Cleanaway: A defensive midcap on the rise

Cleanaway Waste Management (CWY), Australia’s leading provider of waste management and environmental services, has jumped 9% after delivering a 46% increase in revenues to $1.1bn, and a 43.2% increase in EBITDA to $221m.

The uplift in revenue and earnings improvement was driven by the Toxfree acquisition, organic growth and synergy realisation.

Three key highlights from the result

-

Organic growth in 1HFY19 was very solid:

- Revenue up 9.3%

- EBITDA up 14.7%

- EBITDA margins increased to 21.5% up 100bps

Earnings quality remained sound with free cash flow up 126.5% and the FCF conversion of 95.9% was a solid outcome. Earnings quality continues to be diluted by the ongoing drag from landfill remediation payments of $12.6m, which remains in line with expectations. Capital expenditure in FY19 is expected to be c.85%-90% of D&A and guidance for this to continue next year.

The key driver of solid 1H organic growth was momentum in Solid Waste Services which benefited from the addition of the Toxfree Solids businesses, increase in landfill volumes along the east coast, and the full ramp of major contract wins namely:

- NSW Central Coast municipal contract;

- Coles

- NSW Container Deposit Scheme

- Commencement of the Brisbane City Council resource recovery contract.

2. CWY was a beneficiary of commodity pricing stabilising in 1HFY19 compared to FY18. Moreover, commodity price fluctuations have been mitigated by improved contract terms with customers.

3. The Toxfree acquisition has expanded CWY’s footprint of strategically significant infrastructure assets, enhancing the value of its vertically integrated model. Importantly, CWY re-affirmed total synergies of $35m to be realised over the next 3 years.

Our investment view

We remain positively disposed towards CWY’s investment case given its high level of earnings visibility (>80% of earnings contracted) and growth optionality across each of its businesses.

CWY’s vertically integrated waste model across collections, resource recovery, treatment and landfill afford the company with high barriers to entry in an essential industry. CWY remains well placed to benefit from structural changes to the Australian waste industry, which increasingly bestow higher regulatory imposts and a growing requirement to provide sustainable waste management solutions.

Overall group margins are likely to benefit from $35m of synergies associated with the TOX acquisition over the next 3 years, resulting in a potential uplift of 150bps.

Further investment optionality exists as CWY has retained a conservative balance sheet with a net Debt/EBITDA ratio of 1.5 times and an undemanding dividend payout ratio of 50%.

CWY is trading on a FY20 EV/EBITDA of c. 8.8 times, which compares favourably to its international waste management peer group, particularly given its ability to continue to deliver double digit earnings per share growth over the forecast period.

What the market is overlooking here

The market is underappreciating CWY’s network of waste-related infrastructure assets at a time of growing sustainability trends.

Australia’s waste management industry is benefitting from several tailwinds including growing waste volumes per capita, improving resource recovery rates, and industry consolidation.

Recent developments, notably the implementation of China’s National Sword recycling policy, underpins the growing recognition that Australia’s waste industry is actively investing in greater resource recovery, recycling and alternative waste treatment. The urgency of developing a more comprehensive waste solution was driven by China abruptly shutting its doors to receiving contaminated and hazardous waste in December 2017.

As the largest importer of recycled material globally this has heralded a paradigm shift in how the world has needed to change its thinking on recycling. In the short- term south-east Asia has been the cauldron for the worlds recycled waste but over the longer- term Australia (as with other developed economies) will need to materially lift its investment in recycling & waste energy processing facilities. Such investment requires scale and expertise highlighting the benefits of CWY’s incumbent position in Australia’s waste industry.

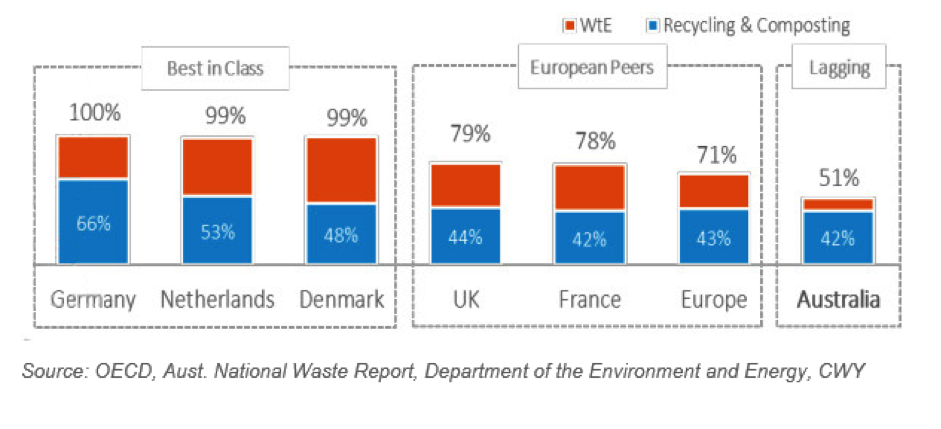

The accompanying chart (figure 1) underscores Australia’s opportunity to improve waste recovery rates and need for further investment.

Figure 1 – Recovery rates of municipal waste

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO (Asia Pacific) for Canaccord Genuity.

1 topic

1 stock mentioned

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Marcus is the co-founder and CIO of Blackmore Capital. Marcus' career spans over 27+ years focussed on Large Cap Australian Equities including work as a research analyst at McIntosh/Merrill Lynch, Portfolio Manager at Cooper Investors, and CIO...

Expertise

Comments

Comments

Sign In or Join Free to comment