A stark risk reminder

Well, what a difference six months can make… I can remember thinking just a few short months ago that if the global strategists were right and the consensus was correct, 2020 was shaping up quite nicely and, although stretched, the bull market might just ride out another year.

Today, we’re staring down the barrel of a very different and sobering new reality, with the prospect of recession or depression – conditions not seen since the last World War. Capitalism, credit markets and humanity have suffered a stark risk reminder, this time biological, and we’ve all been humbled by the economic and human loss COVID-19 has caused over the last three months. At this stage, it’s very difficult to estimate the fallout from the pandemic as death tolls, job losses and global debt levels continue to climb around the world. There are just so many unknowns.

Early on in the crisis, we saw impacts to travel, retail and airlines, but that quickly spread to value chains as lock-downs, closed factories and border closures disrupted logistic channels. By March, the economic impacts were becoming much more visible. The pandemic was changing our whole system of living as schools and businesses closed and social distancing measures were widely implemented.

It’s been a harsh ‘reality bites’ moment worldwide and with it has come the repricing of risk in equities and bonds.

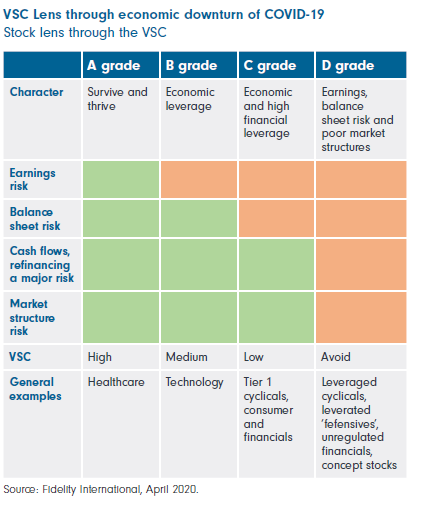

If we look back to 2019, ‘momentum’ extremes were already fading. Concept stocks, unicorn boom valuations such as Uber or WeWork were much more challenged over the last 12 months. But in the current environment, the shift back to fundamentals (balance sheet strength, cash flow certainty and liquidity) has moved from a low priority to a top priority in a matter of months. Long duration drivers of success are today beginning to matter much more – viability, sustainability and credibility are for some a driver of earnings and valuation, while for others, a factor determining survival.

When it comes to stock selection, I tend to use a framework of grading stocks through the Viability, Sustainability and Credibility (VSC) process lens, as per below. Currently I’m seeing some good opportunities in grade B and C, but remain cautious of companies in grade D.

Going forward, I think there will be valuation opportunities that arise in the traditional long-term clusters of future leaders – global healthcare, global technology, tier 1 global cyclicals and global consumer brands.

Navigating through the current environment

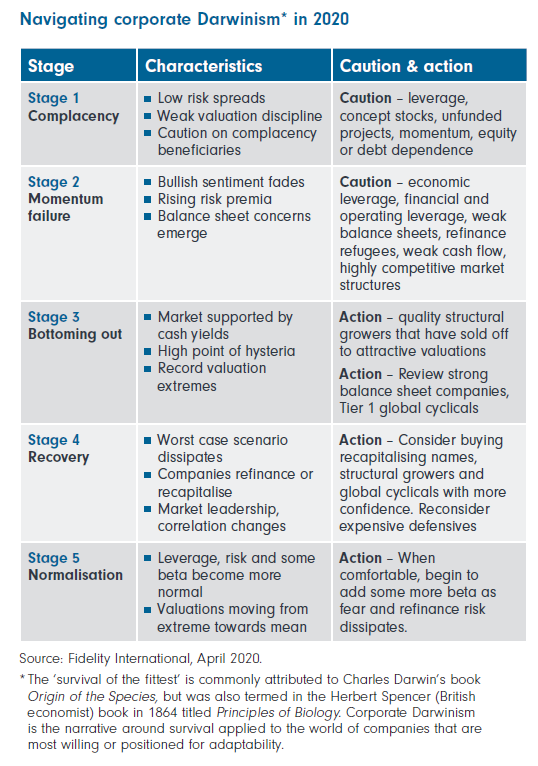

I’m having a lot of conversations with clients about how best to navigate through the current environment. In my view, now is not the time for complacency, as I don’t think we’re through the worst. Over the next four to six weeks, we’ll likely see a bottoming-out as the balance sheet recapitalisation process continues, unemployment numbers begin to rise and the tests of lifting social distancing rules provide a firmer guide of the path toward normalisation.

Surviving a correction

If some of the concerns of the last few years, (emerging market debt, high yield bonds, unfunded pension funds, European banks, to name but a few) are realised into a global liquidity event or economic recession, then risk will quickly re-price and sustainability will become the central question for financial markets, but also for governments.

As some of my Fidelity colleagues have noted, ‘History doesn’t repeat, but it does rhyme’, and so the lessons of previous corrections and market dislocations can help in navigating these very difficult times. Cash is king. Quality matters. Sustainability is critical.

Want the latest news on Australia's future leaders?

The challenge is to identify those that are headed for a bright future and separate them from those more likely to fade into the background. The Fidelity International Future Leaders Fund was recently awarded the 2020 Australian Domestic Equities Small Cap Fund of the Year for the third year running. Click 'contact' to get more information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James has been portfolio manager of the Fidelity Future Leaders Fund since 2013, after joining Fidelity in 2003. Prior to that he worked at Constellation Capital Management, BNY Equities and Ernst & Young. James holds a Master of Commerce.

James has been portfolio manager of the Fidelity Future Leaders Fund since 2013, after joining Fidelity in 2003. Prior to that he worked at Constellation Capital Management, BNY Equities and Ernst & Young. James holds a Master of Commerce.

Expertise

James has been portfolio manager of the Fidelity Future Leaders Fund since 2013, after joining Fidelity in 2003. Prior to that he worked at Constellation Capital Management, BNY Equities and Ernst & Young. James holds a Master of Commerce.

Expertise

Comments

Comments

Sign In or Join Free to comment