real-time, on a daily basis.

Give them what they want

Investors can do so much better to manage risk by being more selective and investing with those who are actually good at what they do.

Partnering with investor-centric experts with the right motivations, right skills, and access to opportunities has always made much more sense for developing a product that actually performs.

In this regard, The Future Fund, Australia's sovereign wealth fund, which manages more than $200 billion, is widely seen as Australia’s pre-eminent investor.

The fund has a far superior investment approach to large super funds. It has access to the world’s best thinking offshore and other large institutions and significant internal investment talent. Its genuine diversification, superior risk management, and active asset allocation approach are similar to our thinking and portfolio construction.

In short, the Future Fund is so much better than super funds in every way. All Australian investors deserve and have waited a long time to have direct access to something like it. We want to let these people know that the Lucerne Alternative Investments Fund (LAIF) exists and unlike the Future Fund, the market can actually invest with us.

The 8.1% gain that LAIF generated in the most challenging of markets, during my first year managing the fund, hasn’t been a happy accident. It is the culmination of 20 years of industry experience, including serving as CIO of a conservatively managed $12 billion insurance fund with outstanding results.

I expect markets to present more volatility and challenges in FY21 and beyond. I look forward to continuing to manage these risks and giving our investors more of what they want: consistent high absolute returns with low risk of large losses.

We value integrity, care, excellence and doing things differently

At Lucerne Investment Partners we take an investment approach focused on low volatility and low correlation to stock markets, with capital preservation top of mind. Click 'CONTACT' to learn more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's more challenging investment environment. Jerome has achieved net returns for clients of around 20% in both the challenging 2020 year and in 2021, with much lower drawdowns and volatility than Australian equities and hence much superior risk adjusted returns. His Wealthlander Diversified Alternative fund targets double digit returns annually for wholesale clients, with lower volatility and greater consistency than Australian equities, using a diversified multi-asset portfolio approach.

........

This has been prepared by Lucerne Australia Pty Ltd ACN 609 346 581 a Corporate Authorised Representative of AFSL number 481 217 and issued by The Trust Company (RE Services) Limited ACN 003 278 831 as responsible entity and the issuer of units in the Lucerne Alternative Investments Fund. It is general information only and is not intended to provide you with financial advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider the product disclosure statement, available by calling 03 8560 1440 or visiting our website (VIEW LINK), prior to making any investment decisions. If you require financial advice that takes into account your personal objectives, financial situation or needs, you should consult your licensed or authorised financial adviser. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. No company in the Perpetual Group (Perpetual Limited ABN 86 000 431 827 and its subsidiaries) guarantees the performance of any fund or the return of an investor’s capital.

2 topics

1 contributor mentioned

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Comments

Comments

Sign In or Join Free to comment