A glimpse into the post-COVID world

Following the longest expansion on record, the global economy is currently plunging into what could easily become one of the deepest but also shortest recessions in modern times. However, business cycle history offers few clues for what is likely to unfold over our cyclical six to 12 month horizon, which makes the outlook even more uncertain than usual.

This time truly is different ...

There is no precedent and thus no good playbook for the global recession that is currently unfolding. Recessions are usually caused by the interplay between severe economic and/or financial imbalances building up during the expansion and a typical late-cycle tightening of monetary policy, sometimes aggravated by a sharp increase in the price of oil.

This time is very different because the underlying cause of the downturn is a truly exogenous shock that originated from outside the economic and financial sphere: a highly contagious new coronavirus that has been spreading fast in a globalized world since the start of the year. As the severe health crisis in several strongly affected regions illustrates, the COVID-19 pandemic threatens to overwhelm healthcare systems in many countries around the globe over the next few weeks and months.

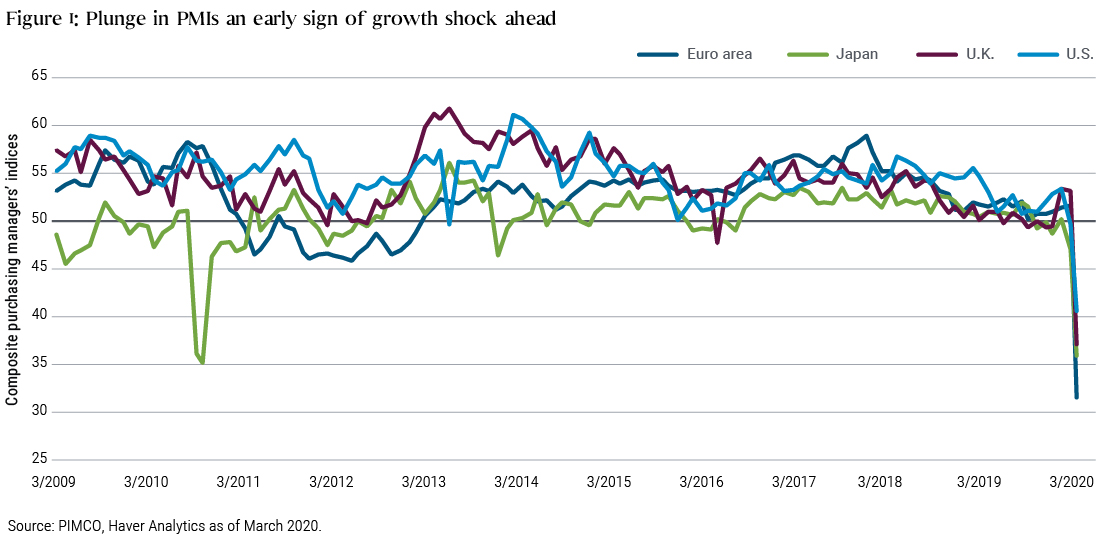

Most governments have responded by aggressively curtailing economic and social activity in order to suppress the further spreading of the virus as quickly as possible. This has already led to a sharp drop in aggregate output and demand in many Western economies during the second half of March (for example, composite purchasing managers’ indices plummeted – see Figure 1), which is likely to continue in the near term as suppression efforts not only remain in place but are being intensified. Thus, we are seeing the first-ever recession by government decree – a necessary, temporary, partial shutdown of the economy aimed at preventing an even larger humanitarian crisis.

Importantly, despite the record length of the expansion that likely ended this March, there were no major domestic economic imbalances in most advanced economies: Consumers were less exuberant than in the previous cycle, firms hadn’t overinvested in capacity, housing markets – with a few exceptions – didn’t overheat, and inflation was generally low and stable. All of this should be conducive to a recovery less impeded by economic legacy issues once the virus is under control.

However, we have been concerned about financial imbalances that have been building in the U.S. corporate sector with a significant rise in leverage on the balance sheets of riskier and more cyclical companies. We return to this downside risk below.

... as is the economic policy response

What is also different this time is the unprecedented speed and size of the monetary and fiscal response to the crisis.

Policymakers have been pulling out virtually all the stops in an attempt to keep the recession from turning into a lasting depression with mass bankruptcies and mass long-term unemployment.

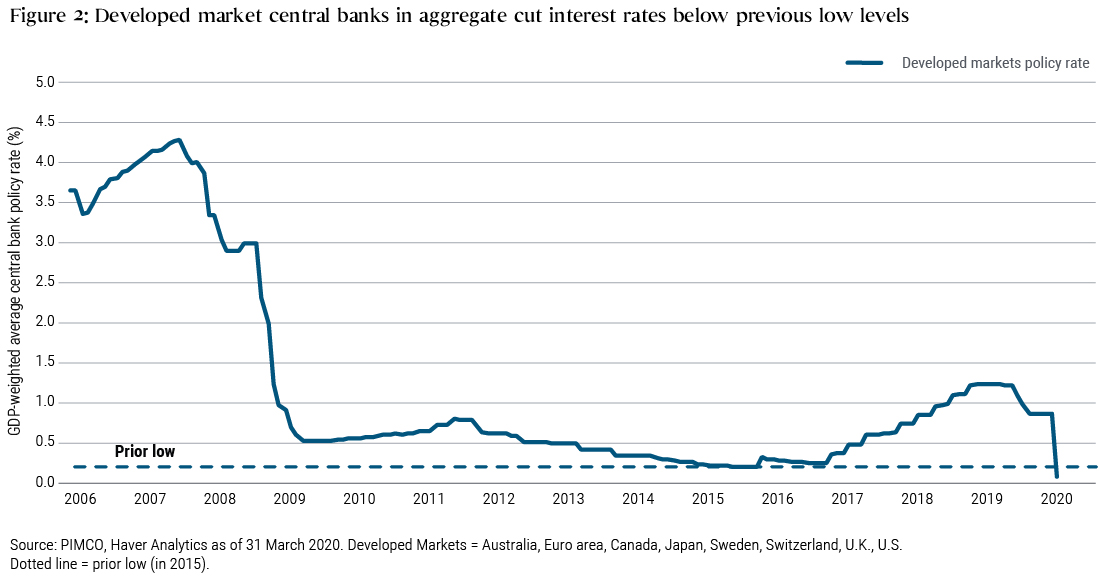

Central banks have stepped up as lenders of last resort not only for banks but increasingly also for other financial intermediaries and even for nonfinancial corporations through a range of lending and asset purchase programs. Moreover, through near-zero or negative interest rates (see Figure 2) and large-scale purchases of government bonds, central banks also provide a much-needed backstop for fiscal policy.

As ever, the euro area faces additional coordination challenges. After initial communication missteps, the European Central Bank (ECB) appears to have put in place a robust framework for dealing with the strains on the euro area during a deep recession, while acknowledging the necessity of a significant fiscal response.

Many governments have also reacted swiftly by addressing both liquidity and solvency concerns. Liquidity support includes large-scale guarantees for bank loans to businesses, delaying tax payment deadlines for individuals and corporations, and providing backstops for central bank lending programs (not all programs are being implemented across all governments). Many governments are also providing income support for households and firms through a range of transfers to individuals and subsidies for companies.

In many countries, the fiscal response underway already exceeds that during the Great Recession of 2008–2009, and additional measures are likely to be announced over the next several months.

While a deep recession is inevitable given the mandated temporary shutdown of major parts of the global economy and given that many of the recently announced transfers and loans will only arrive after some delay, the large fiscal response will very likely help prevent a global depression and support economic recovery once the restrictions on economic activity are lifted.

As with the monetary policy response, the logic of the euro area dictates greater uncertainty over the fiscal response and its implications in the short and medium term (for details, see the blog post, “In Europe the Crisis Policy Response Is Substantial, But More Is Likely Needed”). Fiscal and monetary coordination is of course easier to achieve with one Treasury and one central bank.

Our cyclical base case: from hurting to healing

Given the swift and large monetary and fiscal policy response and in the absence of major imbalances in the real economy that would require a prolonged period of cleansing and adjustment, we expect the global economy to transition from intense near-term pain during the virus-suppression phase to gradual healing over the next six to 12 months, once the spread of the novel coronavirus is under control and the restrictions are being lifted.

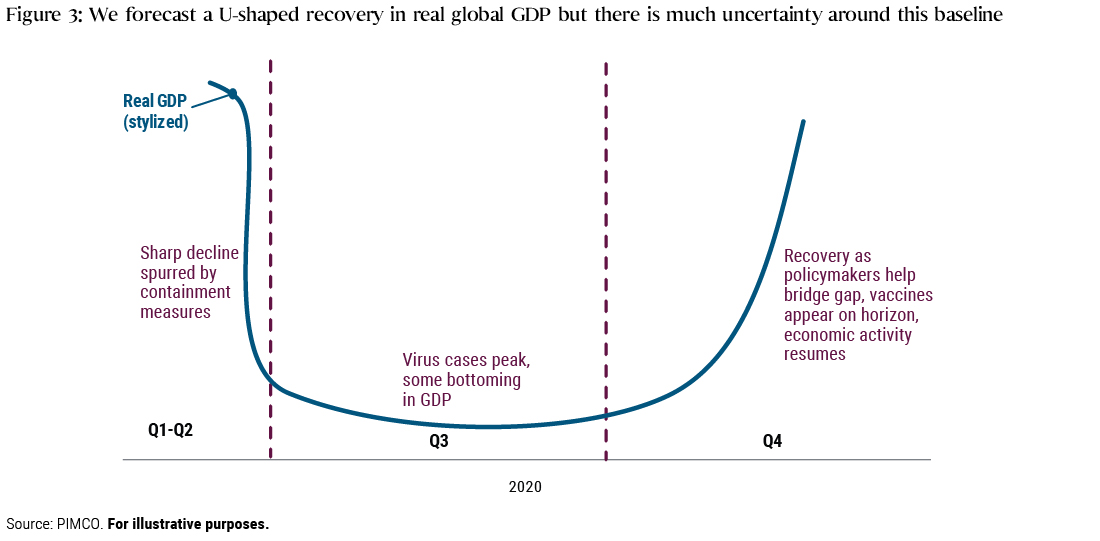

However, our base case remains a U-shaped rather than a V-shaped recovery (see Figure 3) because the restrictions on economic activity will likely be lifted only gradually and at different speeds for different sectors and regions. Also, repairing the supply chain and overcoming logistical and transport bottlenecks will take some time. As a consequence, following the nosedive in economic activity that is currently underway (the downward I in the U), we expect the bottoming process to last a few months after the virus is under control (the L in the U), before output and demand ramp up back closer to more normal levels eventually, helped by fiscal and monetary support (the upward I in the U).

We plan to provide more details on our growth forecasts for the major economies in a follow-up publication in the coming weeks.

The risks: longer stagnation, or recovery and relapse

We see two main downside risk scenarios to our base case of a U-shaped economic trajectory over the next six to 12 months: a prolonged L-shaped trajectory, or a recovery interrupted by relapse – call it a W. The two main swing factors that could push us into these more adverse scenarios are 1) the shape of the pandemic curve, and 2) the shape of the default curve in the highly leveraged, cyclical sectors of the economy that may not have direct access to central bank and/or government balance sheets.

A prolonged stagnation would likely result if governments’ current suppression strategy turns out to be insufficient to significantly slow the spread of the virus, so that suppression measures have to be kept in place for longer than the six to eight weeks currently anticipated. With activity depressed for longer in this scenario, many of the more highly leveraged firms in the cyclical parts of the economy would likely default, feeding back negatively into jobs and demand.

Conversely, even if the virus suppression is successful in the near term and a lifting of containment measures leads to a revival of economic activity, we may experience a second wave of contagion later this year that leads to renewed economic stoppages. A relapse following the recovery would likely be exacerbated by defaults of cyclical companies that survived the first wave.

A V-shaped trajectory is in theory possible, although not something that we are currently placing a great deal of weight upon. Such a trajectory would be the result of the combination of successful macroeconomic policy interventions and also, crucially, medical breakthroughs and increases in the capacity of health systems and public administration more generally to surprise on the upside in terms of dealing with the current crisis.

A glimpse into the post-COVID world

Markets are discounting machines, so it’s never too early to think about the potential longer-term consequences of this crisis. Even if the more adverse cyclical risk scenarios (the L and the W) can be avoided and our U-shaped “hurting to healing” base case comes to pass, this crisis is likely to leave some long-term scars that investors should start considering now.

- First, globalization may be dialed back even faster now as firms try to reduce the complexity of their global supply chains, which proved vulnerable not only to trade wars but also to sudden stops caused by natural or health disasters. In addition, governments may use health concerns to implement further curbs on trade, travel, and migration.

Thus, companies, sectors, and countries that are very dependent on trade and travel are likely to take more than just a temporary hit to their business models.

- Second, private and public sector debt levels will likely be significantly higher after this crisis. This could erode central bank independence further as monetary policy becomes increasingly involved in allocating resources to the nonfinancial corporate sector (essentially a fiscal act) and needs to ensure that the costs of servicing government debt remain low. If governments continue to engage in more expansionary policies even after the crisis, fiscal dominance of monetary policy may eventually lead to significantly higher inflation rates than markets currently price in. But with central banks capping the rise in nominal yields that would normally result from higher inflation, real rates would tend to fall as inflation rises.

- Third, many households will likely come out of this crisis with higher levels of personal debt and will have experienced severe income and/or job losses. This in turn could increase the demand for precautionary saving in relatively low-risk instruments such as cash and bonds. Also, we expect many households will strive to build home equity faster by reducing mortgage debt. Thus, with the private sector saving glut likely to rise further, investors should brace themselves for a New Neutral 2.0 of even more depressed real interest rates over the secular horizon.

Investment implications

We are “dealing with disruption” on an unprecedented scale. In this highly uncertain environment – as PIMCO has done during previous periods of extreme dislocation – we will focus on a defensive approach at a time of heightened volatility. We will look to position to take advantage of normalization of market conditions over time but, for now, we believe a caution-first approach is warranted in an effort to protect against permanent capital impairment.

Want to learn more?

For our latest insights into market volatility and the implications for the economy and investors, visit our “Investing in Uncertain Markets” page here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Joachim is a managing director and global economic advisor based in the Newport Beach office. He is a member of the Investment Committee and leads PIMCO's quarterly Cyclical as well as the Secular Forum process.

Featuring

Joachim Fels,

PIMCO

Joachim is a managing director and global economic advisor based in the Newport Beach office. He is a member of the Investment Committee and leads PIMCO's quarterly Cyclical as well as the Secular Forum process.

Joachim is a managing director and global economic advisor based in the Newport Beach office. He is a member of the Investment Committee and leads PIMCO's quarterly Cyclical as well as the Secular Forum process.

Expertise

Comments

Comments

Sign In or Join Free to comment