Australian interest rates: the next move is probably down

Our view is non-consensus, and we’re okay with that. For the most part, the economic consensus in Australia is that the next interest rate move will be up. The current debate centres on when this move will occur, with the more dovish commentators suggesting we may have to wait until late 2020 to see the cash rate move to 1.75% from its current 1.50% setting.

Recent GDP growth (3.4% in the June quarter) and declines in unemployment (now down to 5%), along with an improved fiscal position, lend support to the thesis that the Australian economy is going “okay”. Indeed, Assistant Governor of the RBA, Guy Debelle, recently suggested it was only a matter of time until the labour market tightens and we see meaningful wage gains.

We have a different perspective. Most of the positive indicators (labour, GDP etc) tend to be lagging indicators – more informative about where we have been, rather than where we are going. When we think about interest rates, we focus on where we are going.

The case for lower interest rates

In February 2015 we put forward the case for Australian interest rates to approach 0%. At the time this was a non-consensus view, and the official cash rate was 2.50% (it was cut to 2.25% not long after). Of course, today the rate is stuck at 1.50%.

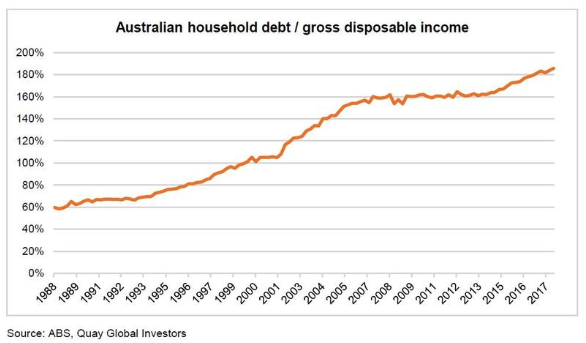

Much of our argument centred on the idea that the higher the private (household) levels of debt across developed economies, the lower the official cash interest rate. The thesis was simple: As households take on more debt, the potency of high interest rates increases – thereby biasing future movement more to the downside.

Australian household debt relative to income has only increased further since we published our paper. Now, any increase in interest rates would be highly restrictive based on current household balance sheets.

Now there’s more to the story

So Australian household debt levels, relative to income, are now at an all-time high. Can they go even higher from here?

Since the Royal Commission into the financial services industry, questions have been raised as to the quality of the lending practices of our major financial institutions. This has placed pressure on new lending, which is in turn placing significant pressure on residential property prices. The ability for households to borrow more is becoming problematic.

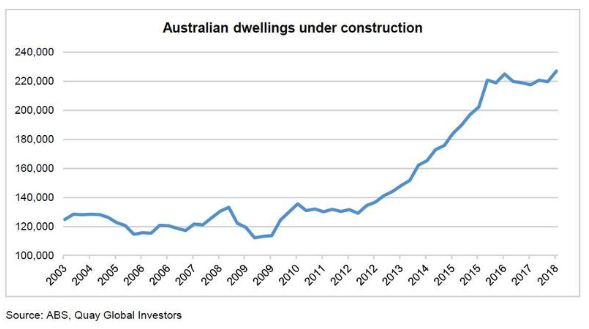

The banking industry’s sudden concern for conservative lending practices could not come at a worse time. Not only have east coast auction clearance rates fallen below 50% for certain weeks (where volumes are 800-1,000 dwellings), but the sheer volume of new supply under construction and yet to be settled (+220,000 dwellings) will place enormous additional demands on bank lending. In fact, required funding to settle current dwellings under construction has never been higher.

Assuming $0.8m per dwelling, total funding required for the current dwelling pipeline is near $180bn. To put this in context, total residential investment loans (which the RBA has tried to restrict) are only $550bn.

Given the time it takes for a project to go from pre-commitment to construction to completion to sale, it is likely the credit available to committed buyers has been reduced. This will surely put additional pressure on residential prices as ‘soon-to-be-owners’ look to sell prior to settlement and into the same market, where credit availability is just as tight.

The RBA does not move interest rates just for the property market – so why will a soft housing market convince the RBA to cut?

It won’t – at least not initially. They won’t be able to ignore it forever: households are a major part of the economy. Sentiment matters, as it will likely feed through to consumer confidence, then business confidence.

The risk is that housing weakness can lead to more tangible economic weakness. As prices fall and credit becomes tight, the construction industry will begin to contract. Jobs will be lost. If we look at the historic ratio of construction jobs to total jobs, it could be as many as 250,000 jobs (or 2.2% of the total workforce).

The experience in the US was worse post the financial crisis, as the industry shrunk to a size much smaller than the pre-cycle ratio. Markets tend to overshoot, and the construction job market in Australia is prone to meaningful downside risk.

The wider economic risk from contraction of the housing industry should not be underestimated. In 2011, the ABS estimated that the total ‘multiplier’ for output and employment in the construction industry is 2.866. So for every $1 million decrease in construction output, there is a decrease in output elsewhere in the economy of $2.9 million.

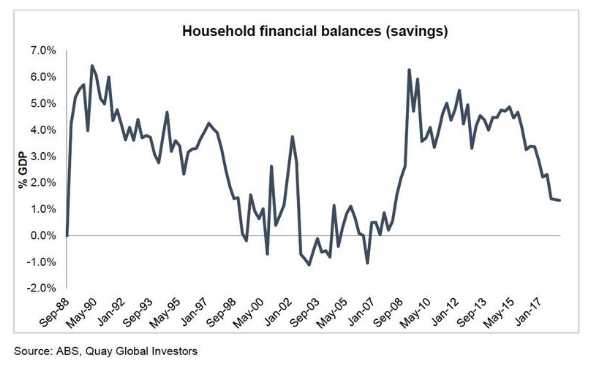

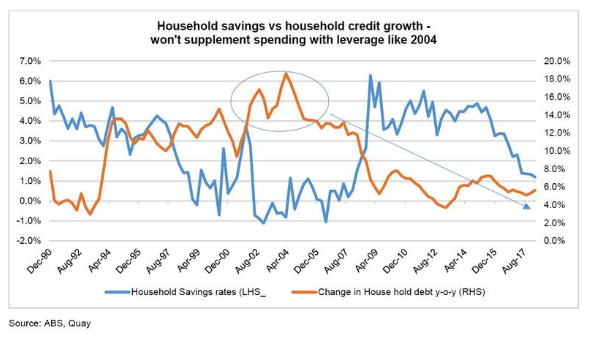

Australian savings rates are dangerously low

A factor that has supported Australia’s economic (and jobs) growth over the past four years has been the decline in household savings rates. While wage growth has been anaemic, household consumption has contributed positively to growth as households have chosen to save less (i.e. spend more) of their static income from one period to the next.

This trend is unsustainable for two reasons.

1. Households on balance need to net save due to a) the requirements of the superannuation guarantee system; and b) the fact that, on average, wealthy households tend to save more than they earn and the less wealthy cannot sustainably spend more than they earn.

2. In the past, certain households could supplement spending, despite low savings, by increasing leverage (borrowing) against real assets, as occurred in 2000-2005 (see chart below). In the current credit environment, this is almost certain not to happen again to the same degree.

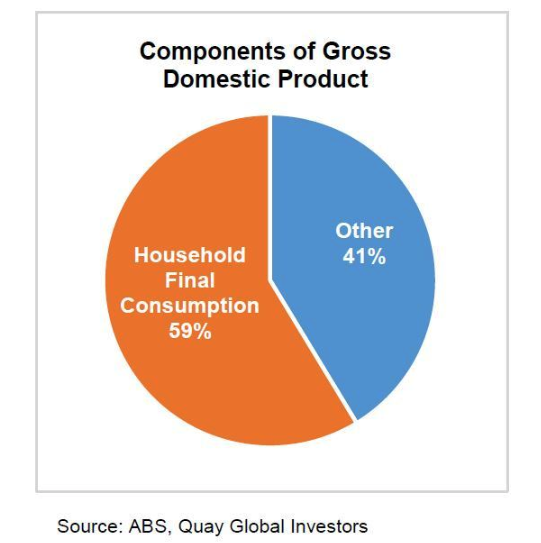

If the decline in household savings rates reverses (which seems inevitable) without a corresponding lift in credit, a major headwind will emerge for household consumption (60% of the economy). Since households are usually the customers for business, then business and investment conditions will soon follow.

In May 2017 we outlined our concerns for the Australian residential property market. As auction clearance rates fall and house prices correct, it seems this paper has aged well.

However, our attention now turns to the macroeconomic impact of this correction and the implications for policy. We see meaningful downside risk to the economy as the housing cycle unwinds, specifically due to:

• very high levels of household debt;

• tight credit conditions;

• potential downside to jobs and economic activity from the construction sector; and

• the almost inevitable rise in household savings, impacting 60% of GDP via household consumption.

We get the sense the RBA will be reluctant to cut given the current governors’ preference for financial stability over inflation. However, as far as financial stability is concerned, we fear that horse has already bolted. If the housing market continues to weaken, we believe the risk is that the RBA will face a sharply weaker economy in 2019 and will be forced to consider an official rate cut before the end of the decade.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Commodities

Central banks are doubling down on gold - should you?

Livewire Markets