Boring Reliable Inc vs Moonshot Inc: Who wins and why

One of the side effects of low interest rates is that, because of the way that companies are valued, investors place a higher value on companies (and investment projects) which have a low probability, high payoff, a long time in the future.

This helps explain why investors have been prepared to pay up for loss-making companies.

We can show why this makes perfect sense mathematically, using a (relatively) simple example. There is a bit of maths involved but I’ve tried to keep it as simple as possible to make it easier to follow.

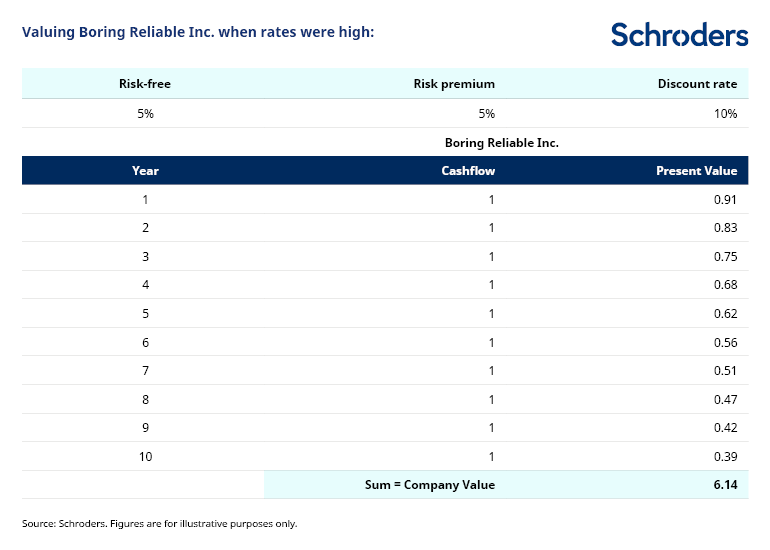

Boring Reliable Inc.

Consider a fictitious company, Boring Reliable Inc. It pays out $1 of cash-per-share to equity holders each year for the next 10 years. For simplicity, I’ve assumed this stays constant over time and that it has no other residual value. However, the broad principles and conclusions would remain the same if we used more realistic assumptions.

The value of this company today can be calculated as the present value of these cash flows. i.e. how much is $1 in 10 years time worth today? This is the maths part…

We use a “discount rate” to work this out, which is the sum of two factors. Firstly the “risk-free rate” of the time – this is normally equal to the interest paid on an investment considered extremely safe, such as a 3-month US government bond. This is added to a “risk premium”, which is the difference between the expected rate of return from an asset and the risk free rate.

For the purposes of this example, we have assumed a risk premium of 5%, but our broad conclusions would be the same if we used a different figure. The table below shows how this works out, if we used a risk-free rate of around 5%. This is similar to where they were before the financial crisis hit, hard as it might be to imagine today, when the risk free rate is around 0.70%!

The present value of these cash flows is the value of the company today: $6.14.

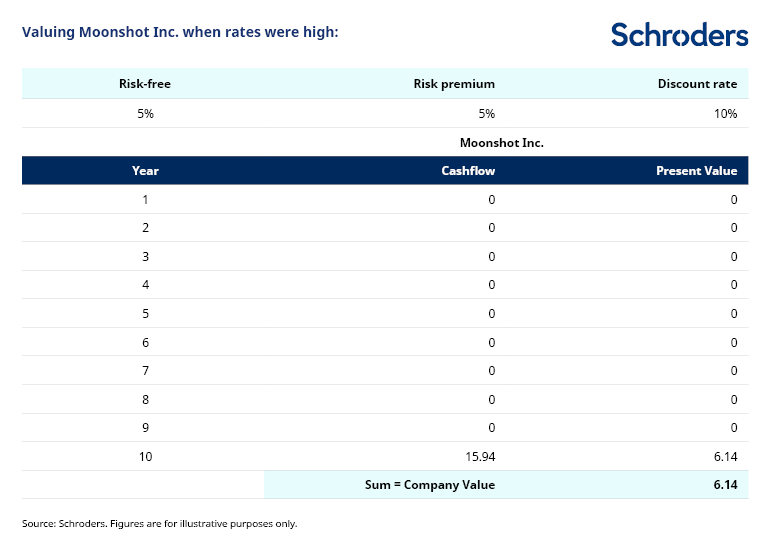

Moonshot Inc.

Now consider a racier (also fictional) company, Moonshot Inc. It is expected to generate no cash whatsoever for the next nine years but then hit gold in year ten, with a bumper payout for investors. We can work out how big this payout needs to be for the two companies to have the same present value. This turns out to be $15.94:

So if you can transport yourself back to 2007, Boring Reliable Inc. and Moonshot Inc. would have been worth the same. What about today?

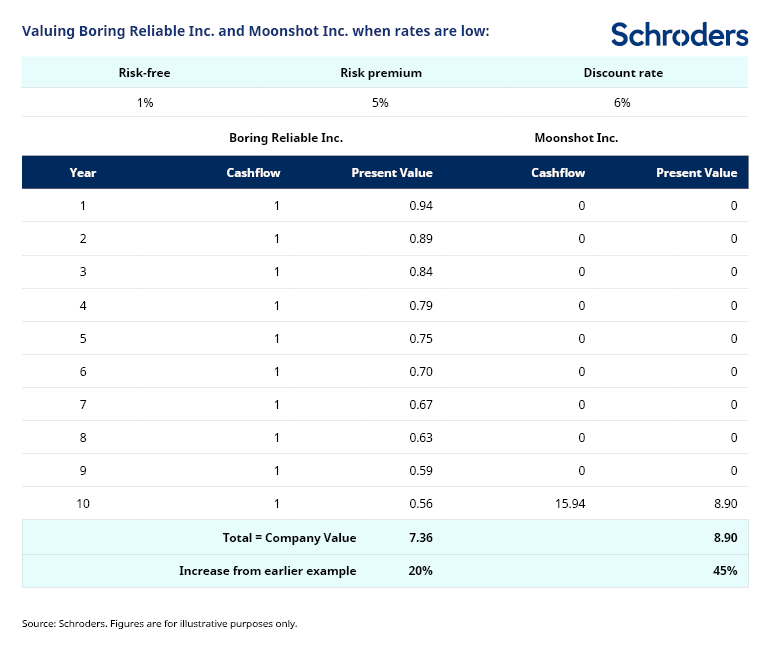

The impact of lower interest rates

To keep the numbers simple, let’s use a risk-free rate of 1% to reflect today’s environment. If you used 0% or a negative number it would simply result in a more extreme version of our results. The most important point is that it is much lower than the 5% used previously.

The table below shows how the value of each company changes under these new conditions. We have kept all other assumptions the same, for simplicity.

Both companies are now worth more, as the lower risk free rate results in a higher present value for future cash flows – even though those cash flows are identical to previously. In other words, for a given level of earnings or cash flow, lower interest rates translate into a higher valuation.

This is one reason why most measures of stock market valuations appear pretty expensive when compared with historical experience. Rather than being surprising, this is what you should expect to see!

Secondly, Moonshot Inc.’s value has shot up by much more than Boring Reliable Inc. : a 45% gain compared with only 20%. This is because the present value of more distant cash flows is much more sensitive to interest rates than those in the near term. Because all of Moonshot Inc.’s value is derived from a single cash flow, far off into the future, its overall value is much more sensitive to the fall in rates.

This is nothing to do with whether Moonshot’s prospects have improved relative to Boring Reliable. Their prospects are the same as before. But their values are dramatically different. A version of this is what has been playing out in markets over the past decade. Growth companies, by definition, are expected to grow faster than other companies. In other words, their earnings in 10 years time are expected to be a lot higher than they are at present. This means the present value of those earnings is highly sensitive to changes in interest rates – like Moonshot’s.

In contrast, value stocks have lower growth expectations, so are more like Boring Reliable – they receive less of a benefit from falling rates.

When considered in this way, the outperformance of growth over value in the past decade can be partly explained by maths – it is a direct consequence of lower interest rates (among other things not covered in this article, such as changes in relative growth prospects).

Of course, the reverse is also true. In the example above, Moonshot would fall roughly twice as much as Boring Reliable for a given rise in interest rates. Even a small rise in rates could swing the tables back in value’s favour.

One other important consideration is that a lot can happen in 10 years. Although Moonshot may be forecast to earn $15.94 at that time, there can be no certainties. In contrast, Boring Reliable is forecast to start generating cash immediately. There is less hope baked into its valuation. Followers of growth and value stocks would be wise to bear this in mind.

Stay up to date with all my latest insights by clicking the follow button below

Disclaimer

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

This information is not an offer, solicitation or recommendation or to adopt any investment strategy. The forecasts included are not guaranteed

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Duncan Lamont is responsible for high quality thought leadership research, aimed at offering insights which help our clients make better investing decisions. Since joining Schroders, Duncan has written and co-authored a wide range of papers, worked with industry bodies and been quoted in the press on a variety of topics. He joined Schroders in 2016 and is based in London.

Duncan was a Principal in the Global Asset Allocation team at Aon Hewitt from 2009 to 2016, which involved the development of the firm’s long term strategic capital market assumptions and driving its medium term asset allocation views across the full range of traditional and alternative asset classes. He was an assistant director at MacArthur & Co from 2006 to 2009, a corporate finance boutique, where he advised on small cap public and private market capital raisings, and M&A activity. He was a trainee investment consultant at Hewitt Associates (now Aon Hewitt) from 2004 to 2006, which involved advising defined benefit and defined contribution pension funds on all aspects of investment strategy.

Duncan Lamont is responsible for high quality thought leadership research, aimed at offering insights which help our clients make better investing decisions. Since joining Schroders, Duncan has written and co-authored a wide range of papers,...

Expertise

Duncan Lamont is responsible for high quality thought leadership research, aimed at offering insights which help our clients make better investing decisions. Since joining Schroders, Duncan has written and co-authored a wide range of papers,...

Expertise

Comments

Comments

Sign In or Join Free to comment