Consequences of the vaccine

Pfizer and BioNTech just announced that their vaccine was over 90% effective in a trial of 43,000 people, with no major adverse safety effects.

These trials work by taking a large number of people, giving some the vaccine and some a placebo, then waiting until a predetermined number of people catch the virus. Once this number is reached, the test is unblinded and the researchers can see whether those with the virus were vaccinated or not. Of course, if the infected were in the placebo group, it's highly likely that the vaccine was protective.

A rare positive aspect of the recent surge in coronavirus cases that it has significantly sped up the time it takes for that preset number of people to catch the disease.

Readers will know we have long thought that a number of vaccines would be successful. To reiterate:

- Unlike in HIV (the poster child for tough-to-vaccinate viruses), the spike protein in coronavirus is largely unprotected.

- There have been multiple successful coronavirus vaccines in animals - just no commercial imperative to develop them in humans until now. There's no reason for them not to work.

- There have been multiple precedents for the rapid roll-out of vaccines within a year (eg Swine flu and Ebola), the awareness of which is a helpful test as to whether someone in the field knows what they're talking about.

- Most importantly, all the early stage immunological data from Pfizer, Moderna et al was consistent with the vaccines working. It would have been possible, but very strange indeed, if these vaccines provoked an immunological response without protecting against the virus.

There are concerns that the virus will mutate... but given how infectious it is, most mutations will likely weaken rather than strengthen it. And the longer it passes from human to human, the less infectious it will likely become.

This is actually an old method to develop vaccines - pass a virus through human cell after human cell until the virus adapts and becomes safe enough to provoke an immune response without causing disease.

Prospects for other coronavirus vaccines

Given that many of the vaccine candidates target the same spike protein, the success of one is highly suggestive of the prospects of the others, particularly given they target the same surface spike protein.

Usually in biotech, the winner of a race gets the lion's share of the spoils. The runners up have a more difficult task: they must prove their treatment works and that it's superior. The first treatment to market will quickly generate clinical data, physician familiarity, and have an unhindered period in which to win the hearts of medical decision-makers. There's little incentive to reason to risk trying a new treatment for a marginal benefit.

This time is different.

There is an urgent need for coronavirus vaccines today, and even with multiple companies ramping up production, demand will vastly outstrip supply. With lockdowns and travel restrictions still in place around the world, every day's delay is costly. So even a second, third or fourth successful vaccine will find a ready market waiting - and the negative aspects of Pfizer's vaccine (namely, requiring two doses refrigerated at -80 degrees Celsius) leaves plenty of room for other participants.

So we added to Moderna on this news, and the stock has now quadrupled since our initial purchase.

Implications for mRNA

We now have powerful evidence that mRNA vaccines work in humans. Again, there was little reason to doubt they would but, still this is a remarkable achievement for genetic medicine and the human race. It's (comparatively) easy to adapt mRNA vaccines to different viruses (and mutations of the same), so we have a powerful new weapon against our ancient enemy. The mRNA pipeline of a single company shows the promise:

11.png)

Winners and losers and life sciences

The corona-crisis has been a strange one for the life science community, which has never been so venerated nor well-funded. But these spoils have landed unevenly. Those fortunate to be in coronavirus research or quick enough on the pivot have done well. But those associated with, say, elective surgery in hospitals or non-lethal conditions - a large group indeed - have struggled.

Now those trends will reverse, and this is positive for some of our holdings like Progyny, which focuses on fertility. This is certainly no time to be a second or third tier coronatreatment hopeful (more than a few of these...) but the moment offers an extraordinary opportunity to invest in acyclical medical technologies.

Markets

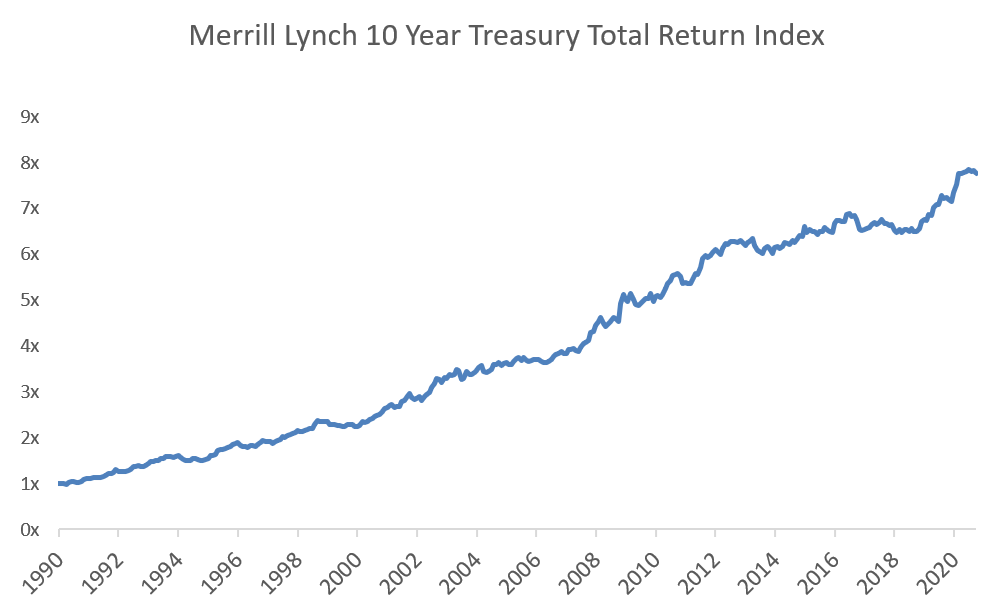

We think this is a rare turning point, the likes of which happen very rarely. Every year since the 2009 financial crisis a new set of managers call the end of falling interest rates. And as night follows day, those trades are reversed or the funds wound up soon after. It's just a terrible trade: you have to pay to hold it, it loses money at the worst possible times when equities are selling off, and it has just been directionally wrong. If you bet on interest rates rising, this is what you are actually shorting:

In other words, it's a buy not a sell. Total return charts like these look completely different to the interest rate charts which everyone uses. We can't help but wonder if a vaccine could mark the end of this four decade trend in falling interest rates. Unlikely, but certainly more possible than usual. We still don't advocate the trade!

But we are following this closely as students of market history, and also because rates drive valuations in the short term according to both theory and practice.

The last great entry point (after which many stocks increased 5x, 10x or many times more) was only two years ago, at the end of 2018, which also happened to be the last time a US central banker tried to raise interest rates. It was from these lows that many software companies increased 10x or more.

There is little prospect of rate rises now. But longer term yields have begun to rise, tech valuations are at record highs, and we believe a period of serious multiple compression has already begun, with many red hot tech stocks peaking a few months ago.

One of the reasons we focus on companies growing organically by 75% or more (often over 100%) is so the 20-30% multiple compressions become increasingly relevant with time.

And indeed, we have been able to escape the recent multiple compression this month and generate positive returns, even while the Nasdaq was down, and even amidst a violent tech rotation we are having a positive month so far, largely because we are avoiding overpriced sectors and the organic growth rates of our portfolio companies is truly exceptional.

The unnervingly simple investment lesson of the last 15 years is to hold fast-growing innovative companies improving our world through thick and thin.

It has been far riskier not to own these companies.

Portfolio

With that in mind, you can be assured in times like these we are as steady as always, and will use such moments to buy, not to sell. But we are not ones to let opportunities go to waste. We're taking advantage of the changing state of affairs in three ways:

Firstly we are increasing our investments in the life sciences. Decades of painstakingly difficult and pedantic work in laboratories all around the world has lifted the state of genetic technology to science fiction level. These foundational technologies are creating extraordinary new greenfield opportunities.

Many companies in the life sciences are coming off epidemically-depressed revenues, are cyclically defensive, and have growth rates as high as any in tech.

Secondly, we are dramatically reducing what little we have left invested in 40x revenue businesses. These have generated spectacular returns for us, but have now graduated into 'lower return prospects'. We are focused on the next set of opportunities in the $1 billion - $20 billion market cap range growing at >100%.

Thirdly, we are adding travel to one of our themes, where it joins renewables, software, life sciences, fintech, online retail and digital health. Rest assured we still hold our Disney shares.

We believe that the best year in travel on record will shortly start, and intend to be there for it.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

........

The information in this note has been prepared and issued by Frazis Capital Partners Pty Ltd ABN 16 625 521 986 as a corporate authorised representative (CAR No. 1263393) of Frazis Capital Management Pty Ltd ABN 91 638 965 910 AFSL 521445. The Frazis Fund is open to wholesale investors only, as defined in the Corporations Act 2001 (Cth). The Company is not authorised to provide financial product advice to retail clients and information provided does not constitute financial product advice to retail clients.

The information provided is for general information purposes only, and does not take into account the personal circumstances or needs of investors. The Company and its directors or employees or associates will use their endeavours to ensure that the information is accurate as at the time of its publication. Notwithstanding this, the Company excludes any representation or warranty as to the accuracy, reliability, or completeness of the information contained on the company website and published documents.

The past results of the Company’s investment strategy do not necessarily guarantee the future performance or profitability of any investment strategies devised or suggested by the Company.

The Company, and its directors or employees or associates, do not guarantee the performance of any financial product or investment decision made in reliance of any material in this document. The Company does not accept any loss or liability which may be suffered by a reader of this document.

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

Michael manages a global equity investment fund focused on technology and the life sciences. Michael completed undergraduate and graduate chemistry degrees at Magdalen College, Oxford University, and studied finance at the London School of Economics

Comments

Comments

Sign In or Join Free to comment