A long expected dividend cut

BHP today made the least surprising announcement since the Fed raised rates in December – they have abandoned their progressive dividend policy. This wasn’t the only interesting development from the company that was once the largest in Australia. “Some are saying the worst is over – which to some degree is true – as the next profit results won’t see the same sort of plunge as we’ve seen this time around,” said Gavin Wendt, Founding Director at Minelife.

One of the big unknowns going into the result was the scale of the losses from the Samarco disaster. While they’ve announced over $1b (pre-tax) in write-downs and losses on the project, the size of the fine has yet to be determined or accounted for. Media suggestions are that the fine could be around $5b for the joint venture project which is 50% owned by BHP.

Results came in significantly below analyst expectations according to Commsec, however not everyone was surprised. John Robertson from EIM Capital Managers said, “The results were consistent with my general expectation that the company's earnings performance would continue to underperform the commodity markets in which it operates. That has been evident throughout the cycle.”

Mr Robertson was highly critical of BHP’s management forecasts, suggesting consistent errors. “The company is very good at blaming external events to allay criticism. Its market analysis has been consistently wrong. It was forecasting big raw material growth rates from China; even after China had flagged it was going to cut back on investment spending.“

The company highlighted large cutbacks to CapEx, sighting global economic uncertainty as the reason. With falling grades at Escondida and falling rig counts in its petroleum operations, could this be indicative of future production falls? Capex is down 40%, and with a goal of reducing it to $5b by the end of 2017.

Mr Robertson, however, doesn’t buy the excuses. “Commodity markets are behaving just as you would expect them to behave given the global growth profile. Global economic uncertainty is a euphemism for "we got it hopelessly wrong".”

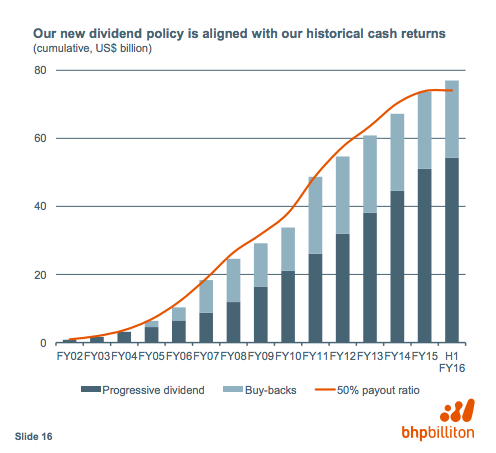

While the graph itself is correct, it is interesting to note how BHP has presented its dividends in the company report showing rising (cumulative) dividends.

(Image source: company presentation)

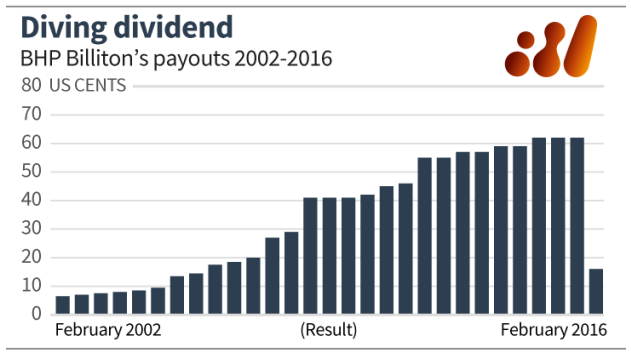

For investors who haven’t held BHP since 2002 however, it looks more like this:

(Image source: Sydney Morning Herald)

While iron ore prices have recovered from their recent lows, Gavin Wendt suggests that this perhaps can’t be relied upon. “It’s hard to see much of a recovery in iron ore prices anytime soon (if ever) and BHP is hugely leveraged to iron ore (about 50% of earnings), meaning recovery will be slow in my view. Then again, BHP is a bellwether mining stock and if investors continue to get serious about resources, then its share price will recover irrespective of near-term challenges.”

BHP closed up 2.62% today on the back of iron ore price support and broad strength in the miners.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

2 topics

1 stock mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment