3 mistakes to avoid when picking a fundie

There has rarely been a more urgent time to assess whether your money is being optimally managed. Market valuations are close to all-time highs while risk levels are high and long-term real return prospects are near zero. We anticipate re-runs of 2020 over the coming years, with more volatility and markets that ultimately go nowhere.

One option for investors in this highly fraught environment is to outsource part, or all, of the responsibility for managing money to experienced fund managers aligned with their needs. This is a critically important process, so in this wire, we discuss a few of the most commonly made mistakes when picking a fundie to improve your chances of getting it right. This may help you turn a potential headache and otherwise mediocre results into long-term investing success.

Mistake #1: Ignoring the massive changes in market conditions and return prospects

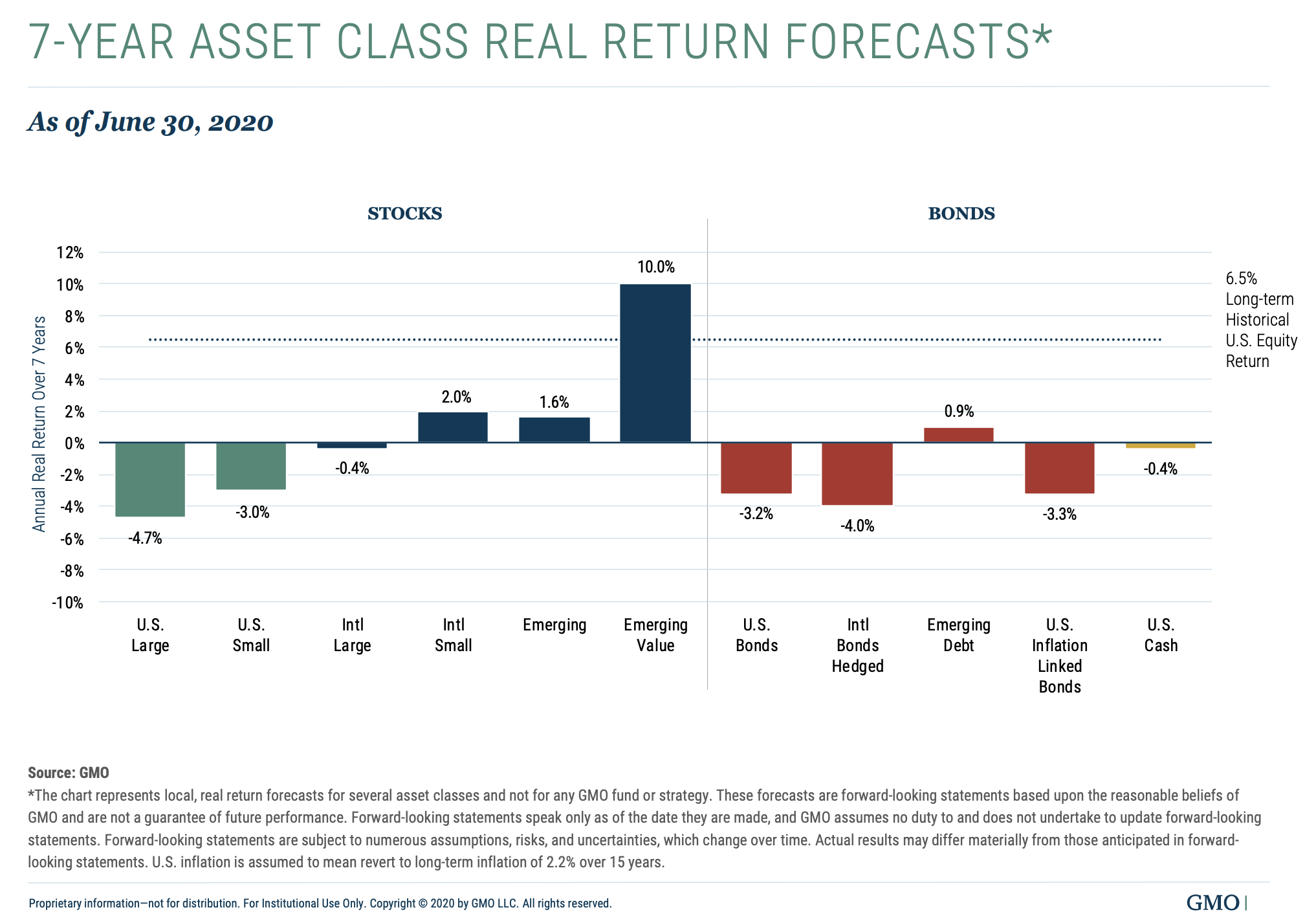

These are not normal times. All asset prices are inflated. Highly credible and previously meaningful forecasts demonstrate that the likely multi-year real return from most mainstream assets is around zero. GMO’s most recent seven-year asset class price forecast, for example, illustrates this below.

John P. Hussman, Ph.D., President of Hussman Investment Trust also recently discussed this in a letter to investors, saying that:

“... investors should be fully prepared for a decade of zero stock market returns.”

Meanwhile, risk is very high, and the chances of multiple repeated crises in the coming months and years causing significant market falls are also higher than usual.

The risk of a massive change in the investment environment is imminent while near-zero bond rates and inflation have been imputed into market prices ‘forever’, yet a vaccine or vaccines, better testing, and changing government policies are likely to greatly influence the market tenor in coming months and years. The current starting point, therefore, provides a dismal risk and return outlook for investors relying upon traditional passive (or quasi-passive) exposures to cash, bonds, property, and equities to make them real gains.

Yet, most advisers and investment managers continue to build portfolios as if it were the 1980s or 1990s when interest rates were much higher and equity return prospects were very strong. This approach ignores the growing possibilities of deflation, inflation, or stagflation, and how devastating these may be for portfolios going forward. We can already see the mainstream results that come from sticking to ‘the old ways’; big drawdowns and very low overall returns when compounded over time. Without change, more of the same results should be expected. It is hence crucial that any fundie you choose has adapted to the new realities of markets.

The rising tide which lifted all asset prices, investment managers, and advisers is receding fast. The need to be thoughtfully different, to adopt non-consensus views, and to be well-researched is now essential. It seems clear that a different type of portfolio and portfolio management is required compared to what has been used in the past.

I suggest being more selective when choosing investments by prioritising value-adding exposures alone, being more dynamic and more active with portfolio management, and being more risk-conscious and intolerant of under-performers to avoid large downside risks. You also need to incorporate much greater use of (good) liquid alternatives with different risk exposures in a portfolio and be willing to allocate selectively to non-mainstream assets which are carefully selected and managed. Greater value-add from the portfolio as a whole through sophisticated portfolio construction and asset allocation (e.g. making substantive weighting changes in response to ever-changing prospects) needs to be adopted. Of course, selecting good investment managers, to begin with, is a very good start.

Furthermore, you need to have all of these things working for you to maximise the probability of success!

Mistake #2: Picking a manager based on recent performance - rather than picking them based on their alignment with your own investment goals

We all like to back a winner, and past performance is therefore one of the biggest drivers of new capital into a fund. Unfortunately, fund performance is routinely cyclical, and a strong patch in individual strategies is often followed by much weaker performance.

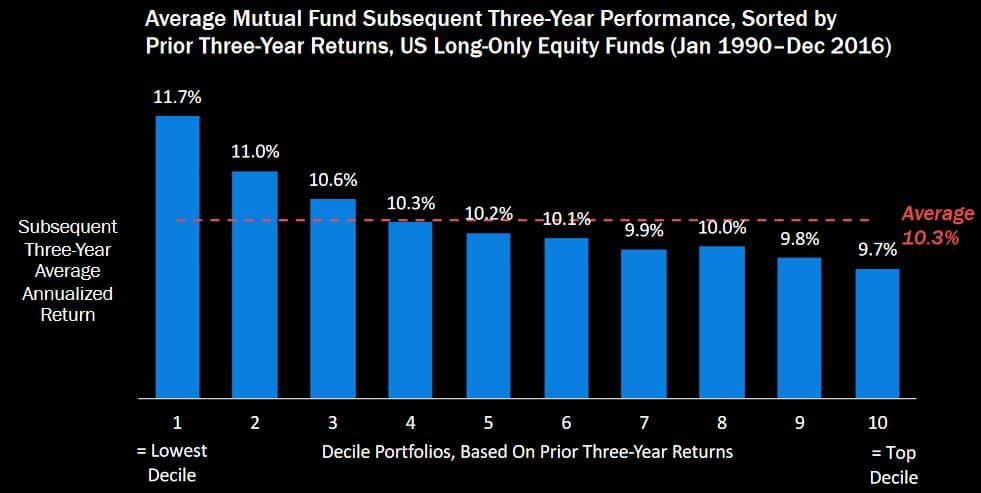

The table below from Research Affiliates reviews nearly three decades of US managed funds data collected by Morningstar and essentially shows that on average the worst-performing funds over a three-year period, subsequently outperformed over the next three years. The opposite is true as well, with the top-performers going on to become the underperformers.

Source: Research Affiliates

Source: Research AffiliatesSo by being overly focused on the past performance of individual strategies and funds, investors may be routinely setting themselves up for disappointment.

It is unfortunately much easier to market something that has just performed strongly as most people are attracted to what’s working today. So, effectively, investor biases and industry dynamics both make it easy for investors to buy a fund high, only to later sell it low.

If you've fallen into this trap, then it is really important to be honest with yourself, and work out how to actively mitigate the dangers. This is your money, so think about what you want for it. Do you want to be invested in overly-crowded assets and strategies that have already had their run and are now being sold to you because they’re yesterday’s best-performer?

Or do you want to invest in strategies that have every chance of doing well over the years to come, are in alignment with your goals and objectives, and are being managed by those with the same philosophy? If you are falling for the past performance trap, a professionally run fund of funds may save you much more from the damage you are doing to your own performance than they are charging in fees.

Four things we can all do to help mitigate some risk from being overexposed to funds with strong past performances which won't persist are to:

- Actively search for good managers whose styles aren’t flavour of the year, and,

- Have a process that actively mitigates against having too much of your portfolio exposed to those that are, and

- Think beyond the typical mainstream products (which are often mediocre) and actively search for less conventional products, and

- look for active investment managers who are aligned with your goals.

For example, a diversified multi-strategy fund with proven downside protection and good upside performance, that’s not constrained to overpriced, long-only equities and bonds, and is better diversified and somewhat contrarian in nature, could better suit your goals.

Such a strategy will not burn down with the latest fad in markets and should have a more disciplined approach to avoiding crowded trades and finding, and actively managing, the best opportunities available in the marketplace today.

Everyone loves a past winner, but it is the future performance that will drive your results. So, get aligned with great managers who have the opportunity set to benefit prospectively and are aiming to deliver exactly what you want and need.

Mistake #3: Picking a fund based on brand, rather than on credentials

Many investors feel more comfortable investing with big names or big brands. However, this comfort is often misplaced if you want investment performance.

Part of the reason is that managing tens of billions of dollars is often the enemy of good investment results. Being so big leaves a smaller pool of investible options, which then reduces the scope for differentiation. Many of these vehicles are therefore pseudo-passive in nature, even while pretending to be active. While the large scale is great for the business and for lowering costs, it can therefore be bad news when it comes to net of fee results which clients rely on. Routinely, we witness mediocre performance and no value-add being delivered by large institutional investment funds as a result. If that’s your experience, you may ask yourself why you stay invested with these funds (because you're missing out if you do).

In addition, big institutions can suffer from the ‘institutional imperative’ a term coined by Warren Buffett in his 1990 letter to shareholders as:

“The tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so.”

Career bureaucrats or politicians often hold senior positions in big funds, many of whom know (or care) little-to-nothing about what is required to run a fund manager that actually performs for clients. They often even actively contribute to a culture that damages the prospects of their investment managers being well-run and seems to have a penchant for recruiting previously underperforming fund managers to join their portfolio management teams (presumably because they can be a good place to hide if you're below average).

The reality is that funds management is often (but not always) a boutique people-business with limited scale, that needs the right culture and people to thrive. There are many highly credentialed and experienced investors operating in a boutique capacity in Australia today who are highly likely to outperform their institutional brethren.

Perhaps then, one of the best things you can do for your portfolio performance is to get your money out of your “branded”, lazy and lethargic fund being run by a large institution, and give it to more focussed people operating in a boutique who are aligned with what you want for your money and with whom you can have a more authentic relationship. This applies to your super money as much as it does to the rest of your portfolio.

The same goes for advisers

If your adviser is licensed by one of the big institutions, there is every chance the products they can invest in need to be listed in their APL (Approved Product List), and that this is actually quite restrictive and reflective of yesterday’s winners (in line with the usual biases) rather than the best options available for your money.

Don’t make the mistake of investing purely on the basis of your adviser’s sparkling personality alone, but ask whether they can demonstrate what makes them worthy of managing your money; in other words, think more about content than form or likeability. Assess whether the results they achieve for you match the rhetoric, are actually industry-leading results, or whether you have a better option elsewhere with a better resume. Demand high standards from those given the privilege of managing your hard-earned and give your capital to someone better if they can't meet those standards.

Reviewing - and comparing - performance

Results must be understood in the context of market conditions and portfolio objectives to be meaningful. We must also have realistic expectations of what’s achievable in different market circumstances.

That said, one of the great things about this industry is that ultimately it is relatively easy for an informed eye to assess results and to see who has delivered and who hasn’t if you understand how to do this properly in context.

Results speak louder than words, and they certainly speak louder than the brand.

Time to check if your portfolio is ready for the road ahead

There has rarely been a more urgent time to assess whether your money is being optimally managed. This is true whether it is with an institutional investment manager, super fund, adviser, or if you are managing it yourself.

Unfortunately, if your portfolio is like most portfolios, it may not be well-aligned with your goals and could be destined to underperform. Backing or instituting an aligned investment approach, implemented by diligent investment boutiques that recognise and have adapted to the massive change in market conditions is incredibly important right now.

Do all this and you could not only avoid a great deal of stress and disappointment from your portfolio over the coming years but also enjoy a fighting chance of great success.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's more challenging investment environment. Jerome has achieved net returns for clients of around 20% in both the challenging 2020 year and in 2021, with much lower drawdowns and volatility than Australian equities and hence much superior risk adjusted returns. His Wealthlander Diversified Alternative fund targets double digit returns annually for wholesale clients, with lower volatility and greater consistency than Australian equities, using a diversified multi-asset portfolio approach.

........

This has been prepared by Lucerne Australia Pty Ltd ACN 609 346 581 a Corporate Authorised Representative of AFSL number 481 217 and issued by The Trust Company (RE Services) Limited ACN 003 278 831 as responsible entity and the issuer of units in the Lucerne Alternative Investments Fund. It is general information only and is not intended to provide you with financial advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider the product disclosure statement, available by calling 03 8560 1440 or visiting our website (VIEW LINK), prior to making any investment decisions. If you require financial advice that takes into account your personal objectives, financial situation or needs, you should consult your licensed or authorised financial adviser. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. No company in the Perpetual Group (Perpetual Limited ABN 86 000 431 827 and its subsidiaries) guarantees the performance of any fund or the return of an investor’s capital.

2 topics

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Comments

Comments

Sign In or Join Free to comment