One company that passed our nine-point checklist

With over 2000 companies listed on the Australian Stock Exchange, it is impossible for an individual to be adequately across all the businesses in that investment universe. Therefore, the question is, how do investors identify which businesses to invest in?

Although this may appear to be a simple question, the reality is somewhat more complicated with industry ‘experts’ and commentators exclaiming the virtues of countless different approaches to equity investments ranging from momentum strategies, chartist strategies; top down bottom up, contrarian investing and so on.

It is essential that investors settle on an approach they have confidence in, and then stick to a process that allows them to unearth a list of businesses that they can then conduct further detailed research and due diligence.

By implementing and constantly adhering to a certain ‘screening’ process, investors can narrow their focus towards opportunities that meet certain criteria. This can ultimately simplify the investment process and ensure time is efficiently allocated towards those businesses with brighter prospects.

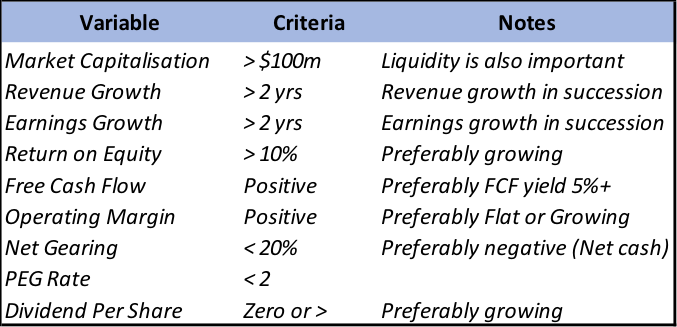

The nine-step checklist for screening for opportunities

Unnecessary complexity can invite unnecessary risks, so instead, we aim to keep it simple to achieve success. We appreciate that there are many ways to ‘skin a cat’ and some of the criteria included, or indeed excluded, are subjective.

Do bear in mind one can adjust the parameters to suit their certain preferences, but naturally less arduous parameters delivering a greater number of businesses for consideration, and vice versa. Our basic screening process involves the following:

It’s important to make it clear that just because a company passes the screening process doesn’t automatically make it a buy. In fact, the screening process is just part of the investment process.

Markets are meant to be forward-looking so once an investor identifies a list of possible candidates for their portfolio, the next step is to consider the forward outlook and the potential future compound annual growth rates (CAGR) for key variables revenue, earnings and margins.

Further considerations include business stability and industry cyclicality. For instance, those businesses with more predictable earnings streams are preferred of those with more cyclical numbers.

The reason for each of the nine checks

Below we look to breakdown the reasoning behind the inclusion of each criteria:

- Market Capitalisation - > $100m

- Perhaps the most subjective of all the criteria. Larger businesses tend to have greater liquidity allowing investors to easily enter and exit positions.

- Liquidity is also an important consideration. Individual investors tend to have an advantage over large institutional funds given their ability to be nimbler and invest in smaller businesses without affecting prices.

2. Revenue Growth - > 2yrs + successive revenue growth

- Revenue growth is important as it can shed light on the quality of earnings and profit growth. Are profits improving because of cost-cutting measures or more sustainable market share gains?

- For business growing at a rapid rate revenue can be a superior measure than earnings.

3. Earnings Growth - > 2yrs + successive earnings growth

- Whether the business is making money and becoming more profitable is important. Our belief is that over the long-term share price growth is highly correlated to earnings growth.

- We acknowledge that certain businesses will sacrifice profitability for growth particularly in earlier years as we’ve seen with the likes of Xero and Amazon. Investors need to be conscious of this and adjust their screening process if they wish to capture such names.

4. Return on Equity (ROE) - > 10% & preferably growing over time

- ROE a key measure of profitability revealing how much profit the company is making on each dollar invested by shareholders. Ostensibly if a company is generating a greater return on each dollar invested by shareholders then that’s a good thing.

- Beware however that higher leverage and debt has the effect of inflating the ROE. For that reason perhaps Return on Assets is a superior measure for highly indebted companies.

5. Free Cash Flow (FCF) - Positive

- As defined by Investopedia, Free cash flow represents the cash that a company is able to generate after required investment to maintain or expand its asset base.

- FCF is a measure used determine the amount of cash that can be distributed to stakeholders. It therefore is important measure when considering dividend sustainability.

- A positive, high and growing FCF yield is preferable as it indicates the business is generating greater cash levels.

- Negative FCF can indicate a requirement for debt to maintain operations. This may hinder profitability in outer years.

6. Operating Margin - Flat or Growing

- Operating margin is a measure of business efficiency. It essentially highlights what percentage of revenue earned remains in the business after expenses are accounted for.

- A growing Operating margin signals improving economies of scale and greater profitability.

7. Net Gearing - below 20%

- Net gearing is a similar measure to the debt to equity ratio, however net gearing takes into consideration the cash on a company’s balance sheet.

- Ideally a company will have a negative net gearing, as this indicates that the company holds more cash then debt on the balance sheet.

8. PEG Ratio - below 2

- In our opinion the PEG ratio is a far superior measure than the simplistic P/E ratio as it takes into account a company’s earnings growth.

- The lower the PEG ratio the ‘better’ as it alludes to the company being undervalued relative to its earnings growth.

- A company with a P/E ratio of 20x and earnings growth of 20% will have a PEG ratio of 1.

9. Dividend Per Share

- Whether a company is paying a dividend or not isn’t of the greatest concern to us if they are successfully reinvesting the cash for growth. Notably this preference may differ from investor to investor.

- However, if the business is paying a dividend, we’d prefer to see that dividend per share grow over time to at least offset inflation and maintain the purchasing power of that capital.

Identifiying a winner - and avoiding a loser - using the screen

The above screening process has a preference for businesses with earnings and balance sheet momentum and will therefore tend to overlook turnaround stories and cyclical business such as miners.

As an investor, you may disagree with some of the filters outlined above, but the beauty of this is that investors can tweak, add and remove variables to suit their preferences and risk tolerance. The purpose of this particular ‘screen’ is to provoke thought and provide a framework from which the investment process can begin.

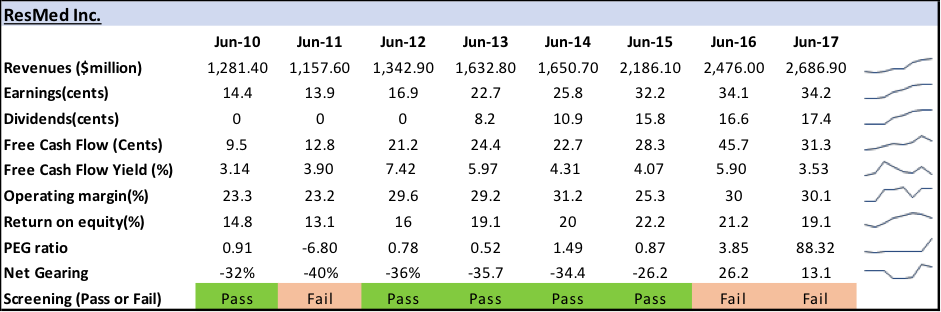

Resmed: Passing the checklist

One stock that has frequently passed this checklist over the years is ResMed Inc (ASX: RMD).

As you can see in the table above, ResMed has demonstrated consistent growth across key several key screening metrics over the past 8 years. Only on three occasions has RMD failed to pass the screening process, on each occasion due to an unfavourable PEG reading caused by slowing or negative profit growth.

Even if you hadn’t been fortunate enough to purchase ResMed (ASX: RMD) shares back in 2010, had you done so even as recently as 2015 your performance to date would still have been very impressive.

It’s important to note that just because ResMed (ASX: RMD) failed the screening process in 2016 and 2017, it doesn’t mean the company automatically becomes a sell. Occasionally there are one-off changes such as an acquisition, or capital expenditure programs that can distort variables such as Earnings Per Share and leverage for a period of time. That’s why investors cannot totally rely on a screening process for direction and still need to delve into further research to ascertain whether a specific issue is transitory, or something more permanent.

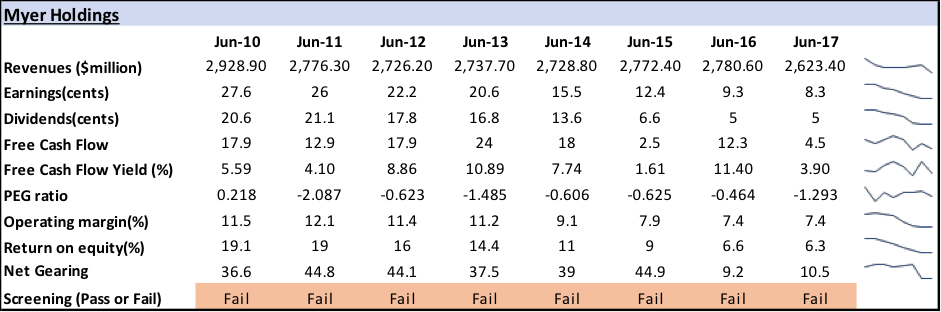

Myer: failing the checklist

On the opposite side of the spectrum to ResMed (ASX: RMD) is a business such as Myer Holdings (ASX: MYR). As you can see from the table below the business delivered a consistent deterioration in key financial metrics as the years progressed.

At no stage did Myer pass the screening process, highlighting how a simple screen could potentially help an investor avoid making a poor investment decision.

For those already holding Myer a lesson to take away from the screening process is that although you mightn’t necessarily sell something on the first occasion it fails the process, if something consistently fails to meet the criteria then it could well be a good reason to consider selling down a holding.

For instance, even had an investor held onto Myer (ASX: MYR) through to Jun-2013, although they would’ve still incurred a sizable loss by that stage, they still would’ve avoided further significant loss in the ensuing years had they considered the repeated screening ‘fails’, bitten-the-bullet, and sold.

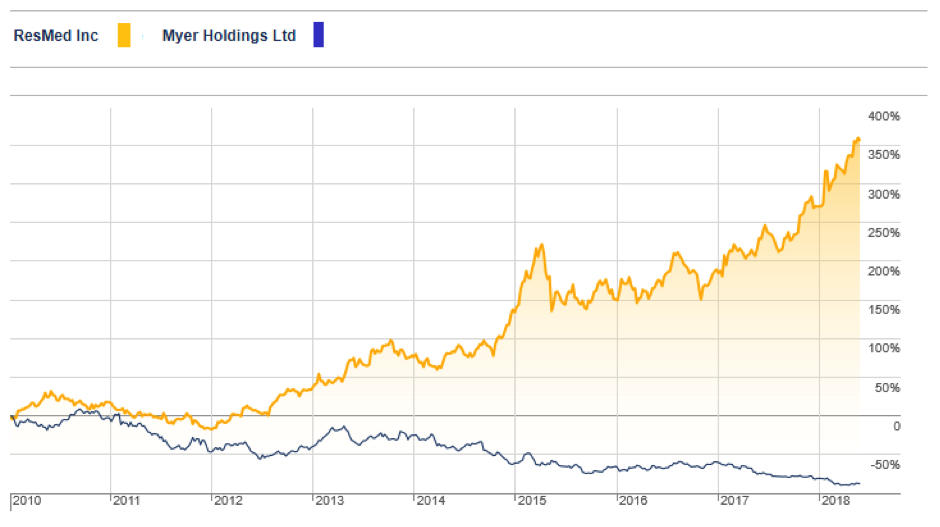

Divergent long-term performance

The price chart below highlights the enormous difference in price performance between the two businesses. Although this may be interpreted as an extreme example, the stark contrast in both balance sheet and share price performance helps to simply illustrate the potential benefits of following a process and screening for quality.

Share market strategies are often convoluted, but in our opinion, investing in the share market doesn’t need to be overcomplicated. As a general rule, we believe investors should focus on simplifying things by investing in fundamentally sound businesses that have bright prospects and sustainable business models.

Investors can use the aforementioned screening processes to help identify those traits and characteristics that make up a successful business so that they can be highly selective before purchasing new holdings for their portfolio.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

2 stocks mentioned

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Comments

Comments

Sign In or Join Free to comment