A look inside the AustralianSuper engine room

With more than $170 billion of assets under management at the end of 2019, Mark Delaney from AustralianSuper manages one of the largest pools of funds in the country. While managing large pools of funds no doubt presents many unique challenges, what stood out to me was that Delaney was dealing with many of the same issues that everyday investors are challenged by. Are government bonds still worthy inclusions in a portfolio? How do you position for what might lie ahead? And how can you ensure you have true liquidity for the next crisis?

We don’t often get to see how the investment team at AustralianSuper operates, but in a recent webinar for Bloomberg, Delaney lifted up the hood and gave us a look inside. In this wire, I share some of the highlights.

The big picture

Delaney says that while the economic situation looks dire in the short term, over the longer term he’s more positive. He says there are three things he focused on when thinking about markets today:

- What is the immediate impact of the virus?

- What does the second half of 2020 look like? Do we see a recovery, or a second wave?

- What does 2021 and beyond look like?

“The further you look out, the more confident you become. The nearer you look, the more nervous you become…Economic data is dire currently, but will it be dire in 2021? We don’t think so.”

He says a ‘second wave’ has always been a big concern for markets, as many models include a material second wave as people go back to their lives and mobility increases. They’ve been looking at countries across Europe and Asia that have begun to open up, particularly those who were earlier in opening up, to get a sense for how this is playing out.

“Recently we’ve begun to see signs of substantial clusters in places that have opened, like Beijing. The one in Beijing is quite significant, because it’s big enough to cause a fair bit of concern.”

He said that Beijing could be “a very interesting test case” to see whether the ‘test and trace’ approach (such as is being employed in Australia) is effective at suppressing the virus.

The beginnings of a new cycle?

In 2018 and 2019, many agreed that markets were getting towards the end of the cycle. Indeed, we here at Livewire Markets did a whole event about ‘late-cycle investing’! But as we were all reminded of repeatedly, nobody knows when or why the cycle will end.

“No one knew what the trigger would be, and no one could’ve guessed it’d be a virus.”

With markets having substantially repriced through February and March, he says they appear to have set themselves up for a new cycle.

“We still think that’s probably the right mindset – looking forwards to the new cycle. There’s a lot of scope for economies to grow in that new cycle.”

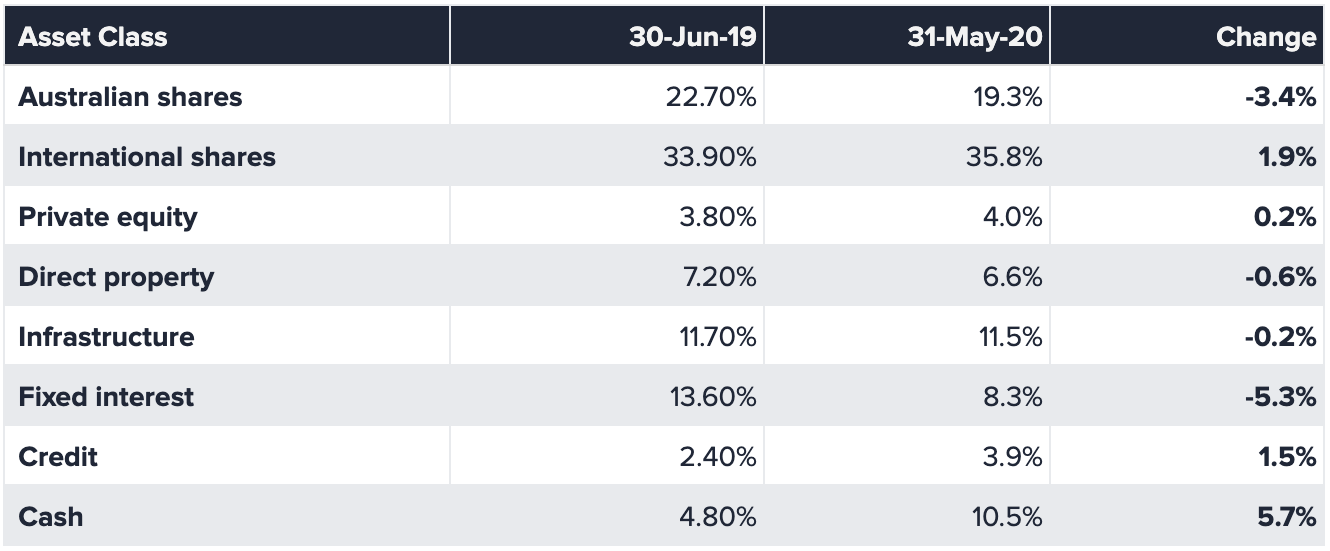

Despite this, cash levels in their flagship Balanced Option remain higher than historical levels. Delaney said that the higher cash levels are partly due to high valuations in mid-risk assets such as property, infrastructure, and credit.

“We’re waiting for valuations in those asset classes to improve.”

Allocations to equities are close to historical averages. He says they declined to “chase” stock markets when they rallied in March and April.

“If we get a chance, and the markets pull back substantially, we’ll look to deploy some of that cash. Otherwise, we’ll look to start putting money into assets like credit, and hopefully, some really good unlisted opportunities.”

When it comes to government bonds though, they’re remaining under-weight. With yields still under one percent, prospects for both income and capital gains are limited.

“We think if the recovery does take hold, the pressure will be on government bond rates to rise. But it won’t be much. Central banks are trying to keep those rates low by buying substantial amounts of them.”

Among the big arguments for holding government bonds have been the negative correlation with risk assets, and the easy liquidity they can provide in times of crisis. But Delaney says they’re looking for other sources of diversification.

“There are many cases in history where you lose money on bonds and equities at the same time. They’re not the perfect hedge… When liquidity became hard to get in the crisis, Treasury Bond yields went up when you thought they should’ve gone down. That was only a short-term thing, and then yields went back down again. But with yields being very low, and the zero bound looking to be pretty firm for the time being, they don’t offer the same diversification benefit as what they’ve done historically.”

Instead, he prefers having a balanced portfolio of diversifiers such as holding offshore currency, unlisted assets, and using synthetic strategies.

“You just need a balanced portfolio of diversifiers, rather than purely or extensively relying on fixed income.”

AustralianSuper Balanced Option Asset Allocation

No concerns with early access requests

When the government first announced the early release of superannuation changes at the beginning of the crisis, many commentators (admittedly, this author was one of them) were concerned whether some super funds would have sufficient access to liquidity to meet the demands. Many of Australia’s big super funds invest heavily in illiquid and unlisted assets on the basis that members would not require access to their funds for many years.

As it turns out, the requests have been processed without issue. No small feat from a logistical perspective, given over 300,000 requests processed for AustralianSuper alone. Link Administration (LNK) no doubt had a big job, as they administer AustralianSuper, REST, HostPlus, and a suite of smaller funds. Given the size of these funds and the fact that some of them operate in the hardest hit industries, there may have been close to a million early release benefits paid in the past few months.

Delaney said the scheme had gone “really well”, with requests processed quickly and $2.2 billion paid out to people who needed the funds. He notes however, that it’s come at the cost of long-term retirement savings, and it’s something to be conscious of and try to rebuild.

The big question this raises though is whether we’ll see a repeat of this scheme during future crises. If so, do funds need to change the way they manage portfolios?

“Part of the reason you can have a long term investment horizon is because you consider the money’s going to be there for a long time.”

A lesson on recency bias

Towards the end of the audience Q&A session, he was asked a series of questions about banks and banking crises. While he pointed out that he’s not a bank analyst or even an equities specialist, I though his remarks were an interesting comment about people’s propensity to expect the current crisis to look like the most recent past one.

“I think this focus on the banking crisis might be misplaced. Because 2007 was a banking crisis, people keep thinking of market downturns in banking crisis terms. The banks, because they’re leveraged investors, always experience some difficult in a downturn, and this will be no different. But it’s not a banking crisis like 2007, this is a health crisis with economic consequences."

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

1 stock mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment