Australian equities look attractive

Although we are now recommending clients lock in some gains on international shares, globally Credit Suisse believes investors should hold a higher than average allocation to Australian equities. We have been buying Australian equities since the beginning of April but still see upside. That said the next month or two may see some weakness, so those looking to add should get the opportunity.

Based on consensus expectations, financial year 2020 earnings are expected to decline by 20%, approximating what occurred during the GFC. A lot of bad news has been factored in. But like the GFC, earnings are expected to recover - by 8% in 2021 and 13% in 2022.

ASX 200 Earnings Index – Based on Consensus

Source: Credit Suisse, Data Stream

Not only are earnings expected to recover, but there is evidence that earnings upgrades are starting to filter through, as companies gain confidence in forecasting future earnings and economic data is not as bad as previously feared. The retail sector has been surprisingly strong as consumers spend superannuation withdrawals, receive government support and buy the infrastructure to enable work from home. The large miners are due upgrades based on spot iron ore prices. Energy producers should also see upgrades based on the current oil price. Even the banks appear to at least be meeting expectations as bad debts are contained so far. We believe economic and earnings data will continue to improve as the economy opens up. Australia’s sterling effort in controlling the virus, leverage to China which is essentially back to work, and massive fiscal and monetary support, should continue to see an improved earnings outlook.

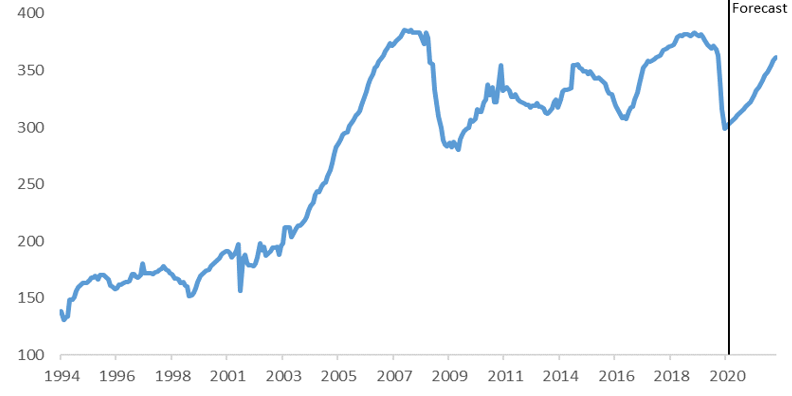

But, Australian equities have already recovered nicely. The ASX 200 has risen 31% since its March low. Capital gains have occurred against the backdrop of earnings per share (EPS) downgrades, such that the market's price-to-earnings (PE) multiple on a 12-month forward consensus basis has risen disproportionately to almost 19x. Investors have now started to question whether the market has become too overbought, if not too expensive. To be sure the easy gains have been made, but the rise in PE is very similar to the GFC experience as the recovery got underway. PE’s early in an earnings recovery should be high. Admittedly the PE is higher than the recovery phase of the GFC, but very low interest rates do justify a higher PE going forward, as the discount rate applied to future profits is reduced. Historically, PE falls with earnings recovery rather than a decline in share prices.

Australian Equities PE 12 Month Forward

Source: Credit Suisse, Data Stream

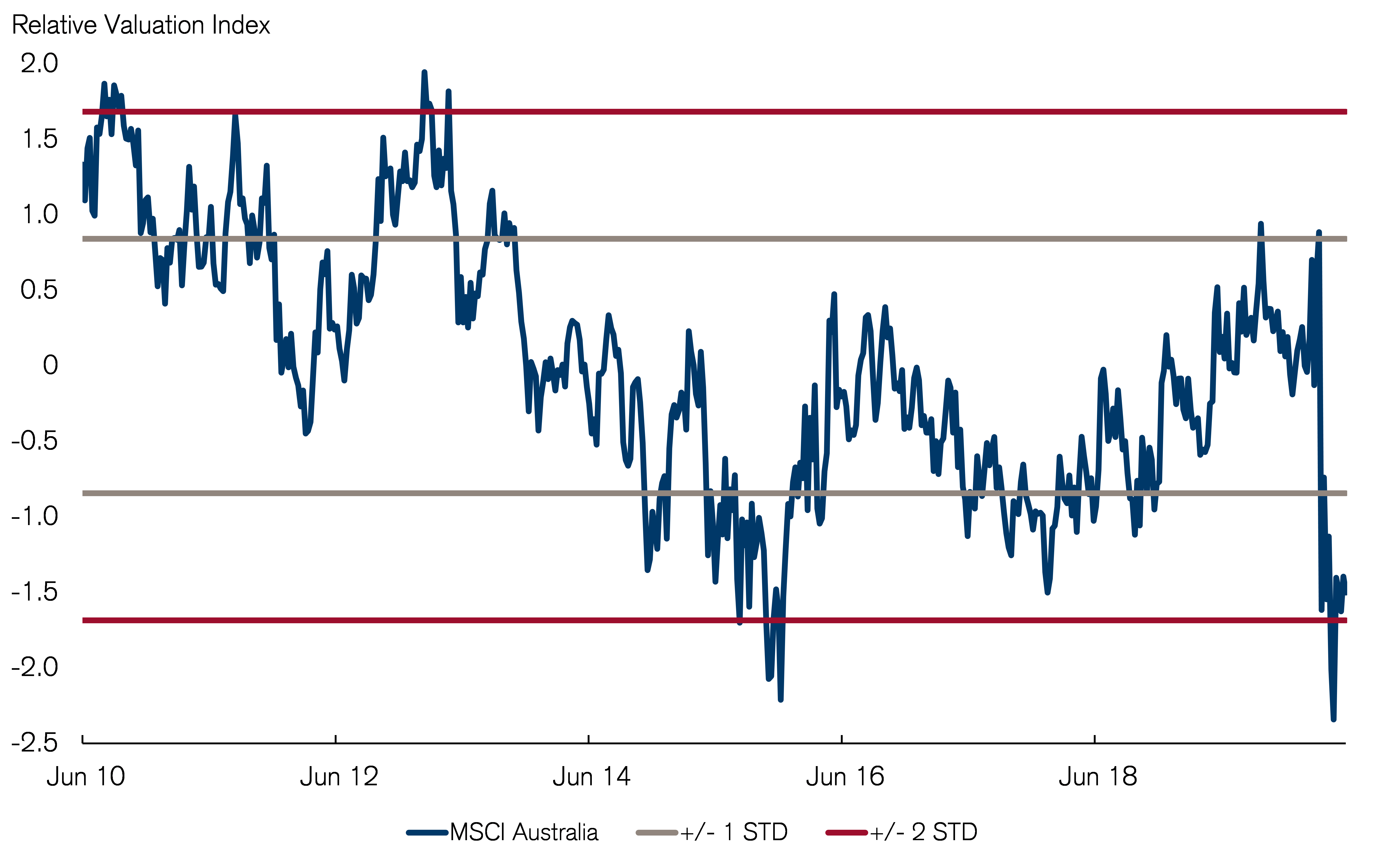

Apart from showing some absolute upside in the medium term, we also think Australian shares look attractive relative to international shares. Below is a graph of an index we created to track relative valuation of Australian equities versus international. It takes an average of PE, price to book and dividend yield and compares it to the rest of the world.

Relative Valuation – Australian Equities Versus International

Source: Credit Suisse, Data Stream

The index shows Aussie shares are trading almost two standard deviations cheaper than normal relative to international shares. The last time Australian shares looked so relatively cheap, at the beginning of 2016, they outperformed for six months, led by the miners.

The miners look well positioned to us and our discretionary portfolios hold an overweight position in the big three iron ore producers. We have also been slowly adding to our banks exposure due to attractive comparative valuation on a historical basis, and the view that a very poor scenario has been priced in that won’t eventuate. RBA action to anchor medium term rates at a low 0.25% has seen the yield curve steepen which should support loan margins. We have a core of quality growth stocks in the Healthcare sector and are underweight A Reits, and in particular retail mall owners which face structural and cyclical headwinds pre and post Covid-19.

As always, there are risks to our view. A poorer than expected outcome as to Covid-19 cases and reintroduction of restrictions may see markets leveraged to global growth like Australia sell off sharply. Fiscal policy is due to run out in September, creating a cash cliff for households. We think the risk of this can be managed as the Federal Government has shown a willingness to introduce or extend programs. The US election is four months away and announcements from the two candidates could see weakness. Overarching these risks are central banks taking a “whatever it takes” approach to support the recovery.

At every point in time markets have risk, but for the moment the positives outweigh the negatives for Australian equities.

Learn more

Credit Suisse Private Banking specialises in asset diversification, holistic wealth planning, next generation training, succession planning, trust and estate advisory, philanthropy. Stay up to date with our latest insights by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

1 topic

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment