3 questions investors should be asking

The fixed income market has experienced a sharp rebound since the early days of the pandemic, with spreads on many fixed income securities narrowing to close to pre-crisis lows. Economies are generally regaining strength, albeit inconsistently based on local outbreaks and sensitivity to COVID-related weakness, while full recovery appears dependent on the approval and distribution of vaccines.

In this unusual environment, combining low yields and ongoing market volatility, we believe fixed income investors should focus on three essential questions:

- What could growth look like?

- How will inflation fit into the picture?

- And what segments of the market appear attractive on a relative basis?

We explore these issues below.

Global Growth: Multiple Paths

Looking ahead, low-interest rates and generally easy financial conditions should continue to support the economy, but its path likely depends on the successful development and distribution of COVID-19 vaccines, the generation of additional fiscal stimulus, and consumer behaviour. The recovery in China, despite some localised virus flare-ups, should be supportive of the global economic picture. With these dynamics in mind, we believe two scenarios are among the most likely:

1. K-Shaped Growth. A key recent dynamic has been companies and industries’ truly variable responses to the pandemic, depending on their cyclical exposure, ability to adapt, and in some cases benefits from economic shifts tied to the pandemic. Assuming some virus resurgence, a lack of fiscal response and/or consumer caution, we could see some sectors continue to improve while others stall or decline. Continued weakness of some especially COVID-sensitive sectors, such as transportation, leisure and hospitality, would make it hard to achieve meaningful headline growth. In this environment, sector selection would remain crucial.

2. Back to ‘New Normal.’ A more positive outcome would occur with gradual containment of the virus, improved treatment efficacy and the introduction of a vaccine late this year or early in 2021, with wide distribution sometime in the middle of next year. Additional fiscal stimulus would be an important component for stabilising or improving, growth rates until a vaccine is fully distributed. In this case, we would likely see economic growth stabilise at modestly positive overall levels analogous to 2011 – 15 when the lingering impacts of the global financial crisis hindered output. Here, with a generally improving fundamental backdrop, an understanding of balance sheet risk in light of valuation would take on increased importance.

At this point, the IMF is anticipating global contraction of about 4.4% for 2020, which is nearly a percentage point improvement from its projections in June, and an advance of roughly 5.2% in 2021. However, overall economic health again may be highly variable and require both a bit of luck and appropriate actions by fiscal and monetary authorities. For markets, 2021 will likely have a reasonable growth trajectory, albeit from levels still depressed from 2020.

Keep in mind that, during 2020, monetary policy has served to mitigate downside risk and create some upside in the markets. In contrast, central banks are likely to be on pause during 2021, and while they should continue to reduce tail risk, any growth and investment upside will likely need to come from fiscal policy. As a result, next year’s market could see more emphasis on the trajectory of fiscal stimulus, at least until the arrival of vaccines.

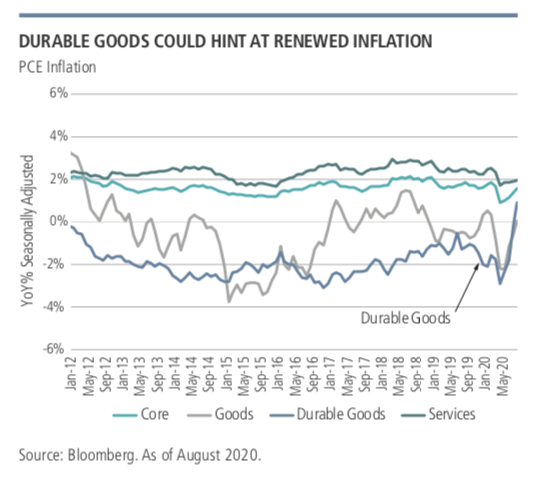

Inflation: Back in Sight?

In recent years, inflation has largely been a non-issue for investors, as central banks have been unsuccessful in attaining target inflation levels on a consistent basis, despite repeated efforts. However, the trajectory of inflation could become a renewed focus for markets given the regime change underway at central banks, including potentially several years of near-zero, short-term interest rates in the U.S. and the vast expansion of their balance sheets on a global basis, as well as growing government spending, to limit the impacts of COVID-19.

Recent developments in consumer spending also suggest modest pressure toward a higher inflation rate: Purchases of durable goods such as cars and washing machines have increased, both outright and as a percentage of total purchases, resulting in rising goods inflation pressure. This is a significant change versus the past decade when durables helped keep a lid on inflation. Moreover, the U.S. housing market has been robust in terms of overall sales volume. Thus far, this has had a muted impact on prices, but that could change with time.

Investment Strategy: Looking for Relative Value

As discussed previously, we anticipate that interest rates will remain low for a long period of time, as central banks remain committed to engineering economic recovery from the impacts of the pandemic. In particular, we expect the front end of the yield curve to be pinned down by zero-rate policy. Theoretically, longer rates could creep up with economic strengthening and intensifying inflation, but the lack of a term premium in markets suggests scepticism that inflation targets can actually be realised. In addition, the markets perceive that the Federal Reserve would likely implement policies to effectively cap long-end interest rates if we were to see any significant upward pressure in these rates.

In light of low-interest rates, we continue to believe that developed market government securities generally lack appeal from a risk/return perspective. Rather, we believe that credit provides more opportunity, particularly in high yield, where there is now better visibility into troubled sectors, while many companies have worked to reduce their vulnerability. Within emerging markets, hard currency spreads and local yields in many countries remain attractive, and currency performance could benefit from the global recovery. Agency mortgage-backed securities have stayed on our radar in light of the demand for high-quality spread, particularly for more conservative fixed-income investors.

A client-led partnership

As a private, independent, employee-owned investment manager, Neuberger Berman is structurally aligned with the long-term interests of our clients. Click 'FOLLOW' below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ashok K. Bhatia, CFA, Managing Director, joined the firm in 2017. Ashok is Chief Investment Officer and Global Head of Fixed Income, and a member of Neuberger Berman's Partnership and Asset Allocation Committees and Fixed Income's Investment Strategy Committee. Previously, Ashok has held senior investment and leadership positions in several asset management firms and hedge funds, including Wells Fargo Asset Management, Balyasny Asset Management and Stark Investments. Ashok has had investment responsibilities across global fixed income and currency markets. Ashok began his career in 1993 as an investment analyst at Morgan Stanley. Ashok received a BA with high honors in Economics from the University of Michigan, Ann Arbor, and an MBA with high honors from the University of Chicago. He has been awarded the Chartered Financial Analyst designation.

........

This material is provided for informational purposes only and nothing herein constitutes investment legal accounting or tax advice or a recommendation to buy sell or hold a security. This material is general in nature and is not directed to any category of investors and should not be regarded as individualized a recommendation investment advice or a suggestion to engage in or refrain from any investment-related course of action. Neuberger Berman is not providing this material in a fiduciary capacity and has a financial interest in the sale of its products and services. Neuberger Berman as well as its employees does not provide tax or legal advice. You should consult your accountant tax adviser and/or attorney for advice concerning your particular circumstances. Information is obtained from sources deemed reliable but there is no representation or warranty as to its accuracy completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types. Investing entails risks including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

The views expressed herein are those of the Neuberger Berman Fixed Income Investment Strategy Committee. Their views do not constitute a prediction or projection of future events or future market behavior. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events or market behavior may differ significantly from any views expressed. This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions. The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

All information is as of September 30, 2020 unless otherwise indicated. Firm data, including employee and assets under management figures, reflect collective data for the various affiliated investment advisers that are subsidiaries of Neuberger Berman Group LLC (the “firm”). Firm history and timelines include the history and business expansions of all firm subsidiaries, including predecessor entities and acquisition entities. Investment professionals referenced include portfolio managers, research analysts/associates, traders, product specialists and team-dedicated economists/strategists.

CFA, Managing Director, Chief Investment Officer and Global Head of Fixed Income

Neuberger Berman

Ashok K. Bhatia, CFA, Managing Director, joined the firm in 2017. Ashok is Chief Investment Officer and Global Head of Fixed Income, and a member of Neuberger Berman's Partnership and Asset Allocation Committees and Fixed Income's Investment...

Expertise

CFA, Managing Director, Chief Investment Officer and Global Head of Fixed Income

Neuberger Berman

Ashok K. Bhatia, CFA, Managing Director, joined the firm in 2017. Ashok is Chief Investment Officer and Global Head of Fixed Income, and a member of Neuberger Berman's Partnership and Asset Allocation Committees and Fixed Income's Investment...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

Battery Age Minerals: Undervalued, uncovered, unmissable

Fawkes Capital Management