Are the Pieces Falling into Place for an RBA Rate Rise?

The consensus view is that it is unlikely that the Reserve Bank of Australia (“RBA”) will act to raise cash rates in 2018. While not all the pieces are in place yet to justify a rate rise, it may not take that much to get the RBA over the line.

The key to determining what any central bank will do is understanding its policy reaction function and the range of factors which impact upon their objectives when setting monetary policy. The objectives for the RBA are set out in the Reserve Bank Act of 1959 and include:

- The stability of the currency of Australia;

- The maintenance of full employment in Australia; and

- The economic prosperity and welfare of the people of Australia.

From the early 1990’s, these objectives have found practical expression in a target for consumer inflation of 2-3 per cent per annum.

When trying to gain an insight into a central bank’s policy reaction function it can be useful to review the economic conditions leading up to previous tightening cycles. Since 2000, there have been three tightening cycles undertaken by the RBA. Therefore, we have chosen to focus on the economic growth and inflation conditions in the 12 months prior to the RBA’s initial increase in interest rates for each tightening cycle.

Why focus on just these two factors when there are also other objectives? Basically because “stability of the currency” and “economic prosperity and welfare” can be viewed as much longer-term objectives which are encapsulated within achieving the inflation target; i.e. achieving one objective means that you will achieve the other objectives. The same cannot be said for the interaction between full employment and inflation. Central banks may often find that there is a clearer trade-off between the two outcomes which must be more explicitly balanced within their policy reaction function; e.g. lowering inflation may require the central bank to set policy to explicitly raise the unemployment rate above full employment.

Objective 1: Maintenance of Full Employment in Australia

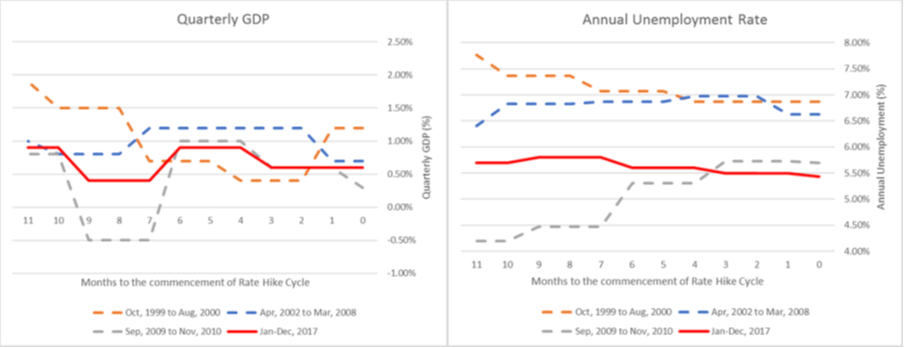

Chart 1 :

Full employment is difficult to determine and is often only evident after the fact. For this reason, the analysis focuses more on unemployment rates and real GDP growth. Growth and unemployment rates have varied prior to the commencement of each tightening cycle. However, the current unemployment and GDP growth rates are strikingly similar to those prevailing prior to the most recent tightening cycle in 2009 (Chart 1). This suggests that, in terms of growth and labour market ’tightness’, current economic conditions more than justify the RBA taking steps to correct the policy misstep of 2016 by commencing to raise rates.

Objective 2: Target for consumer inflation of 2-3 per cent per annum

To date, it is the lack of any material pickup in inflation which has prevented the RBA from feeling under pressure to reverse the rate cuts of 2016. Yet when considering the impact of inflation (here measured by the RBA’s mean trimmed Consumer Price measure) on RBA policy it pays not to interpret the RBA’s target too literally.

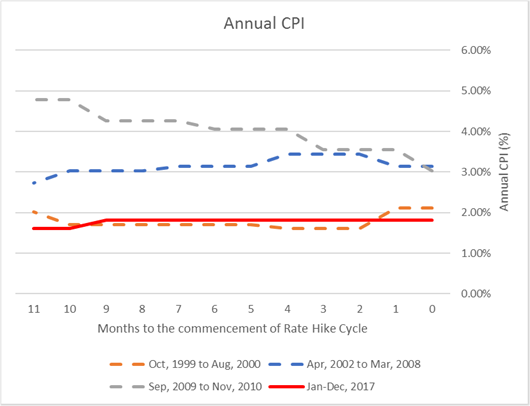

Often the 2%-3% inflation target will be interpreted to mean the rolling 12-month inflation reading or “year-on-year” inflation. Based on such an interpretation, with year-on-year inflation below 2%, there would appear to be little pressure on the RBA to raise rates any time soon. Yet such an interpretation of the inflation target risks being too narrow. Contrary to what many may expect the RBA has not always waited until the year-on-year CPI measure is towards the top of the inflation target before starting to raise interest rates. This was highlighted by the 2009 rate rise cycle (Chart 2) which began with the CPI at the bottom end of the target band and not far off current levels. The reason for this is that the RBA takes a forward-looking view of inflation. Accordingly, while year-on-year inflation may be at the bottom end of the target range this generally has not in the past necessarily acted as an impediment to the RBA raising rates.

Chart 2 :

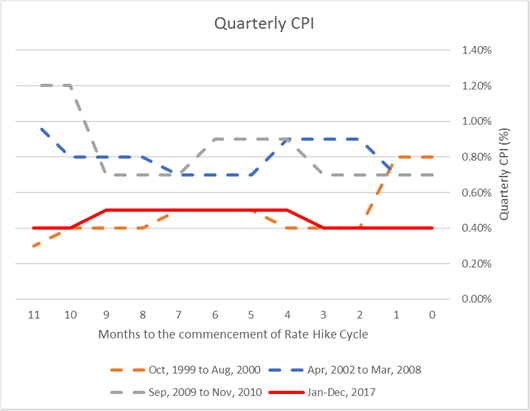

When judging the future path of inflation what appears to be more important to the RBA is the direction of the more recent quarterly CPI readings (Chart 3). Past behaviour would suggest that if the annualised quarterly CPI readings are well and truly within the upper half of the target range (above 2.5% annualised) this can serve as sufficient justification for raising rates even if the year-on-year inflation rate is still at or below the bottom end of the inflation target. It therefore would not appear to be a coincidence that prior to the commencement of each tightening cycle the latest quarterly CPI was between 0.70%-0.80% per quarter or 2.8%-3.2% annualised. If it simply takes one or two quarterly CPI readings within the upper end of the inflation target to justify taking back the rate cuts of 2016 then the inflation hurdle may be materially lower than many may be anticipating.

Chart 3 :

What are the red flags to look out for regarding a rate rise by the RBA?

Overall, the current low rates of inflation provide the RBA with adequate grounds to maintain a more accommodative stance to monetary policy. However, judging from the commencement of past tightening cycles, the hurdles in the way of a rate rise may not be as great as many may think. The key watchpoint is an increase in the annualised rate of quarterly inflation to above the mid-point of the target inflation range of 2%-3%. With the policy misstep of 2016 serving as a backdrop it may only take a relatively modest pickup in the quarterly CPI readings to get the RBA over the line in terms of raising rates.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

1 topic

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management