Australian inflation-linked bonds: inflation protection but also potentially a 'double-edged sword'

One of the key attractions of inflation-linked bonds (ILBs) is that they provide explicit protection against an increase in inflation. This becomes particularly relevant in the current environment where central banks are intervening in nominal bond markets. However, the potential inflation protection provided by inflation-linked bonds shouldn’t blind investors to the potential that they could be a ‘double-edged sword’.

The Relationship Between ILBs and Nominal Bonds

ILBs provide investors explicit protection against increases in inflation as the price is indexed to reflect realised inflation, thereby providing investors with a fixed real value. Whether an ILB provides better protection against inflation than a Nominal bond (Nominal), i.e. a bond where the payments are of fixed amounts, really comes down to the level of inflation, or inflation expectations, incorporated in Nominal prices. It is this difference between actual inflation and inflation expectations which determines the relative attraction of Nominal versus ILBs. To better understand the dynamics between the two types of bonds, it helps to consider some simplified relationships.

As a starting point, the realised return on an ILB is made up of a real yield (RY) and actual inflation (∆P) :

ILB = RY + ∆ P

By comparison, the return on a Nominal is fixed at the time of purchase so its yield comprises the same real yield as an ILB but, rather than actual inflation, it incorporates expected inflation (Exp (∆P)). This means that a Nominal yield comprises:

Nominal = RY + Exp (∆P)

Linking Nominal and ILB yields together is expected inflation which, though it cannot be directly observed, can be inferred. Inflation expectations can be inferred because at any point in time an investor can observe the real yield on an ILB and the yield on a Nominal. The difference between these two yields, of similar tenor, is referred to as the Break Even Inflation Rate (BEI). The BEI is an indication of the expected inflation over the life of the two bonds. It follows from these relationships that the yield on an ILB and Nominal will be equal when:

∆ P = BEI

where

BEI ≈ Exp (∆P)

Where there is equivalence, then ILBs and Nominals will provide investors with the same level of protection against the current level of expected inflation. The proviso is that actual inflation must be the same as expected inflation or the BEI. Where actual inflation is below/above the BEI, then ILBs will provide an inferior/superior return to Nominals.

Yield Curve Targeting May Distort Nominal Bonds

The interesting nuance which arises in the current environment is associated with the monetary policies of the Reserve Bank of Australia (RBA) being conducted via the Nominal market. By targeting the nominal yield curve for the conduct of monetary policy, the RBA runs the risk of distorting the relationship between Nominals and ILBs. To better understand whether the current conduct of monetary policy is distorting the relationship, it is useful to start by comparing the BEIs with expected inflation. There are two ways this can be done. The first is to compare the BEI with the RBA’s inflation target of 2%-3%; i.e. an average inflation rate of 2.5% over the cycle. The only issue with such a comparison is that the RBA has consistently undershot its inflation target for an extended period, which makes such a comparison largely academic. Given this persistent undershooting by the RBA, an alternative, and in the current environment arguably preferable approach, is to compare the BEI with actual inflation surveys.

With the current BEI in line with inflation surveys, this suggests that the current level of distortion associated with yield curve targeting in Nominals is quite limited.

ILBs as Inflation Protection

That there is a lack of distortion in an environment where inflation pressures are low does not mean that distortions cannot occur going forward. One of the key ones which investors appear to be wary of is the impact of rising inflation in an environment where the RBA is maintaining yield curve targeting. Such a scenario can be considered as a ‘stagflation’ environment where real growth remains low and inflation rises. Under a ‘stagflation’ scenario, investors will be seeking out inflation protection. Unfortunately, as low real growth means that they may remain depressed by the RBA’s yield curve targeting policies, Nominals are less likely to provide efficient inflation hedges. Inevitably, investors will need to look to ILBs for inflation protection. Yet the relatively low supply of ILBs is likely to result in real yields being pushed lower as equivalence between ILBs and Nominals is maintained. Even if real yields do not get pushed lower, the incorporation of the higher level of inflation into ILB yields should provide a level of outperformance versus Nominals. Accordingly, the attraction of ILBs as an inflation hedge derives not from a current distortion but from potential distortions should inflation begin to rise materially.

Beware The Double-Edged Sword

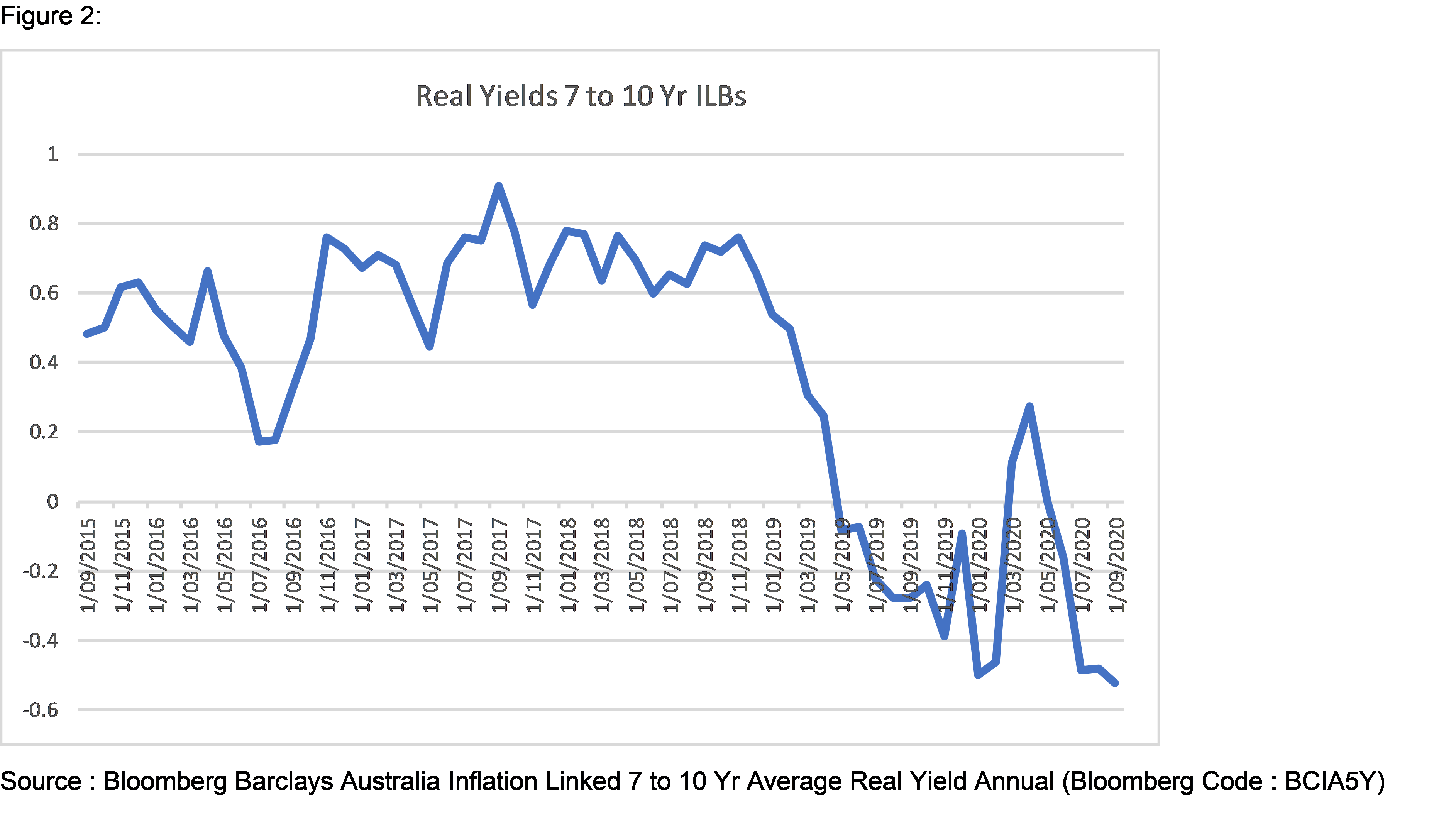

Yet such a focus on inflation risks overlooks that there is another key component to bond returns, which is real yields. The real yield is a common factor to both ILBs and Nominals and, with all else being equal, should be the same for each class of bonds. Investors therefore need to not just consider inflation but also the level of real yields when considering the attraction of ILBs. Such a consideration is particularly relevant as real yields are down around historical lows (see Figure 2).

When considering the current level of real yields, it is important to take account of the range of factors impacting on them, including real growth, cash rates and investor demand for safe assets. Given this range of factors, it is not surprising that at this point in the cycle the real yield would be around ‘all time’ lows. What is equally clear is that a lot of these factors are potentially transitory in nature.

The transitory nature of the factors depressing real yields lays open the potential for an alternative scenario under which ILBs underperform Nominals. This may be considered as the ‘Normal Economic Cycle’ scenario. Under such a scenario, real growth, and investor risk appetite, recovers first with inflation beginning to pick up as the rebound in real growth closes the output gap. Only after the rebound in real growth has sufficiently closed the output gap will inflation begin to be pushed higher. Should this scenario pan out, then ILBs are more likely to underperform as the real yield moves back to more ‘normal’ levels prior to inflation picking up. This underperformance occurs because, although real yields are common to both ILBs and Nominals, the ongoing yield curve targeting by the RBA depresses the upward pressure on Nominal yields. By preventing the upward movement in Nominals, the result will be a compression of BEIs so that they become materially lower than inflation expectations. It is this upward movement in real yields and the compression of BEIs which will in turn prove the catalyst for the future outperformance of ILBs. Though there is still a material amount of uncertainty regarding the economic outlook, given the ongoing failure of central banks to stimulate inflation, this scenario would appear to be the more likely to unfold going forward.

Investors, when considering the relative attraction of ILBs, are unfortunately faced with the ‘chicken and egg’ dilemma of whether inflation or real yields will rise first. Complicating the assessment of likely scenarios are the uncertain times that we find ourselves in, which makes assessing the relative risks especially problematic. While recognising the complications, simply focusing on the inflation protection features of ILBs means investors risk overlooking the potentially adverse impacts associated with movements in real yields. Accordingly, while the outlook is still unclear, investors need to appreciate that though ILBs provide inflation protection, they can potentially be a ‘double-edged sword’.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets