5 stocks to buy on weakness

It is important to find ideas where companies can generate cash flow growth regardless of the macro backdrop. Here we look at five stocks that pass our filters and would look attractive on market weakness.

If a company can generate strong cash flows in different market environments this should be ultimately be reflected in the company's share price over the medium term, regardless of stock market volatility.

The examples we have set out below provide more detail around this idea, with all these companies (operating in a wide variety of industries) demonstrating an ability to either double, or generate predictable growth (using EBITDA as an admittedly imperfect proxy).

Just as important in stock selection, is what is the capital (capex) required to generate that cash flow growth? Return on capital employed is a critical metric to assess a company’s ability to generate shareholder returns. The companies listed below have a combination of organic growth (Atlas Arteria and Baidu), while Tabcorp and Bega have invested significant capital to generate the cash flow trajectory. We believe both Tabcorp and Bega have strengthened their industry position by embarking on this strategy, hence we remain supportive of this use of capital.

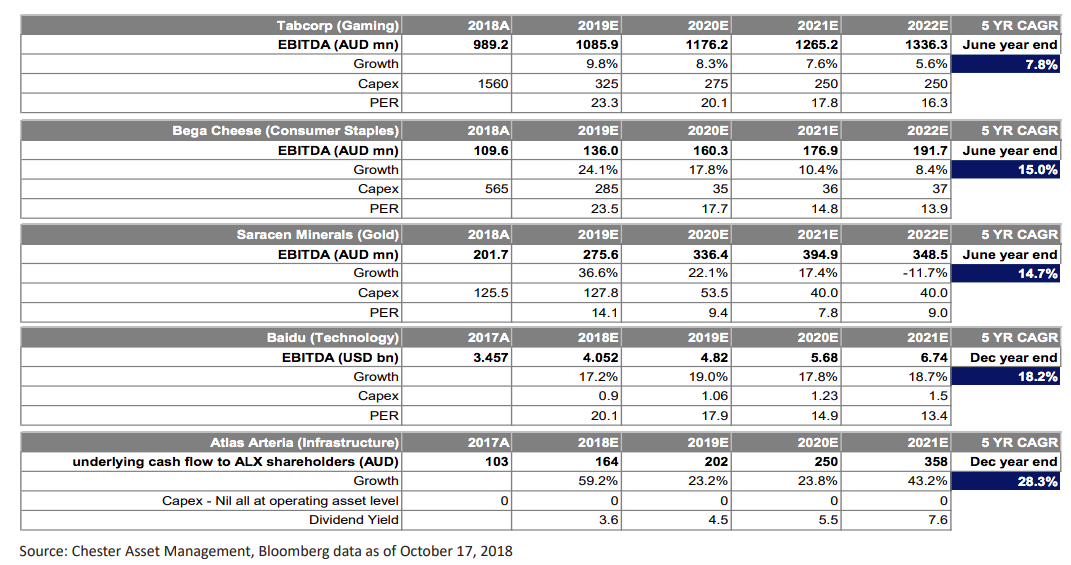

Tabcorp (TAH)

The combined TAH and Tatts Group business has strong market positions in Lotteries, which is an effective monopoly, and wagering, where the combined group remains the market leader, albeit with strong competition. While there have been industry headwinds in wagering over the past 5 years due to corporate bookmakers (led by Sportsbet and now Bet Easy), the TAB wagering market share has eroded over this time period.

TAH is now in a position where due to regulatory changes, there is a more level playing field in which to operate. In wagering, various state-based Point of Consumption (PoC) taxes have been progressively announced to counter the tax avoidance online wagering companies have benefitted from for several years. As the new PoC taxes are introduced next year we expect to see a large impact to corporate bookmakers profitability. Hence there is a possibility that this PoC tax contributes to improved yields for TAH courtesy of less competitive market pricing, along with fewer inducements for customers. The likely outcome is that TAH holds wagering market share, if not growing it.

The combination of organic growth and cost synergies achievement underpins our forecasts for ~9% CAGR EBITDA growth on the back of mid-single

digit revenue growth over the next 3 years. Offering investors a dividend yield well in excess of 4% at current prices and trading at sizable discount to our valuation of $5.45, we believe TAH is attractive below $4.50, where we believe it will provide a predictable 10-12% total shareholder return over the next 2-3 years.

Bega (BGA)

We have always been attracted to Bega for the quality of the business and the Management team and the recent pull back creates an attractive entry price. In its efforts to create a Great Australian Food Company BGA has undergone several transformational changes in the past 2 years. The first was the 2017 acquisition of Mondelez Australia and NZ for A$460m which provides BGA with the leading position in spreads (Vegemite and Peanut Butter) through strong brands, capable personnel and facilities.

We do note the business performed below our (earnings) expectations in FY18 however significant investment was made on marketing and integration, providing a strong platform for future growth. In July 2018, BGA acquired the Koroit milk processing plant in Western Victoria, we believe this is a strategically compelling asset for BGA to own and underpins much of the cash flow growth of the next two years.

Saracen (SAR)

Following FY18 drilling success at Karari and Whirling Dervish, evident within the August reserves report there is increased confidence in the mine life at Carosue Dam. Reserves life currently stand at 7 years with potential for 10+ given the shallowness of SAR’s mines compared to peers and grades increasing at depth. SAR has also outlined a plan to increase gold production to 350kozpa however optionality exists with crushers to push this to 400kozpa. Given the strength of the balance sheet (>AUD100m net cash) and Management we believe SAR is well placed to continue to generate cash flow growth, and as a gold producer, provides a non correlated return to most other sectors.

Atlas Arteria (ALX)

Atlas Arteria is a toll road owner with assets in France (85% of its Net Asset Value) and in the US. This is a relatively simple story, wrapped up in a complex ownership structure. Most of the cash flow growth to the holding company (ALX shareholders) is coming via both organic growth and a significant reduction in interest payments following a debt restructuring this year.

Macquarie Bank has simplified the structure recently by exiting the business and internalising the management of the assets. We see further simplification strategies to unfold over the next 12-18 months, which could add upside to the anticipated doubling of the distribution to shareholders over the next 3 years. Regardless of what bond yields do, very few infrastructure stocks can provide that cash flow growth.

Baidu (BIDU US)

Baidu is China’s dominant search engine. We have started to add BIDU to the portfolio recently as the share price has retraced 35% from its peak on concerns that Google may re-enter China and liquidity outflows on poor sentiment toward China. We think concerns around Google re-entering China (after exiting in 2011) are overplayed given the current rhetoric from Washington and our understanding is that BIDU continues to win ad share with its news feed product.

It is the market leader in AI programs for autonomous vehicles, it has almost 20% of its market cap in cash, and is growing at a high teens rate. On a price to growth basis, it remains very compelling value.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

4 stocks mentioned

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management