A few Highlights and Challenges for the Big Four

We have decided to take a look at the major banks in Australia. There are a number of reasons why stock market investors are worrying about the Australian banking sector which we outline below, followed by a discussion on each of the major banks.

Challenges

- The Financial Services Royal Commission,

- Potential interest rises,

- Political instability leading to concerns about changing regulations,

- Worries about an overheating residential property market and the resulting exposure of our banks,

- Falling $AUD.

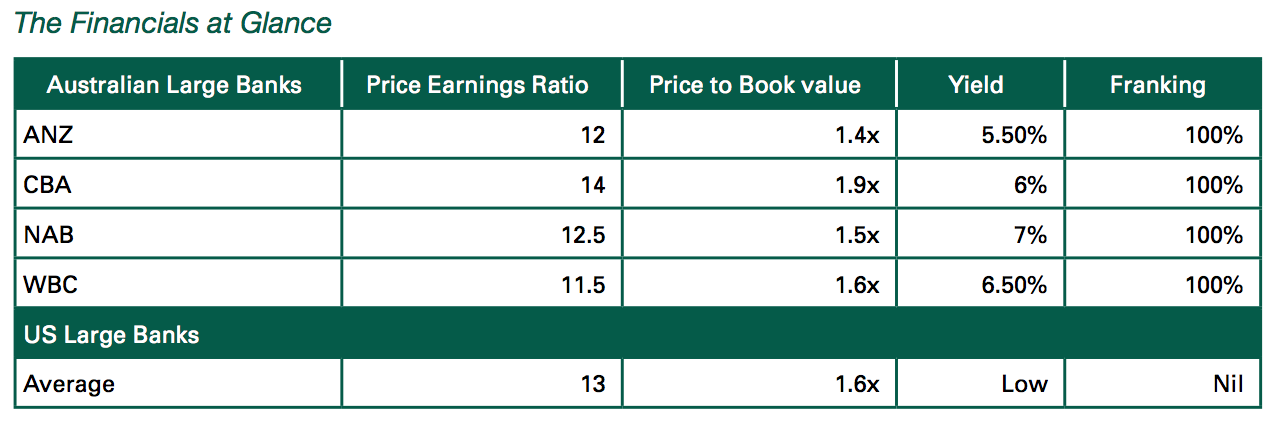

On the numbers above we can make some interesting observations:

- Westpac is the cheapest bank on a PE basis.

- ANZ is the cheapest bank on a price to book basis.

- NAB is the highest yielding bank.

Including franking, our banks provide excellent tax effective yields. Compared to the large US banks, Australian banks compare favorably, particularly the dividend yields in Australia provide a compelling comparative investment.

The Australian banks, as a sector, are the recent losers versus both the Australian equity markets as can be seen above and also against globally strong equity markets. Since the Global Financial Crisis (GFC) occurred, NAB has been a dramatic underperformer and CBA the big outperformer on the Australian Stock Market. We think this is the time to be reassessing exposure to Australia’s major Banks.

A few Highlights and Challenges for the Big Four

Australia and New Zealand Banking Group. (ANZ)

As with all of the Big Four, retail banking conditions remain tough with a significant slowdown in owner occupied home loan growth, higher funding costs and the inability to re-price loans. ANZ has underweight mortgage exposure vs peers and thus may be in a better position than some of the other banks; lower impairment charges are a strong positive, albeit surprising.

Commonwealth Bank. (CBA)

The negatives for CBA are the upcoming costs of addressing governance and cultural issues. Also, CBA has fallen below industry growth rates and this may also mean an increase in costs. As the largest retail bank, with over 25% market share, they are less exposed to the riskier agriculture and manufacturing sectors. CBA’s online and mobile platform seems to resonate better than the others with the younger generation.

National Australia Bank. (NAB)

Despite talking of cost reductions NAB seems to be losing the battle, a big part of this is regulatory expenses. As with the other banks, renewed competition for new mortgages, negative sentiment from the royal commission and the ACCC and Productivity Commission, and a challenging political environment the increased funding costs will be bore by shareholders rather than borrowers – at least for the short/medium term. Despite this, NAB has a very strong balance sheet and low impairments.

Westpac (WBC)

WBC’s focus on cost management may be detracting from business growth and mortgage competition and thus profitability under pressure. Funding costs are increasing; WBC’s core revenue driver, its net interest margin, has fallen to its lowest level since 1H15 on the back of rising funding costs from international markets, adding roughly $400m to the banks cost base. These costs can, and traditionally have been, recouped by increasing the standard variable interest rate on mortgages, however, given the current political environment and the focus on the banks, this change may prove to be difficult; Westpac has an overweight position in the housing market. The key upside for Westpac is the potential accelerated expense management and low global relative valuation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

3 stocks mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment