Caltex: Shrink to grow

Sam Dyson

Vertium Asset Management

Investors love companies that can deploy capital at high returns over a long period of time. However, great shareholder returns can also be achieved from companies that shrink their capital base. Take Caltex for example.

Caltex operates in an industry perceived to be dying. Vehicles are ever more fuel-efficient, and cheap battery power is just around the corner. Surely this is a stock to avoid? Yet its history is one of successful restructuring: shifting focus and capital to where it can best create value. And now, Caltex is looking at doing exactly this with its fuel retailing assets.

The Refining Retreat

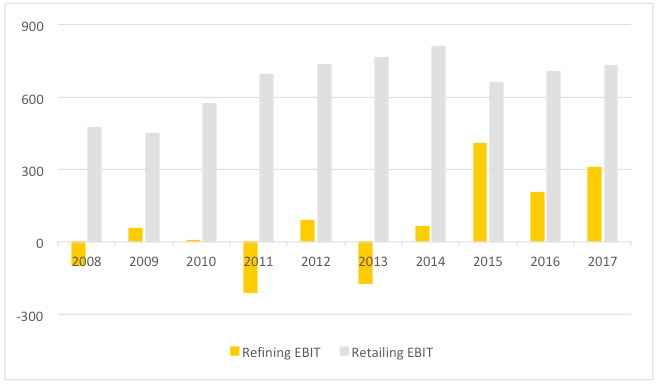

Profits for most of Caltex’s corporate life have come from refining crude oil into fuels. Earnings were volatile and highly sensitive to the mega-refineries being built in Asia. Caltex suffered during the Asia crisis when fuel imports were much cheaper, and then benefited in the 2000s from stricter Australian petrol standards and higher Asian refining margins.

In 2009, Julian Segal as Caltex’s new CEO recognised that the jewel in the crown was the company’s fuel retail network. The refining division delivered feast or famine, while the under-appreciated retailing division had grown steadily.

Chart 1 – segment earnings

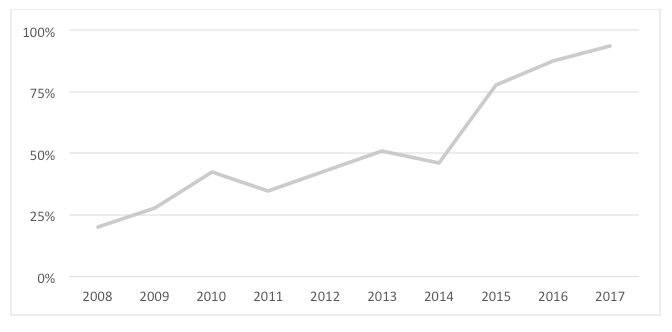

Caltex, under his stewardship, was to focus on fuel retailing. A renewed focus on brand, premium fuels and convenience was coupled with, firstly, a failed attempt to buy Mobil’s petrol stations, followed by the acquisition of some of the Caltex franchise re-sellers. Capital expenditure was increasingly devoted to fuel retailing, as seen in chart 2.

Chart 2 – share of capital expenditure on retailing

In 2014 Caltex closed its volatile, capital-intensive refinery at Kurnell, converting it into an import terminal. Profitability improved because Caltex’s one remaining refinery was fully utilised, and its regional trading activities received a volume boost. With less maintenance, lower working capital and a tax holiday, there was even enough spare cash to buy back $270m of shares in 2016.

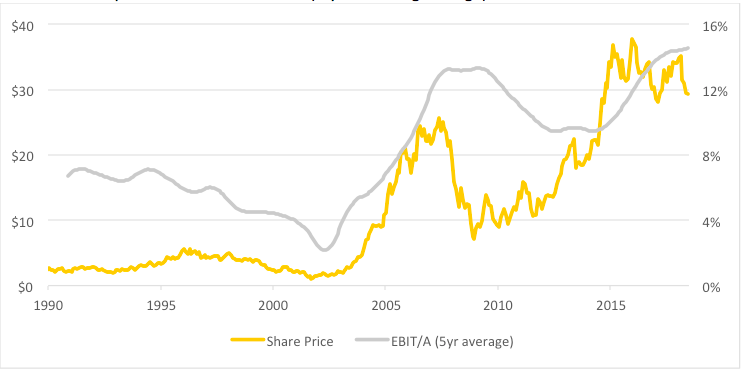

This is ‘shrink to grow’: assets shrunk and profits grew. The share price has followed the company’s return on assets (EBIT/A) higher.

Chart 3 – share price and return on assets (5-year moving average)

What’s Next?

Return on assets is now very respectable at around 14%. Is that it, or can CTX do more ‘shrink to grow’? We think more: management are contemplating an asset ownership restructure, vending the retail properties into a property trust. These property assets would be highly prized by REIT investors who want yield and a dependable 3% annual rental growth.

Spinning off assets is nothing new. Wesfarmers, for example, views it as a core strategy to maximise the company’s return on funds, constantly vending Bunnings property assets into its listed trust (BWP) or to other asset owners. And CTX has two precedents in its own sector. Viva Energy (the Shell fuel business) spun off Viva Energy REIT (VVR) in 2016, and in 2017 the APN Property Group floated about 70 petrol sites via the Convenience Retail REIT (CRR).

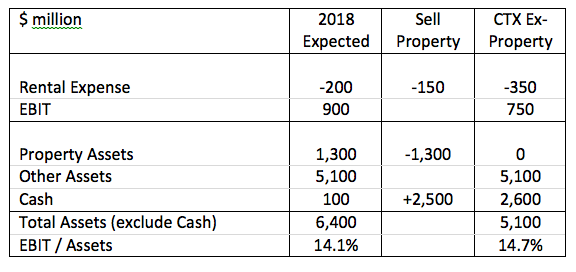

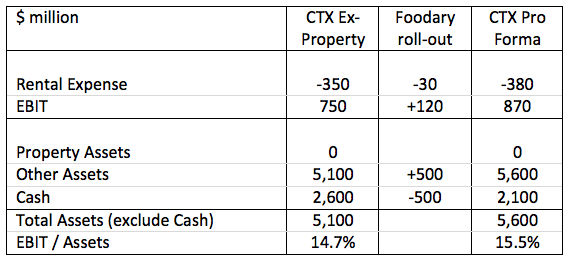

How does selling assets create shareholder value for CTX? Petrol retail assets are valued at around a 6% cap-rate, which is equivalent to roughly 17.5x EBITDA. That compares to the whole of Caltex which is currently valued around 7x EBITDA. That is a significant value uplift: property valued on the books at $1,300m, generating $150m of rent, can be sold at a market value of $2,500m.

Redeploying Capital

So far, this is just half of the story. How could Caltex redeploy the $2.5 billion proceeds?

Caltex wants to buy back its franchisees and roll out its ‘Foodary’ convenience format, transforming petrol retailing into a ‘click and collect’ offering for fuel, food, laundry and mail. Retailing is all about maximising sales per square metre, so this makes a lot of sense.

There is execution risk. Management may want to do this before selling the properties, however property investors would love to fund such a roll-out. For a slight rent increase, Caltex could save itself roughly $0.5 billion of capex. Another $400m or so would be needed to upgrade systems and the metropolitan sites outside the REIT, plus $100-120m to buy back the franchises. In return, on its own (somewhat conservative) estimates, Caltex expects a $120-150m boost to pre-tax earnings.

Franking Credits At Long Last?

In this scenario there is roughly $2 billion of cash. But isn’t this just ‘financial engineering’? After all, Caltex is just swapping its property assets for a large rent liability. New accounting standards will bring this back on to the balance sheet anyway… Well yes, but renting is what retailers do.

Caltex could pay off all debt and still have $1.3 billion of cash left over. Its ‘fixed-charge coverage ratio’, a measure of balance sheet strength commonly used for retailers, would be fairly reasonable at 3.3x.

What else? There is a huge $936m surplus of franking credits, enough to fully-frank $3.1 billion of dividends. This really should be in shareholders’ pockets. Returning any surplus cash via a fully-franked special dividend would be a good start. The potential in this scenario is $5.00/share plus $2.14/share of franking credits.

We have a basic idea of the upside potential: modest growth, improved return on capital, and $7/share return of capital. We aren’t paying for that upside, with the stock priced at only 13 times earnings and paying a 4% fully-franked dividend yield. Shrinking can be enriching.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and analysing Australian companies.

Before joining Vertium, Sam was an Investment Analyst at Cadence Capital and an Equities Analyst / Portfolio Manager at Maple-Brown Abbott where he co-managed the Maple-Brown Abbott Australian large and small-cap portfolios.

1 stock mentioned

Sam Dyson

Vertium Asset Management

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and...

Expertise

Sam Dyson

Vertium Asset Management

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and...

Expertise

Comments

Comments

Sign In or Join Free to comment