A fit runner facing an uphill climb

Last year, we compared the global economy to a fit runner competing in a marathon. As we approach the end of 2018, the runner is still in good shape but facing an uphill climb.

There are trade tensions, moderating Chinese growth, emerging market volatility and ongoing monetary policy normalisation by central banks around the world. Nonetheless, there is sufficient constructive growth momentum globally for risk assets to perform. Increasingly, investors will be focusing on and anticipating the end of the U.S. growth cycle and what it means for asset allocation. We summarise our views here.

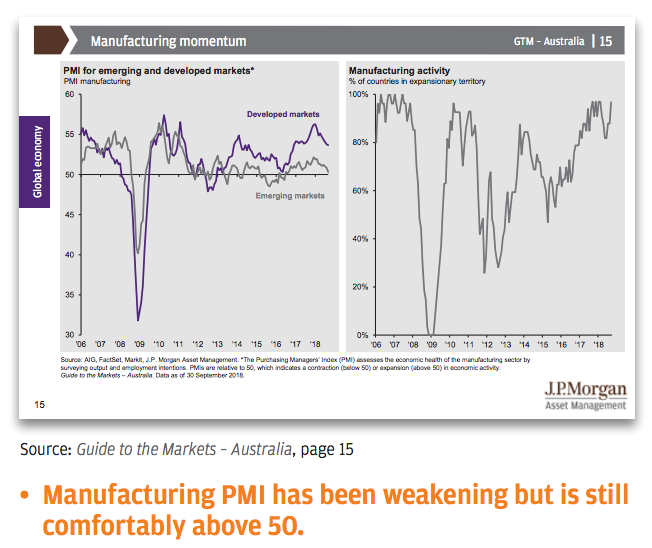

The global economy is still running strong

Underlying momentum from consumption and corporate investment, combined with fiscal stimulus, is helping the U.S. economy to extend its growth streak into its 10th year. While the current fiscal boost should gradually fade going into 2019, a strong job market should continue to support household spending, which encompasses 70% of the U.S. economy.

In Europe, despite the political noise, the unemployment rate continues to fall, supporting consumer sentiment. The euro area is also in an earlier phase of the economic cycle vs. the U.S. In Asia, easing momentum in the global trade cycle poses a challenge, but modest inflation is allowing the region’s central banks to maintain loose monetary policy

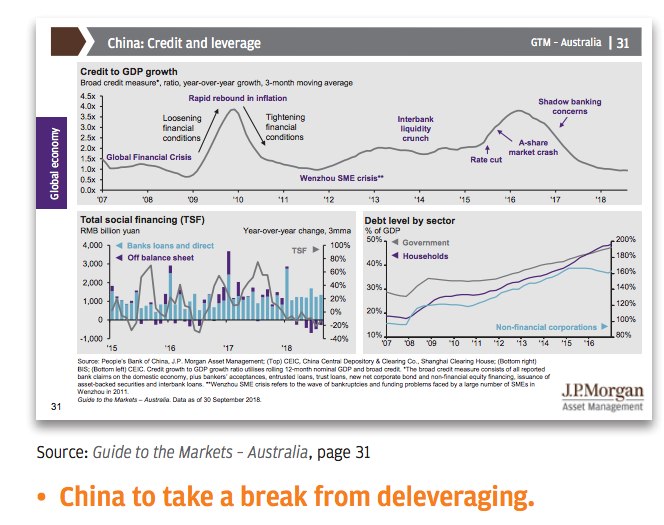

China: Taking a break from deleveraging

China’s economic indicators have softened in recent months, reflecting the impact of the last 18 months’ deleveraging effort. Fixed-asset investment has, in particular, slowed notably. Uncertainties stemming from U.S.-China trade tensions are also undermining business sentiment. Unfortunately, there are currently few signs that suggest Washington and Beijing will reach an agreement to meaningfully de-escalate trade disputes in the near term.

We expect Beijing to remain focused on its medium-term objective of reducing leverage and containing financial risks. Yet, like a runner on a long run, it will need to slow down to re-fuel and re-hydrate. Sector-specific and targeted monetary policy easing is likely to be the way forward in the months ahead to help stabilise growth. The export sector could be a beneficiary of this easing. A fiscal boost to infrastructure investment could also be a quick remedy

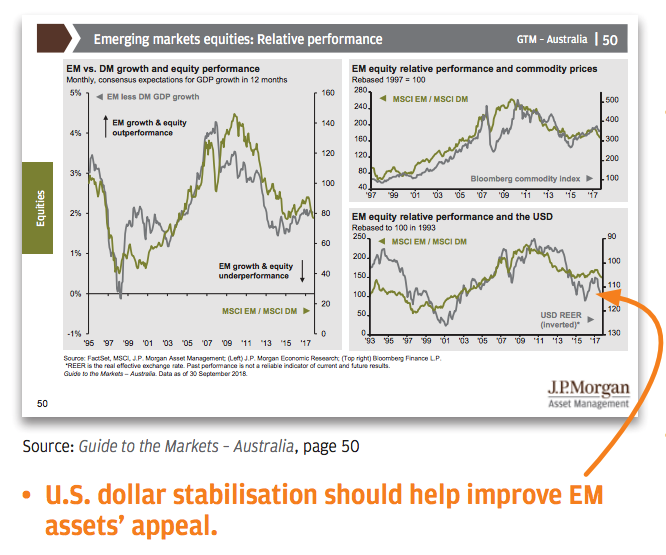

Emerging markets face strong headwinds from the U.S. dollar strength

U.S. dollar strength this year has spurred capital outflows from emerging markets (EM), exerting pressure on the economies and currencies. Yet EM countries are not all the same. It is important to differentiate based on fundamentals: Countries with high inflation, insufficient foreign exchange reserves and/or a current account deficit will require more aggressive monetary tightening to relieve currency pressures. We continue to expect that the U.S. dollar is on a long-term downtrend due to the U.S. current account and fiscal deficits, but the near-term strength could persist.

The weakening of the Chinese yuan has put pressure on Asian currencies, despite these countries’ healthy balance-of-payment positions and ample reserves. But with the People’s Bank of China signalling it will pay more attention to defending the currency, other Asian currencies and assets should also find a greater basis for stability

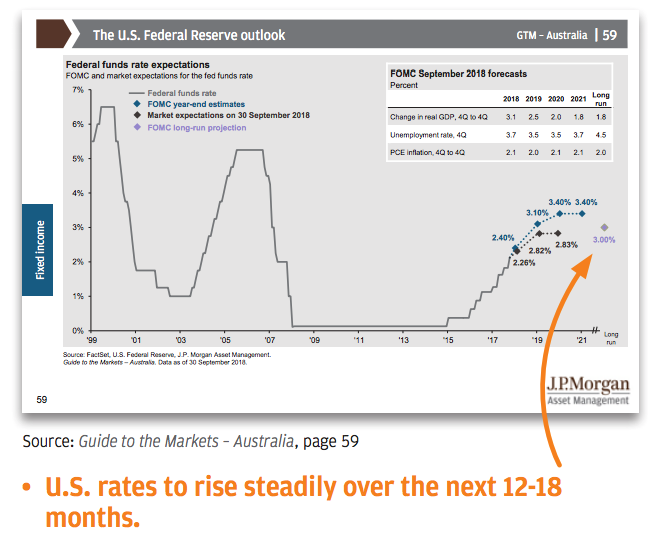

Ongoing monetary policy normalisation

The U.S. Federal Reserve (Fed) is expected to raise policy rates once a quarter for the next 12-18 months as full employment and data from the core personal consumption expenditure deflator—the Fed’s preferred inflation measure—have been consistent with its dual policy mandate. With the current economic momentum, the Fed could raise policy rates beyond its projected long-run rate of 3% by the second-half of 2019. This could start to cool economic momentum.

The European Central Bank is also on track to end its asset purchase program by the end of 2018. The G4 central banks, in aggregate, are expected to shift from being a net buyer of assets to a net seller in the first-half of 2019. Developed market government bond yields, especially in the euro area, are expected to rise, and potentially increase market volatility going forward.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

Expertise

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets