Buckle Up Investors, More Cliff-Drops are Coming

The cliff-drop in US equities at the opening of trading on August 17 shocked many investors. Since then, the ongoing questioning of the true liquidity within major markets and the amount of leverage that is now built into investor viewpoints has continued. In October a seminal paper on volatility and shadow convexity was released by Artemis Capital, which I highly recommend if you have the time and headspace for a 40 page philosophical/investment thesis. Combining some of themes of this paper with my own thoughts, I want to focus on three areas which have the potential to amplify sell-offs and create further cliff-drop moments.

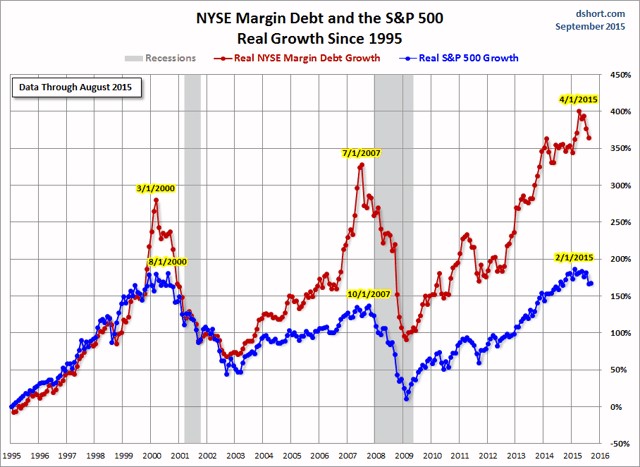

Firstly, the proportion of investment products with built-in leverage appears to be at very high levels. Some exchange traded funds have double or triple exposures built-in, which in theory allows investors to express both a highly liquid and leveraged view. Other avenues for leveraged investing include contracts for difference, options and futures trading, repurchase agreements and margin loans. The reduction of margin lending in China in the third quarter, which reversed during October, appears to explain much of the movements in Chinese equites. Also of note is the reduction in margin lending in the US, which as the graph below shows is following a similar trend to 2000 and 2007.

Secondly, there’s been a massive reduction in the amount of human controlled trading of vanilla investment products in the last decade. Index funds and ETFs often rely on automated trading for rebalancing. High frequency traders have largely replaced market makers, which works well during the good times but can fail abysmally during high volatility periods. In the event that markets become volatile, automated systems are often turned off, and the ones that are left running can end up chasing down prices until a human steps in and takes the other side.

Thirdly, the widespread acceptance of risk parity investing brings further leverage to markets. Risk parity argues that each asset class should be of equal risk in the portfolio, with leverage added to low risk classes to increase their risk. In a basic application, this means that the bond allocation would be leveraged, whilst the equity allocation would remain unleveraged. In theory, this should create a much more stable portfolio as when equities fall, bonds usually rise and vice versa. The leveraging of the bond component (in theory) means the size of the ups and downs are equalised. The knockout event is if equities and bonds both fall, something that is rare in recent decades but not without precedent. With interest rates at or near all-time low levels and equities at elevated levels by some measures (e.g. CAPE, Market Cap/GDP) the potential is there for a bad outcome for risk parity.

The largest and most successful proponent of risk parity has been Bridgewater, the world’s largest hedge fund. Its success has inspired many others to follow this style, in the same way that LTCM attracted copycats with its profitable early years. A comparison with LTCM is somewhat unfair in that the amount of leverage involved is far less. However, the potential for a whole bunch of investors to crowd into the same trades and end up on the wrong side of market moves is a history lesson we should keep in mind.

Pulling the three concepts together, we have more leverage and more automated trading. Together, this increases the possibility of cliff-drop price movements as occurred on August 17. The historical comparison that seems most applicable is 1987, with program trading taking the blame for the severity of the sell-off on October 28/29 that year. A spike in interest rates, accompanied by a sell-off in equities, could see crowded and leveraged positions exposed and forced to unwind quickly. Buckle up investors, more cliff-drops may lie ahead.

Written by Jonathan Rochford for Narrow Road Capital on November 16, 2015. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

1 topic

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The shift toward scarcity: a playbook for a new era of investing

Talaria Asset Management