Cash is King

Andrew Smith

Perennial Value Management

During reporting season we were faced with many presentations that had flattering adjusted EBITDA and normalized NPAT figures – but these two numbers do not reveal the whole story to investors. To assess a company’s true health we make a beeline for their cashflow statement – a much more difficult statement to manipulate than the profit and loss.

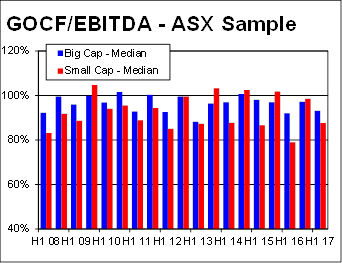

We scrutinise how much of the reported EBITDA translates to cashflow with a result of 100% suggesting the reported EBITDA is an accurate guide, while numbers which fall well below 100% suggesting the company may have leaned heavily on provisions and other accounting tricks to hit their numbers.

Looking at Small Caps during February, it was pleasing to see a general improvement in gross cashflow to EBITDA with an average above 85%, compared to this time last year where the average fell to below 80%.

Source: Independent Research sourced by Perennial Value

When assessing the companies in our portfolio it was even healthier at 97.5%.

One stock which disappointed us on the cash conversion was Mantra. We had started building a position post recent share price weakness, however poor cashflow conversion of 69% (compared to an historic average above 100%) suggested low quality earnings so we exited soon after the result. It is interesting to note that the Managing Director, Bob East, has also found a better use for his money, selling 250,000 shares in early March.

Did earnings grow to expectations?

When assessing the level of growth in small cap earnings it is useful to analyse what expectations were leading into February.

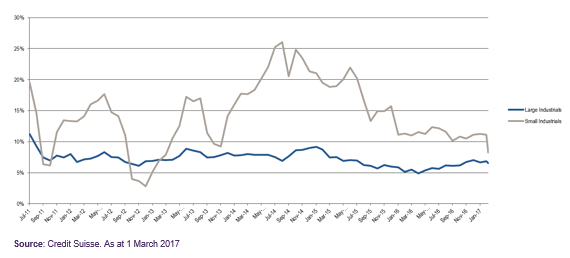

The following chart, courtesy of Credit Suisse, shows that expectations for earnings growth in Small Cap industrials had come back significantly courtesy of the brutal confession season, which began in November 2016.

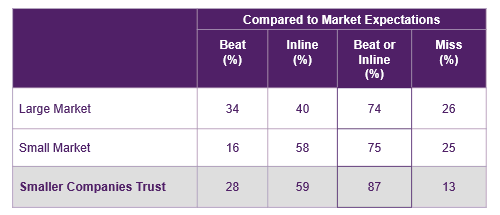

Given how low expectations were it is not surprising that the majority of companies were able to either to come inline with expectations or beat these low expectations. Pleasingly our portfolio performed better than then average relative to expectations.

Source: Date compiled by Perennial Value, Deutsche Bank and Credit Suisse

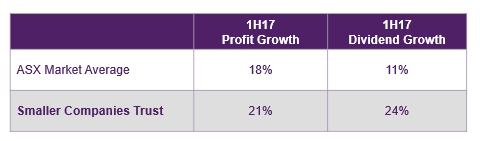

It is testament to the diverse nature of the Small Cap universe that while growth was much scarcer than in past years we were still able to construct a portfolio which delivered 21% earnings growth and 24% dividend growth – this was ahead of the broader market average which was boosted by the recovery in resource earnings.

Source: Date compiled by Perennial Value and Deutsche Bank

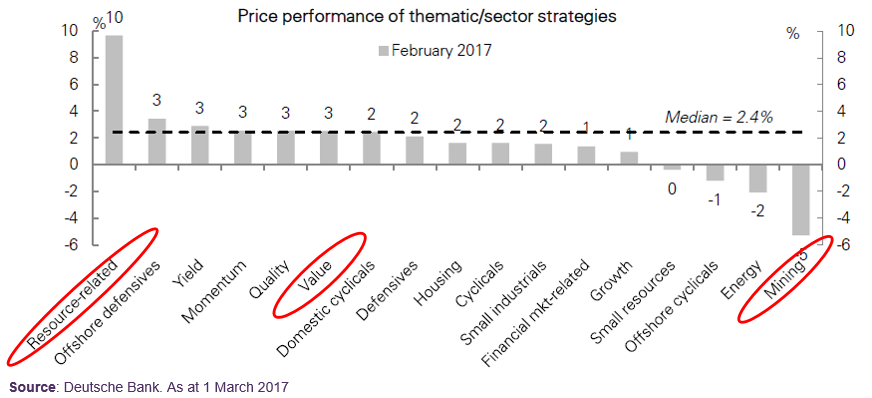

What sectors did well?

The chart below provides a helpful snapshot of which sectors performed during reporting seasons.

Despite delivering the bulk of the earnings growth resources actually did poorly in February as the improvement in commodity prices had already been priced in. The best performing sector was actually resource-related or mining services stocks which will ultimately benefit from higher commodity prices as resource companies begin spending again.

Perennial Value Smaller Companies remains well positioned here with holdings in Swick Mining (SWK), Pacific Energy Limited (PEA), Rungepincockminarco Ltd (RUL), Austin engineering Ltd (ANG), Alliance Aviation Services Ltd (AQZ) and Imdex Limited (IMD).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew commenced with Perennial Value in July 2008.

Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this time he gained a deep understanding of stocks across the small cap spectrum.

Andrew commenced his career at Tyndall in their graduate program, where he gained experience across a number of functions including accounting, product development and stock analysis. Andrew is responsible for managing the Small and Microcap portfolios at Perennial Value.

Andrew attained First Class Honours in Finance while achieving his Bachelor of Commerce degree at Sydney University.

Andrew Smith

Head of Smaller Companies and Microcaps

Perennial Value Management

Andrew commenced with Perennial Value in July 2008. Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this...

Expertise

Andrew Smith

Head of Smaller Companies and Microcaps

Perennial Value Management

Andrew commenced with Perennial Value in July 2008. Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this...

Expertise

Comments

Comments

Sign In or Join Free to comment