Boral Limited (ASX: BLD)

Boral Limited is a multinational company dealing in building and construction materials. Founded in Australia, it also has extensive operations in the United States and Asia. Boral has a diverse area of operations within the building industry, including asphalt, road line marking, concrete, plasterboard, timber, windows, quarry, landfill, transport, roof tiles, bricks and pavers. Boral also produces cement via Boral Cement.

The company has three main divisions:

- USG Boral - is a leading manufacturer and supplier of gypsum-based wall and ceiling lining systems, mineral fibre acoustical ceiling systems, metal framing, joint compounds, high-performance panels and accessories throughout Asia, Australia and the Middle East.

- Boral Australia - is a major supplier of products and materials to the residential and commercial construction, and roads and engineering markets. As one of Australia’s largest and most experienced construction materials suppliers, Boral has the resources and the expertise to perform for customers Australia wide. This division has many subdivisions producing concrete, quarry operations, asphalt, cement, logistics solutions, property management services, bricks, stone, roof tiles and timber for flooring markets.

- Boral North America - The North America division combines the construction materials and building products businesses of Boral USA and Headwaters Inc., following Boral’s acquisition of Headwaters in May 2017. Boral North America has a national fly ash processing and distribution business and manufactures stone veneer, concrete and clay roof tiles, concrete block, light building products and windows for residential and commercial construction markets. Boral North America also has a construction materials business in Denver and has a 50% share of the Meridian Brick joint venture.

Financial Year 2017 Result

Boral recently reported NPAT of $342.7 million for financial year 2017, 9% above consensus due mainly to a lower than expected tax expense. A final dividend of 12 cents per share (50% franked) was declared, taking the full year dividend to 24c, up 7% on financial year 2016 and representing a payout ratio of 82%. EBIT grew 16% underpinned by a 7% lift in Boral Australia earnings and 2 months contribution from the Headwaters acquisition completed in May.

As mentioned, Boral Australia was the standout in the second half of 2017, outperforming previous guidance by 10% due to better price realisation

which is expected to continue in financial year 2018. The other main positive was incrementally optimistic commentary on Headwaters synergy realisation, where the company has guided they expect to achieve greater than US$100 million in synergy benefits. Net debt of $2.33 billion beat the company’s recent guidance of $2.6 billion.

USG Boral was the main disappointment as the Thailand, Indonesian and Chinese operations reported EBIT declines and guidance was lowered for financial year 2018 for these businesses. The company also guided to increased capital expenditure of $425-475 million driven by increased funds required at Headwaters. This increased expenditure requirement at Headwaters is expected to be a one-off expense.

Outlook

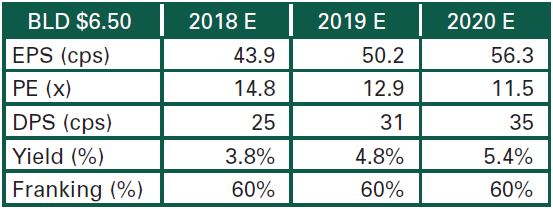

The recently completed acquisition of Headwaters in the US is a game changer for Boral, virtually doubling their market capitalisation. By all accounts the integration of this new business is progressing extremely well and the aforementioned synergies to be had are significant. The expected continuing growth in the US economy (in particular housing and infrastructure) and the Australian infrastructure segment (Boral’s exposure being 20%), leaves the company in a very strong position to continue its impressive trajectory over the coming years. Currently the stock is trading at an 11% premium to the ASX 200 Industrials which is significantly below its 5 year average premium of 19%. When one considers the quality of Boral’s businesses and the anticipated growth coming through in housing and infrastructure, we believe the company is attractively priced at the current 14.8 times financial year 2018 P/E ratio.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment