No virus for global stocks

As Chinese workers slowly make their way back to factories and offices across the country, global stockmarkets are hitting all time highs. For all of the headlines and media attention, investors seem to have taken the Coronavirus crisis in their stride. It’s been surprisingly proportional and light on opportunity.

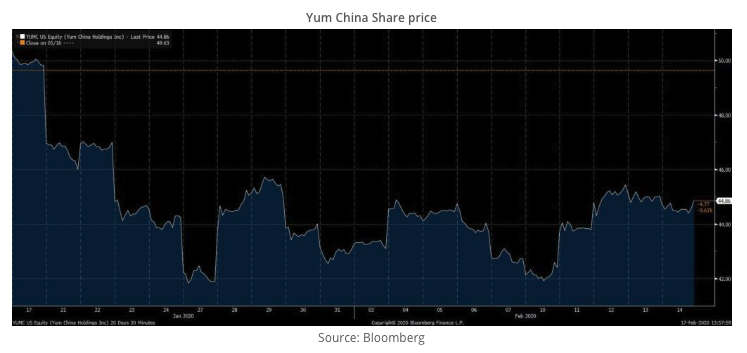

Take Yum China as an example. Yum is an investment in our Forager International Shares Fund that owns KFC and Pizza Hut in China. The stock fell about 16% from its peak on 20 January through to the trough on the 27th. As the rate at which the virus has spread slowed, the share price has bounced some 7%, leaving it roughly 10% off its January highs.

You could argue that’s overkill. Results for the December quarter were better than expected. And, on our numbers, the impact on valuation could be as little as 2% (assuming they lose about half this year’s profits).

But the tail risks are clearly heightened. The most likely case might be only 2%, but the probability of something dramatically worse is far higher than the probability of something better. We have added a little to our holding, but the market response seems a perfectly sensible reaction.

With a couple of minor exceptions, that has been true across our portfolio. And I’d argue it’s been true across the market as a whole. Investors have reacted perfectly sensibly to a significant event that is still unlikely to have a dramatic impact on the value of equity markets.

I’d also argue that this has become a more common feature of equity markets over the last decade. Investors are not panicking as much as they used to. For those of us who thrive on others panicking, that isn’t good news. But there might be good explanations for it.

Index versus closet passive

The first is the rise of index funds. Computers run these “passive” tracker funds, and they don’t feel emotions. They don’t do anything when something like Coronavirus hits the front page of the papers. If Yum China’s share price is down 16%, it is down 16% in the index and the tracker fund alike. Absent inflows and outflows, the computer is going to put its feet up and do nothing for the day.

Of course, the humans who make the decisions that lead to inflows and outflows are still guilty of the same fear and greed as the rest of us. But most of the money has shifted from what I call closet index funds—fund managers pretending to be active but largely tracking the index and charging active fees for it. These closet index huggers used to get the same flows as the tracker fund, but layered their own pro-cyclical human emotions over the top.

When the next liquidity crisis comes along—one driven by redemptions—the computers will be contributing to it. Until then, you can expect less volatility.

Hedge funds and the data explosion

Another argument for the relatively benign reaction to this crisis is the dramatic rise of big data over the past decade.

Ben Graham was getting an edge through alternative data sources in the 1950s. Trying to find indicative information that isn’t released to the stockmarket is nothing new. But access to supercomputers, cloud computing and an explosion in the amount of data being created (mostly thanks to some 3.5 billion smartphones currently used around the world) have transformed alternative data into a multi-billion dollar industry.

The statistics being released by China’s government might not be particularly trustworthy, but the data gathered by New York’s giant hedge funds is getting more and more reliable. In the past, a vacuum of information like we have had about the Coronavirus would cause share prices to fall. Today, Yum China’s share price is likely to be a better guide to the severity of the crisis than the data you’re reading in the paper.

From fairly early on, equity prices have assumed that this latest version of the deadly respiratory virus was relatively benign. Without diminishing the deaths of almost 2,000 people, that reaction is increasingly looking accurate. And it’s unlikely to be a fluke.

TINA to the rescue

Then, of course, there is TINA. There Is No Alternative to equities. With returns hard to come by in any other asset class, any dip in equities prices is seen as an opportunity to invest. Argue what you want about the merits or otherwise of this philosophy, the sentiment is undoubtedly applicable in today’s markets. It has to contribute to downturns being shorter and recoveries sharper than they have been in the past.

This is a market driven by low rates and liquidity. That’s not something a virus will bring unstuck.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and redemptions. Steve focuses on long-term investing in undervalued, underappreciated and sometimes unloved companies.

.jpg)

.jpg)

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Steve began Forager Funds in 2009, and now manages approximately $470m across two funds. The Forager Australian Shares Fund and Forager International Shares Fund are both unlisted and are available to investors with daily applications and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets