Can Australia handle a downturn in home building?

This is the question perplexing many market commentators. There is an adjustment occurring in the residential property market. Property prices nationwide peaked in late 2017 and have since fallen by 9%, bringing them back to mid-2016 levels. According to CoreLogic, property prices peaked in Sydney in July 2017 and have now been declining for 20 months with the market down 13.2%. The recent decline in property values has been steeper than most previous declines. Many have focused on the impact from the Royal Commission.

Reserve Bank of Australia (RBA) Governor Philip Lowe stated in an address to the AFR Business Summit on 6 March 2019 that “the maximum loan size offered to new borrowers has fallen by around 20 per cent since 2015. This reflects a combination of factors, including more accurate reporting of expenses, larger discounts applied to certain types of income and more comprehensive reporting of other liabilities. Even so, only around 10 per cent of people borrow the maximum they are offered.”

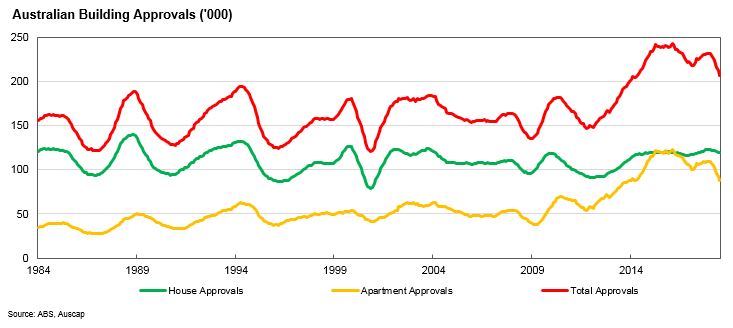

With property prices, housing turnover and housing credit growth falling, building approvals have also slowed.

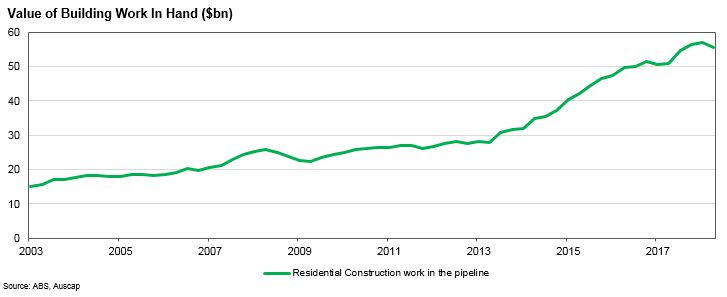

The fall in building approvals is leading to concern that a decline in residential construction will result in a significant contraction in investment activity. It has been suggested that the decline may not be imminent, due to the volume of work in hand in the residential construction sector.

However, fast forward 12 months and the decline in approvals is likely to result in a decline in residential construction activity. The question is, how significant will the decline be to the broader economy?

However, fast forward 12 months and the decline in approvals is likely to result in a decline in residential construction activity. The question is, how significant will the decline be to the broader economy?

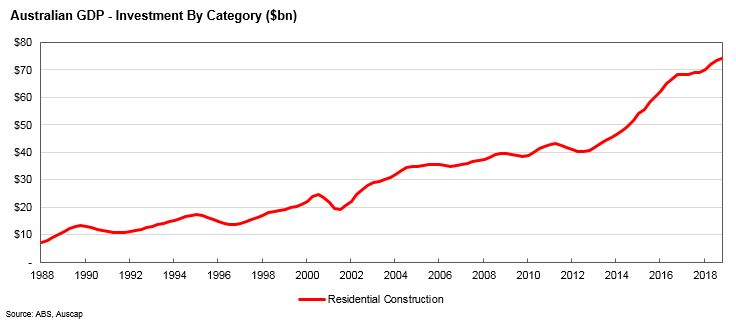

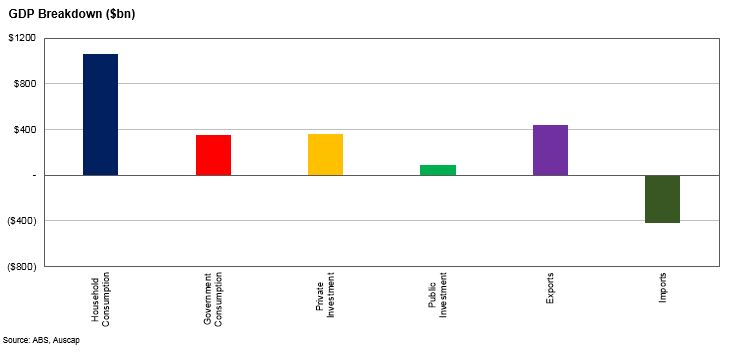

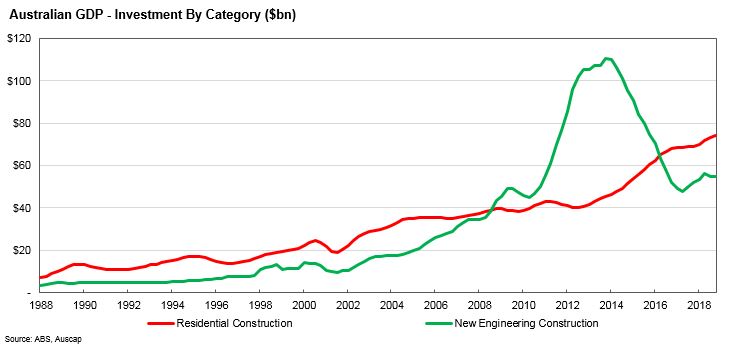

Residential construction contributed $74bn to the Australian economy in 2018. Were the fall in construction activity to be 20-30%, $15bn to $20bn would be detracted from Australia’s GDP. The effect could be greater if this slowdown in activity spills over into related sectors of the economy, something that is difficult to predict. How significant is the potential decline in residential construction activity to the Australian economy? Private and public investment contribute circa $450bn in aggregate to Australia’s total GDP of $1.9 trillion each year. So $20bn is approximately 1% of Australia’s GDP.

The RBA recently focused on the impact of falling house prices on household consumption. While this is not the focus of this newsletter, we note their estimate that a 10% increase in net housing wealth would raise consumption by around 0.75% in the short run and 1.5% in the longer run (Source: Governor Philip Lowe, Reserve Bank of Australia, “The Housing Market and the Economy”, Address to the AFR Business Summit, 6 March 2019)

It is worth noting that the Australian economy has, in the recent past, dealt with a far larger contraction in investment activity. At the height of the mining, oil and gas boom, engineering activity contributed approximately $110bn to Australia’s GDP. Following the completion of this work, this contribution dropped to under $50bn per annum within a few years. This contraction resulted in aggregate investment drifting backwards for a number of years earlier this decade. This suggests that as long as there are compensating factors, Australia’s economy is able to handle a sector contraction.

It is worth noting that the Australian economy has, in the recent past, dealt with a far larger contraction in investment activity. At the height of the mining, oil and gas boom, engineering activity contributed approximately $110bn to Australia’s GDP. Following the completion of this work, this contribution dropped to under $50bn per annum within a few years. This contraction resulted in aggregate investment drifting backwards for a number of years earlier this decade. This suggests that as long as there are compensating factors, Australia’s economy is able to handle a sector contraction.

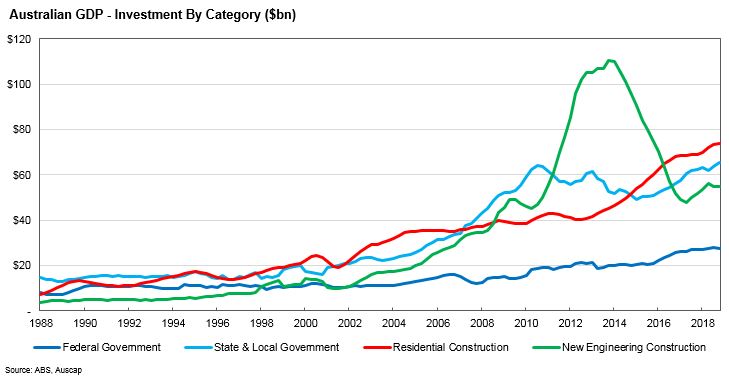

So are there compensating factors that might assist the economy with the forecast decline in residential construction activity? The answer appears to be yes. State and local governments are promising significant increases in infrastructure investment over the next three years. The Labor Government in Victoria secured victory late in 2018 with discussion of $95bn worth of investment spend on infrastructure, with over $30bn to be spent over the next few years. The incumbent Liberal Government has promised the commencement of $70bn of expenditure on transport infrastructure should it win another term in office at the upcoming New South Wales state election, while Labor has promised $50bn worth if it is successful. And with a Federal election looming, promises in relation to Government investment may continue to grow.

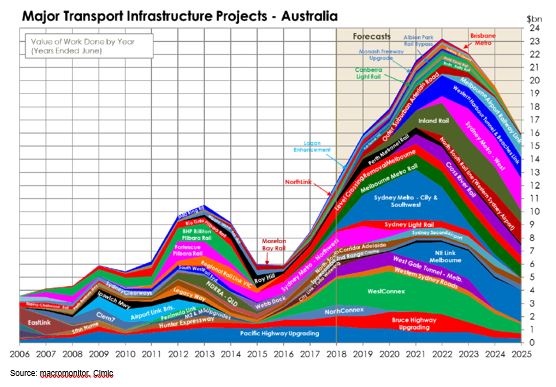

Incremental infrastructure promises will add to the boom that we are already experiencing. The forecast major transport infrastructure projects as at December 2018 are highlighted in the chart below.

Incremental infrastructure promises will add to the boom that we are already experiencing. The forecast major transport infrastructure projects as at December 2018 are highlighted in the chart below.

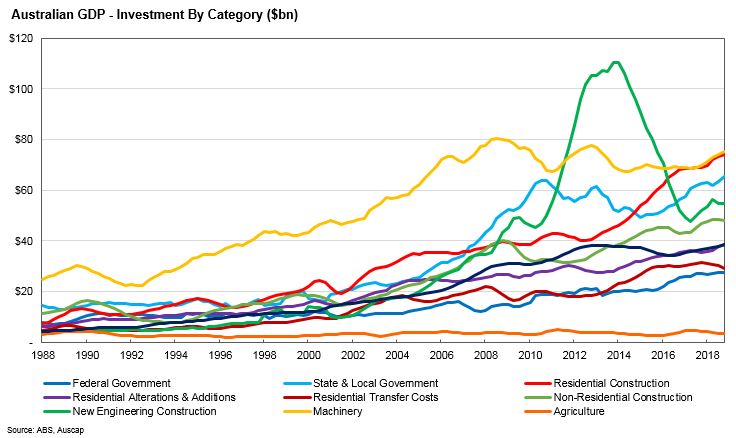

Additionally, there are other sources of likely growth. Engineering investment may have bottomed. In 2018 there were significant approvals for iron ore projects in the Pilbara. BHP approved the AU$4.8bn South Flank project to replace its Yandi mine, Rio Tinto approved an AU$3.5bn investment in the Koodaideri iron ore mine, while Fortescue approved spending AU$1.8bn on the new Eliwana mine and rail project in the West Pilbara. Many other categories of investment are also on an upward trajectory.

Additionally, there are other sources of likely growth. Engineering investment may have bottomed. In 2018 there were significant approvals for iron ore projects in the Pilbara. BHP approved the AU$4.8bn South Flank project to replace its Yandi mine, Rio Tinto approved an AU$3.5bn investment in the Koodaideri iron ore mine, while Fortescue approved spending AU$1.8bn on the new Eliwana mine and rail project in the West Pilbara. Many other categories of investment are also on an upward trajectory.

And in time residential construction, should it fall as expected, will recover. The RBA does not believe that there has been a significant overbuild of residential housing. Australia’s population is growing quickly, with the Australian Bureau of Statistics forecasting the formation of over 170,000 new households a year. This provides a constant source of demand for new housing. Australia’s population growth is solid and supports the likelihood of strong economic growth. We recognise that the housing slowdown might present some risks to the domestic economy, however these risks presently appear manageable. While we continue to closely monitor the data, it currently provides support for a thesis that Australia may, absent external shocks and barring unforeseen circumstances, be able to navigate the current slowdown in residential construction. It seems appropriate for Governor Lowe to have the final word.

“The adjustment in our housing market is manageable for the overall economy. It is unlikely to derail our economic expansion. It will also have some positive side-effects by making housing more affordable for many people.”

RBA Governor Philip Lowe, 6 March 2019

Tim Carleton is Principal and Portfolio Manager at Auscap Asset Management, a boutique Australian equities-focussed long/short investment manager. This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. A person should obtain and consider the Product Disclosure Statement before deciding whether to invest in any Auscap fund.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment