April Market Commentary: Markets are Invincible?

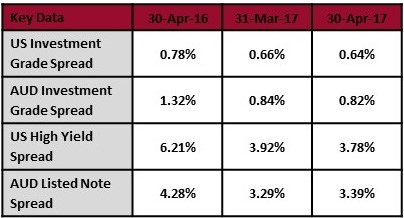

Small gains were made in equities and credit during April whilst commodities were mixed. Equities rose in Europe (1.7%), Japan (1.5%), Australia (1.0%) and the US (0.9%) with China (-0.5%) the odd one out. High yield and investment grade credit made small gains as well. US natural gas (2.5%) and gold rose (1.5%), US oil (-2.9%) and copper (-1.5%) fell but the standout mover was iron ore (-14.4%). Moves by the Chinese regulators to reduce speculative buying, combined with growing stockpiles and supply growth brought about the long expected pullback in prices.

Market Sentiment

Markets started out sluggish in April but came home strongly with the promise of Trump’s tax reforms helping the US and the outcome of the first round elections in France helping Europe. Also positive were small upgrades to global growth forecasts and the stronger than forecast first quarter GDP reading of 6.9% for China. The first quarter US GDP reading of 0.7% was awful, but economists are hoping that will be turnaround bigly if Trump can get through stimulus and tax reform measures. US employment measures continue to strengthen, with the headline readings indicating near full employment putting pressure on the Federal Reserve to continue to raise the overnight rate. Markets are even pricing in a better than 50/50 chance of a small ECB rate hike in the next 12 months. It does seem that markets are invincible for now, blowing off negative news and rallying on positive news.

US retail and restaurant sales continue to struggle with bankruptcies for US retailers this year already above the total for 2016. Excessive personal debt, higher minimum wages and the relentless increase in the cost of healthcare are all part of the problem. The fact that sectors that typically benefit when the US economy does well are struggling now indicates that the average American isn’t doing as well as long term GDP forecasts and job numbers would indicate. Rising credit card charge-offs confirm that. The 10.8% fall in the US classic car index over the last year indicates that wealthier Americans might not being doing so well either. Americans with the highest incomes are the cohort most likely to think they will default on a loan payment in the foreseeable future.

Valuations for equities remain elevated, just one example being the global enterprise valuation to EBITDA ratio at a 20 year high. Global earnings upgrades beat downgrades for the first time in six years. Strong earnings growth in recent years defies the long term trend and raises the question whether earnings as well as P/E ratios are both vulnerable. A record M&A enterprise value to EBITDA ratio, well above levels before the last crisis, shows the bullish sentiment, the impact of cheap debt and the lack of organic growth opportunities for US corporates. The Wall Street Journal sees the current environment for US equities as a mix of the 2000 and 2007 bubbles.

The classic Warren Buffett saying, “what the wise do in the beginning, the fool does in the end” is playing out for US retail investors. There was a record number of new stock accounts opened in the first quarter and there’s more optimism than there has been for a decade. Margin debt levels are setting records again, and the most quoted figures might be significantly understated as security backed loans aren’t being counted. Margin debt levels have been likened to “gasoline in search of a match”. Hedge funds are loving leverage again and banks are more than happy to help them lever up. The memories of losses from forced leverage unwinds in 2008 has faded quickly.

There’s plenty to worry about with debt, global debt levels are growing quickly with emerging markets (predominantly China) seeing the highest growth. The first quarter of 2017 saw a surge in US high yield issuance, driven by refinancing as corporates took advantage of low rates and loose terms. CCC rated debt posted big gains in the US and Asia. A $2.1 billion CLO was funded in April, the largest since the financial crisis. This time around UBS sees subprime lending most prevalent in auto, credit cards, student loans and personal loans. The subprime pet lending business, Wags Lending, has filed for bankruptcy.

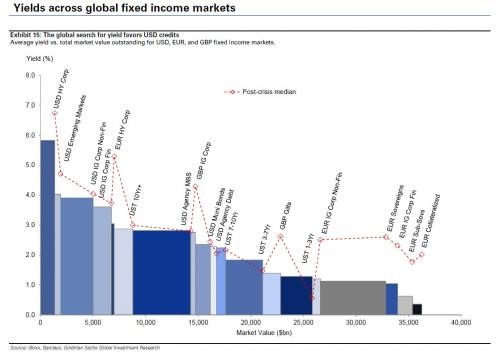

There’s more evidence of yield chasing as US investors are flocking back to local currency denominated emerging market debt. The extra yield looks good a for a while, until you get burned on the currency and the credit risk, usually at the same time. Jeffrey Gundlach warned about the record long duration positioning in bond markets. Goldman Sachs highlighted the chase for yield with the graph below, showing that yields across almost all debt classes in the US and Europe are well below their post-crisis median.

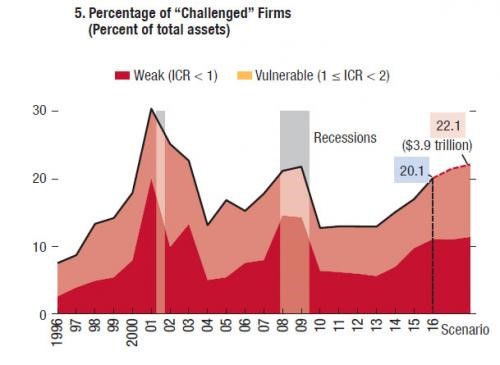

Morgan Stanley looked at US corporate debt levels and found that relative to earnings and cashflows debt is at record highs. The IMF also looked at US corporates and produced a cracking graph highlighting that interest coverage ratios are stretched again. When there’s a large pool of weak borrowers the credit cycle is in its late stages.

One of Canada’s big banks is offering the first uninsured residential mortgage backed security seen there for a long time. It contains substantial refinancing risk, as the underlying borrowers need to be reapproved or refinanced every five years. 54% of Canadians think house prices will rise indefinitely. Drawing on lessons from the US housing debacle here’s five signs Canada’s property market is in a bubble. The shares in a Canadian subprime lender fell 65% after it disclosed it was having funding issues and its credit rating was downgraded from BBB- to B+.

China

The headline result during April was the 6.9% GDP growth for the first quarter, which beat expectations. As usual, record credit growth fuelled infrastructure spending with the growth mostly coming from old economy industries. The mainstream view is the business cycle is ok for now but the financial sector is weak. Far more interesting but less noticed was the government tapping the brakes on the liquidity it provides via bank funding. Shares sold off, iron ore prices collapsed and the cost of debt rose. Chinese banks pulled back on entrusted loans as they struggled to get the funding they needed and regulators starting asking questions about what exposures they had. What looked like a fairly minor move from the central bank had substantial ripple effects on asset prices.

One thing the government has been able to bring under control is the capital outflows. Inflows haven’t changed much but outflows have fallen with multinationals now complaining they can’t get funds out. That works in the short term, but in the long-term multinationals will allocate their capital elsewhere reducing economic growth. The government has issued a warning that it won’t backstop wealth management products but investors don’t believe it and keep piling in. The former finance minister says local governments should be allowed to default without bailouts. ”Off book” government debt is thought to be nearly as big as official government debt. Local government debt issuance has fallen 77% this year as investors have become concerned and shifted to corporate debt.

Investors chasing yield have compressed the spread between lower and higher risk corporate debt to the lowest in nine years prompting one manager to tell investors to sell their riskier debt. Another reason to sell is the record pace of bond defaults in 2017. Bloomberg reported that internal risk controls are almost non-existent at Chinese companies. An example is the widespread practice of making undisclosed guarantees for debts of other companies, which could create a cascading wave of defaults. Highly indebted property developer Evergrande has embarked on a stock buyback binge in a battle against short sellers. Moody’s sample of Chinese companies has 20% with EBITDA less than their interest. On aggregate, it has the debt to EBITDA ratio at a CCC level and the EBITDA to interest ratio at a B level.

Following the share price collapse last month, HSBC has called an event of default on Huishan Dairy and frozen its assets. Huishan has total debts of $5.8b including securities sold to retail investors. Customers of Minsheng Bank have lost $436 million after a bank manager issued fake wealth management products and stole the money. The world’s largest aluminium producer has been underreporting expenses and is now at risk of defaulting on $10 billion of debt.

Banking Bad

Wells Fargo was back in the spotlight as it publicly released a 113 page report into the cross-selling scandal in its retail division. The old CEO and head of the retail bank were fired and have now been docked $47 million and $28 million respectively. The current CEO was largely unscathed. As part of the clean-up process Well Fargo has hired back about 1,000 former staff, many of who are likely to have been forced out for failing to participate in dubious practices or who reported the misconduct. Four Wells Fargo directors nearly got the sack from shareholders at the AGM. The US banking regulator is feeling the heat too after it ignored 700 whistleblower complaints from Wells Fargo employees.

The clean-up of this mess could take quite a while and cost a lot more, in one court case Well Fargo has been ordered to pay $5.4 million and reemploy a whistleblower it sacked in 2010. Barclays CEO is also in trouble for his treatment of a whistleblower complaint. His board docked his pay after he attempted to track down the complainant.

The efforts made by Wells Fargo to clean up its mess aren’t perfect but they are a lot better than what has been happening in Australia. ASIC has been shown to be the corporate watchpuppy yet again with emails released showing that it allowed banks to edit its own press releases on their misconduct. In one case, ASIC thought the investigation by accountants EY was a sham, but failed to report that publicly.

Funds Management

The weight of articles and fund flows can make it seem like index funds and ETFs will eventually overrun all active management. Index funds have certainly made great strides but so far are mostly focussed on the low hanging fruit of the most liquid and transparent sectors. The concept that it is very hard to beat the index after fees in large cap US equities is generally accepted. With so many fund managers and analysts covering this sector the opportunities for finding new, profitable insights is limited. However, index funds have yet to prove themselves where information is constrained and informed institutional investors are the minority. Small capitalisation equities in Australia are an obvious example; if you buy the index you will almost certainly underperform a randomly picked manager.

It is increasingly recognised that index investing is a very different proposition when it comes to debt. Debt matures so there is a natural turnover of capital in debt portfolios. New issues offer slightly higher yields compared to existing securities to attract buyers. Debt indexes are concentrated on issuers that raise the most debt, which is a different construct from an equity market capitalisation index based on what investors think are the most valuable companies.

Another key component is liquidity; debt markets generally reward investors in illiquid securities with higher returns. The best returns come from investing in small syndicates and bilateral deals which index funds don’t participate in. Where debt index funds have shown strong market share gains is in government and investment grade debt securities, which derive most of their yield from the interest rate component rather than credit risk or the illiquidity premium. A private debt manager has a huge illiquidity premium as a head start over index funds and over the long term is very likely to cover their fees several times over.

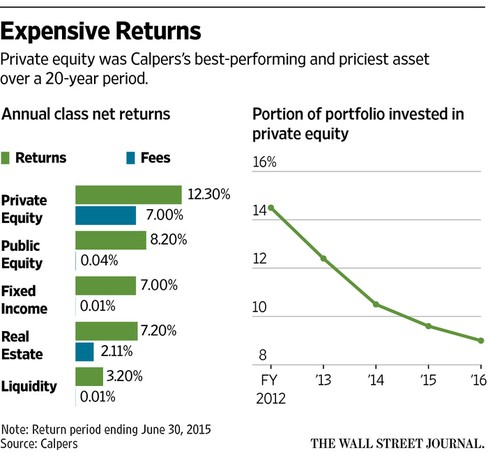

Private equity also has the potential to outperform a generic equity index, but the case is far less clear. The chart below from the Wall Street Journal shows the net returns achieved by Calpers over the last 20 years. Private equity has clearly beaten public equity, even after an enormous fee gouge. However, private equity is notoriously difficult to compare as there are contributions from market timing (buy low, sell high), leverage and illiquidity premium in the returns.

Real estate and infrastructure are sectors where I haven’t seen any data to make a comparison between active and passive management. What I do know from experience is that just like debt, smaller assets tend to attract less competition and offer more opportunity for outsized gains when actively managed. A classic value add strategy for real estate is buying an underutilised building, improving the facilities, signing long term tenants, then selling at a much improved valuation. This is an active approach that harvests gains from more passive investors.

Even with this cursory analysis it is obvious that there is likely to be a permanent place for active management in many sectors. The desire to reduce fees is a noble aim, but if investors are giving away far larger amounts of alpha that’s a fairly dumb decision. Yale has responded to critics calling for it to spend less on management fees noting that if it had prioritised lower fees it would have missed out on billions more in returns. At the other end is North Carolina, which is planning to direct all of its $90 billion to index funds.

Another increasingly popular strategy being called out is risk parity, with Paul Tudor Jones saying it could cause a big sell-off like the failed LTCM strategy did. Others are saying smart beta is fad, based on tortured data. AQR has made its name on both of those strategies and argues that its favoured factors have succeeded in the past and will continue to succeed in the future. AQR’s brand has been tarnished by its managed futures fund which has seen massive growth in assets under management but has posted negative returns over the last 2 years. Jack Meyer did a great job picking managers when running the Harvard endowment, but has lost money five years in a row running a hedge fund. People are worried about tourist investors in emerging market ETFs and venture capital, which could flee for the exits at the first sign of trouble.

The first quarter was a massive one for capital raisings in private equity and private debt. The sheer weight of money headed to private equity means firms are largely immune to fee pressures. Investors should expect that high purchase valuations and the huge amount of capital being allocated will make future returns lower than historical returns. Hedge funds are earning less in fees, but that is mostly due to their poor performance rather than investors insisting on better terms. Commodities have struggled to gain acceptance as a mainstream asset class with critics pointing to complexity, volatility and lower returns.

Emerging markets

The Greek debt melodrama has moved onto another act but the storyline is still the same. The IMF wants Greece to undertake deep structural reforms calling what has been done so far “just a down payment”. Greece points to the surplus it produced in 2016 which the IMF says was inflated by slowing down payments to creditors. The inevitability of a debt haircut continues to be ignored by the Europeans. If Greece was to refinance debt in the capital markets its interest bill would soar and the debt to GDP ratio would only move higher.

Venezuela made the April payment for its oil business with the next big repayments due in October and November. A cargo ship containing Venezuelan oil was seized to cover shipping fees owed to a Russian company. Puerto Rico’s protection from creditors ends on May 1 and bankruptcy is expected. Multiple sides are arguing for priority and there isn’t nearly enough money to go around so it looks inevitable that a judge will be needed to sort this out. Another restructure of the territory’s utility debt was agreed with principal repayments kicked further down the road.

The IMF is worried about corporate borrowers in India, Indonesia, Turkey, Brazil and China. Corruption and higher debt levels are problematic for Mexico. The Frontier index is being hollowed out as Pakistan, Nigeria and Argentina are set to graduate to emerging market status. Zimbabwe is forcing its banks to accept cattle as collateral for loans.

Media Worth Consuming

The UK had its first day without coal power for over 100 years, as gas, renewables and nuclear now fill the gap. It has come at a price though with UK industry paying amongst the highest prices in Europe for electricity. Cutting the cost of batteries is the key to making electric cars competitive without subsidies. A hydrogen truck is being tested in California sporting a 200 mile range. Power producers are betting that wind turbines won’t require a subsidy by 2025.

Millions of American millennials are living with their parents and not working or studying. Before whinging about millennials consider whether Baby Boomers are any better in their sense of entitlement. 44% of recent US college graduates are in jobs that don’t require degrees. Two-thirds of potential assembly line workers were screened out for failing maths or drug tests. Some economists think minimum wage increases have little or no impact on employment, too bad the data from San Diego and a Harvard study says otherwise. Tax cuts lift the incentive to work more for the poor than the rich. New Zealand has the lowest tax rates for average earners in the developed world.

Japan has auto-filled tax returns, why can’t Australia and the US? Is Japan better off than the US with its higher employment levels? Convenience stores in Japan have to automate as they are struggling to get enough employees. None of Japan’s 4000 listed companies went bankrupt in 2016, indicating banks are playing extend and pretend.

Trump gave America a change in style but not substance, he has now backed down on five big promises and chosen war over economic reform. Which big insurer will pull out of Obamacare next? Rhode Island cut healthcare spending and still improved outcomes. Bloomberg and the New York Times sat on evidence that the Obama Whitehouse was spying on Trump’s team but the story got out anyway.

The war on drugs is counterproductive, it has increased death, disease and violence. Here are the statistics on the mainstreaming of marijuana in the US. A tough love drug rehab clinic is getting addicts into work and off drugs. New Jersey prohibits food made at home being sold – another case of nanny state, crony capitalism. Saudi Arabia has been voted onto the UN panel for women’s rights despite an appalling record for its treatment of women. A lady misunderstood what “Furry Con” is, but raised $10,000 for a charity anyway. A brutally funny review of an overpriced French restaurant. Diamonds might be the greatest investment scam ever. Facebook makes you feel worse, real relationships make you feel better. The four behaviours that mark out productive CEOs.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

_YB16.png?utm_source=livewiremarkets.com&utm_medium=referral){kind=link}

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment