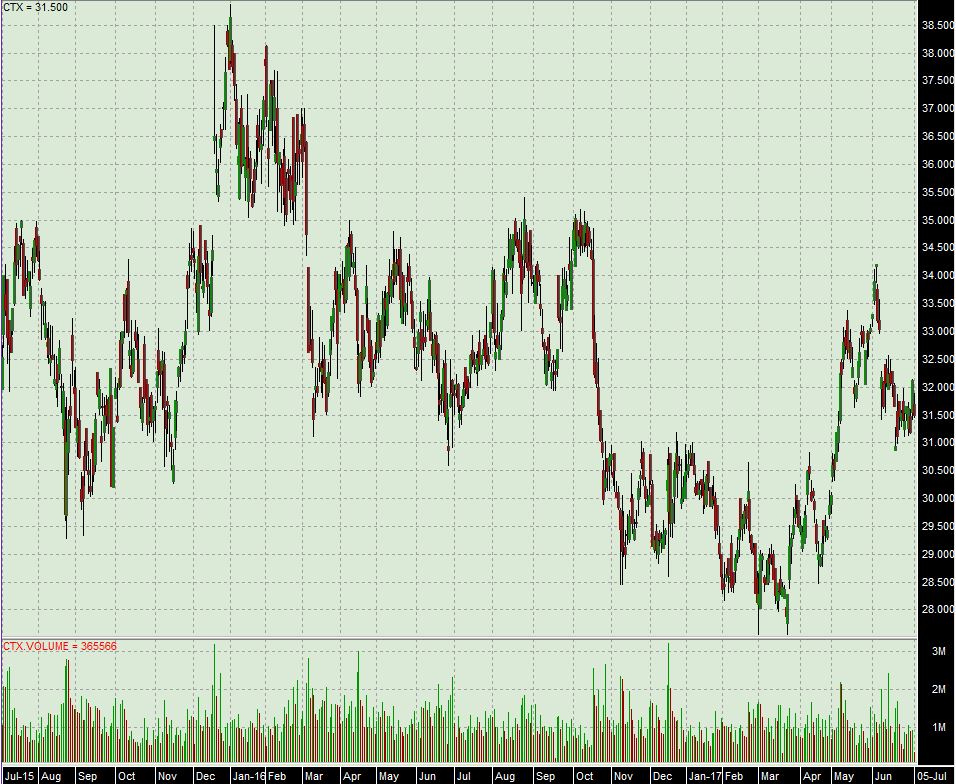

Caltex Australia Limited (ASX:CTX)

Caltex is the leading provider of transport fuels in Australia, providing about 20% of the total fuel market. In addition to being a vertically integrated supplier of fuel, Caltex operates Australia's largest convenience retail network of fuel and convenience sites trading under the Star Mart brand; with more than 620 stores and over 320 franchisees. Roughly 70% of Caltex’s income comes from royalties paid to Caltex by franchisees based on turnover, convenience store income from company operated stores, franchise fees, royalties, property, plant and equipment rentals and income from the company's fuel card (Starcard).

In July 2012 Caltex announced a restructure of their supply chain, including the conversion of the Kurnell refinery to a major import terminal. Margins within the refining business had been under pressure for some time, and the closure was a significant positive for the company. Macro headwinds were affecting crude production and pricing. Caltex has done well to reduce their exposure to the vagaries of this market. On schedule, in October 2014, the Kurnell refinery was safely shut down and terminal operations commenced on site. The new, modern terminal at Kurnell is Australia’s largest fuel import terminal. The clear strategy is to focus on optimising the entire supply chain from product sourcing to the customer. Caltex has upgraded their supply chain information systems and established a Singaporean operation for product sourcing and retained their Lytton refinery in Brisbane.

Caltex Refiner Margin Update

In June, Caltex reported a realised Caltex Refiner Margin (CRM) of US$9.94/bbl for May 2017, down from US$15.32/bbl in April. Despite the fall, the margin is above that reported in May last year (US$9.88/bbl). The key reason for the margin squeeze was the planned shutdown of the Benzene Hydrogenation Unit (BHU) which interrupted premium gasoline production, resulting in a higher portion of regular gasoline production. The temporary shutdown of the BHU project should be viewed as a one-off and was necessary for the completion of maintenance and upgrades that will improve refinery yield.

2017 Half Year Profit Guidance

Caltex announced a half year replacement cost operating profit (which strips out the impact of crude oil price fluctuations on inventory) outlook of $290 million to $310 million, excluding significant items, up from $254 million in last year’s first half. The Supply and Marketing businesses EBIT outlook (including net externalities of around $5 million) of between $360 million and $375 million has increased by 4% on the pcp whilst the Lytton refinery EBIT has come in at approximately $150 million, up from $92 million on the pcp, reflecting overall higher first half refining margins.

Caltex maintains a strong balance sheet, with net debt forecast to be approximately $700 million, including the $95 million used for the Milemaker acquisition (detailed below) in May, but excluding the recent Gull NZ Acquisition (detailed below) that was approved on the 26th of June valued at $325 million. Statutory net profit, including one-offs, is forecast to be $250m to $270m, down from $318m last year after a $40m loss on crude oil and refined product inventories and the $20m cost of setting up an assistance fund for franchise workers.

Woolworths Petrol

In December Woolworths announced that it would not be accepting Caltex’s bid to purchase all of its 527 fuel convenience stores and 16 development sites. Instead, Woolworths and BP will develop a joint fuel convenience store called Metro at BP after the retailer agreed to sell its petrol stations to BP for $1.70 billion. The deal ended the intentions of Caltex to buy the service stations and expand it marketing outlets and will reduce its fuel distribution capabilities via its distribution deal with Woolworths. This acquisition was made at a high EBITDA transaction multiple of 10.5x, too expensive for Caltex and was the key catalyst for losing the bid to BP.

This transaction was a smart avoid by Caltex and we are impressed by the strict acquisition policy employed. In addition, large scale consolidation in the petrol industry has historically been viewed negatively by the ACCC and there is a view that the deal may not be approved (ACCC opposed Caltex’s acquisition of Mobil in 2009). Their preference is for a new player to enter the market and will be worried about the 39% market share BP will have if the deal is approved in January next year. Given BP’s large existing network of petrol stations, the deal will be likely be evaluated site-by-site due to the lessened competition in the areas with both BP and Woolworth’s sites, likely leading to an opportunity for CTX to pick up additional sites.

To replace lost fuel volumes and increase its convenience store foot-print, Caltex has recently made two acquisitions; Milemaker and Gull NZ.

Milemaker; On the 7th November 2016, Caltex announced that it had entered into an agreement to purchase Milemaker Petroleum’s retail fuel business assets in Victoria for $95 million on an EBITDA multiple of 8x. The transaction will see Caltex acquire the business assets and take over operation of 46 service stations in Victoria, with the majority located in and around Melbourne. The deal was approved by the ACCC in May. Caltex will also enter into long term leases for each of the sites with options out to 30 years.

Gull NZ; Caltex Australia Limited (ASX:CTX) welcomes the consent of the New Zealand Overseas Investment Office to its proposed acquisition of Gull New Zealand including 78 stores, and the six currently under construction, for a purchase price of NZ$340 million (approximately A$325 million). Caltex anticipates completing the acquisition in July. The deal will be funded through a combination of existing and new bank debt arrangements and is expected to be earnings per share accretive by the end of its first full year of operation under Caltex ownership. The Gull acquisition represents a multiple of 8x the business’s forecast 2017 EBITDA.

Summary

We view Caltex’s acquisition strategy as a positive and agree that they should not be overpaying for businesses. The Woolworth’s acquisition was a hard one to let go but management maintained they are not willing to expand at any price. If approved, the end of the distribution deal with Woolworths will cost Caltex $80 million p.a., a hole which Caltex is filling quickly with the earnings from new acquisitions; expected to be $50 million p.a. This move represents a shift in business operations as Caltex continues to place emphasis on its retail convenience business rather than fuel distribution agreements, which we view as a better business model (reduced exposure to the oil price and refining margins). Caltex has a strong track record of generating high returns on capital and has outlined strategies to generate higher sales from an underutilised retail sites. The infrastructure assets owned, including the Kurnell importing and Lytton refining facilities combined provide ~20% of Australia's fuel, these assets are hard to replicate and thus provide high barriers to entry.

Financials

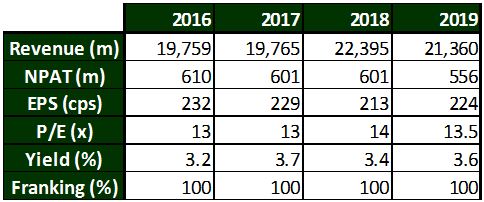

With CTX trading on FY17 price to earnings ratio of 13x, which is low for a defensive business such as Caltex, paying a dividend yield of 3.7% (on a 50% payout ratio) and with relatively low debt, we find its value compelling.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment