How focused minds and concentrated portfolios can outperform

Adrian Warner

Avenir Capital

As investors, there is natural and strong preference to consolidate around accepted ‘norms’, or that which becomes a guideline for what is considered normal. And today we witness the arrival of the true mega-fund managers as fund groups rush headlong into wedlock.

Much like previous periods of mega-mergers in other industries, a key driver has been price collapse, excess supply and a need to cut costs. Unlike the ‘big oil’ mega-mergers of the 1980’s when the oil price was low and could recover with volumes, it is hard to see the trend to lower management fees abating.

These new mega funds management companies are now beholden to maintaining funds under management, sales and market efforts, rising markets and reducing cost. There is also a belief that clients benefit from just a few strategic global relationships.

However, there is a key question that must be asked - can funds management be scaled to infinite scale and deliver for investors the very best investment results? Are the leaderships of these firms as focused on investment culture and supporting investment teams to excel than meet short term-performance, flows and costs?

On the flip side, can a specialist investment firm starting out today ever hope to compete with the resources of monolithic institutional fund managers that make up the bulk of the money management industry?

We hope for investors long-term wealth creation and preservation that the answer is and continues to be a resounding yes.

With gargantuan scale must come a set of headwinds to focused active investment management.

Firstly, institutions inevitably become giant marketing and distribution machines, specialists at making it as easy as possible for clients and gatekeepers to access their capabilities.

Performance becomes just one characteristic of an institutional investment manager but necessarily loses some of the vital imperative it does in a focused investment manager.

It is possible that moderate performance outcomes are enough when backed by a well-known brand name. Clients and gatekeepers will be comfortable recommending well-resourced institutions.

There is a real risk here that we perpetuate a ‘relative performance derby’ forcing fund managers into making short term decisions to optically fit the benchmark in the short term.

Team Size is no Impediment to Success

Markets are not efficient and that can no surer be demonstrated than by the creation of conflicting interests by mega-mergers in the funds management industry.

Nimble, smaller investment teams are afforded the luxury of a simpler organisation structure where they can process investment decisions in a less bureaucratic manner. Rolf-Banz in the early 1980’s identified the relationship between small-firm and higher average returns. Could the same become as true in funds management over the next 10 years?

An experimental studyi of team size and performance on a complex task, showed that per-capita productivity decreases with team size, which is to say individual effort declines as teams grow and that ‘social loafing’ as was described increases.

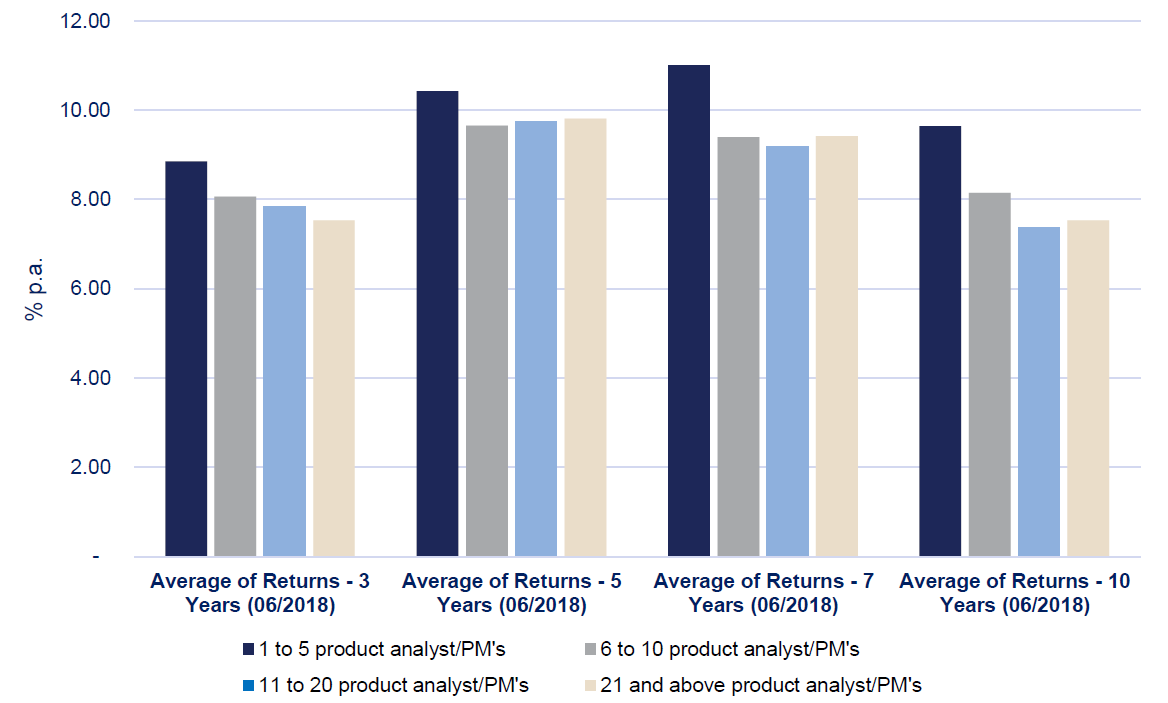

To investigate this ourselves, we used data from eVestment to screen for global equity fund managers with a value investing style that disclose the number of investment analysts and/or portfolio managers by each product or strategy in their organisation.

Global value equity is a good test case for an initial enquiry into whether team size affects performance as it necessarily involves investing against market consensus amidst a very wide opportunity set.

Presenting these datapoints below shows that the best performing strategies are clustered around smaller team sizes. In fact, the best performing strategies generally had only a handful of research analysts and/or portfolio managers (1-5).

Figure 1: Global value strategy total returns by team size category

Source: eVestment. Total sample size of 151 products classified as Global All Cap, Large Cap or Small Cap Value Equity who identify as Fundamental managers. Category sample sizes are 38 (1-5 analysts/PMs), 33 (6-1 analysts/PMs), 32 (11-20 analysts/PMs), 48 (21 and above analysts/PMs). Where Returns are in product base currency to June 2018.

Numerous academic papers have supported this relationship. Kostovetsky and Manconi (2016)ii found through a regression analysis that more advisory and research personnel do not equate to increasing mutual fund returns.

They found that while more human capital is not associated with better performance (controlling for assets under management), having more advisory personnel helps attract more assets, justifying their salaries from the point of view of the firm.

Managers of large global funds often use vast teams as a selling point to investors, although a common-sense view of this dynamic leads one to question how a very large team of analysts or PMs trying to get their ideas into the portfolio leads to better performance outcomes.

In his 1965 partnership letter Warren Buffett articulates this timeless idea best:

“It is close to impossible for outstanding investment management to come from a group of any size with all parties really participating in discussion.”

What Really Matters is Investment Conviction

Investment conviction comes from the analysis undertaken and the impact that has on the decision to invest and the decision as to what the correct size to hold that position should be.

The now eponymous paper by Cremers and Petajisto, that looked at Active Shareiii cuts through a lot of noise and pinpoints that unless you are active, unless your bets are differentiated from the market that your chances of outperformance diminish rapidly.

They used the concept of ‘Active Share’ which can be loosely defined as that portion of your portfolio that deviates from the underlying index. The findings were very instructive. Newer funds, with a strong incentive to perform well and get noticed, had a higher percentage of Active Share.

But, with increased success and increased assets under management, an interesting trend began to emerge - the portion of a fund manager’s portfolio attributed to Active Share began to decline or shrink.

As fund managers build a franchise and develop corporate needs that they need to protect, and as the management fee they generated grew with fund size, they switched to playing the game to not lose rather than playing to win. This means looking more and more like the index over time. Subconsciously, or not, they began to closet index.

Boutique Value Managers – Where Active Share and Nimble Teams Meet

Further evidence of this phenomena can be found in a 2017 study conducted by Fidante Partners, our distribution and administration partner, on the outperformance of boutique investment management firms over their institutional counterparts.

Boutique investment firms are typically small, nimble and majority owned by the portfolio managers. This ensures they have strong alignment with their investors, take a long-term business and investment perspective and are truly active, high-conviction investors.

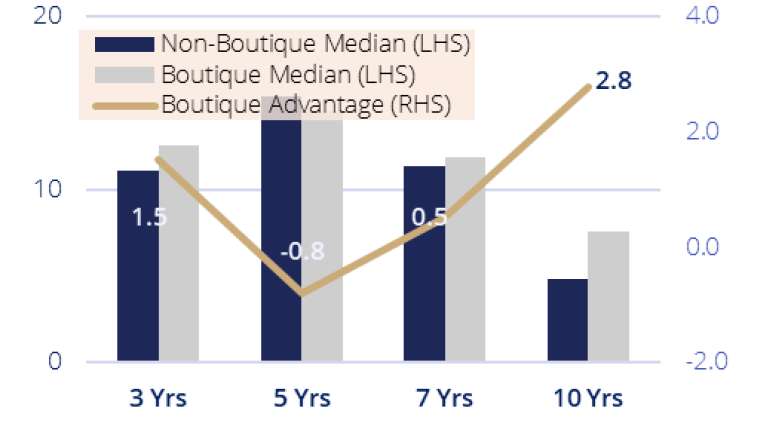

Fidante Partnersiv examined the after-fee performance of approximately 198 global equity investment strategies available to Australian investors using after fee performance data sourced from Australian investment consultant Zenith Investment Partners.

Global Equity Boutiques not only outperformed their benchmarks, they also outperformed Non-Boutiques by 0.5% p.a. over 7 years and 2.8% p.a. over 10 years.

Figure 2: Global Equity Boutiques vs. Non-Boutiques

Median Global Equity Boutique & Non-Boutique annualised median performance to 30 April 2017 (net of fees). Source: Fund managers, Zenith Investment Partners.

Global equity boutiques were found to outperform non-boutique managers over nearly all trailing periods.

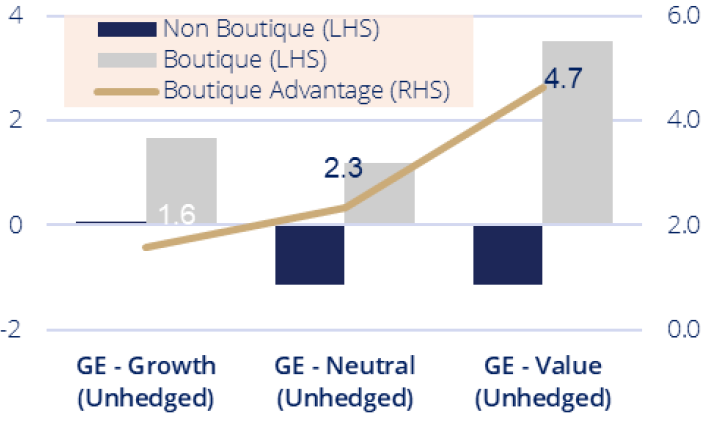

Furthermore, when this was examined by investment style over 7 years, the results show that the global equity value investment firms benefited the most from the boutique structure.

Boutique Global Equity managers outperformed Non-Boutiques across all styles over 7 years. The median Global Equity Manager outperformed Non-Boutiques by 2.9% across all investment styles.

Figure 3: Global Equity Boutiques vs. Non-Boutiques - by Investment Style

Boutique & Non-Boutique annualised median performance vs. benchmarks per investment style over 7 years to 30 April 2017 (net of fees).

Final Thoughts

With the rise of passive investment in the last decade and the resulting increase in fee competition, it has become vital active funds are truly active and not closet indexers charging a fee. Investors seeking to get the most value from their active fee budget would be wise to consider whether they are being seduced by big brand fund managers with their impressive organisation charts and glossy marketing material.

Performance is performance, there is no arguing with that, and compelling evidence is beginning to emerge that being bigger team sizes doesn’t necessarily translate into superior long-term performance. It can be a courageous decision by an allocator to back a small investment team or firm, but those that do may find their clients thanking them in years to come.

By Adrian Warner – Managing Director and CIO, Avenir Capital and Sam Morris, CFA – Investment Specialist, Fidante Partners.

Avenir Capital is a value-based investment manager that brings a long-term, owner-oriented approach to global public equity markets. For further insights from the team, please visit our website

i Mao, A, Mason W, Suri, S and Watts, D. (2016) An Experimental Study of Team Size and Performance on a Complex Task US National Library of Medicine National Institutes of Health.

ii Kostovetsky, L., & Manconi, A. (2016). On the Role of human Capital in Investment Management. Retrieved from SSRN: (VIEW LINK)

iii. Cremers, Martijn and Petajisto, Antti, How Active is Your Fund Manager? A New Measure That Predicts Performance (March 31, 2009). AFA 2007 Chicago Meetings Paper; EFA 2007 Ljubljana Meetings Paper; Yale ICF Working Paper No. 06-14. Available at SSRN: (VIEW LINK) or (VIEW LINK)

iv Fidante Partners, The Boutique Advantage (2017)

The information in this article has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this article, whether express or implied, including the case studies, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Avenir Capital (“Avenir”) (ABN 40 150 790 355, AFSL 405469), Fidante Partners Limited (“FPL”) (ABN 94 002 835 592, AFSL 234668) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, neither Avenir nor FPL nor any of their directors, officers, employees or agents accepts any liability (whether in negligence or otherwise) for any errors or omissions contained in this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in Australia, Asia and the United States with an investment record spanning over 20 years.

Adrian Warner

Chief Investment Officer

Avenir Capital

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in...

Expertise

Adrian Warner

Chief Investment Officer

Avenir Capital

Adrian Warner is the Managing Director and Chief Investment Officer of Avenir Capital and is responsible for the portfolio management of the Avenir Global Fund. Prior to founding Avenir Capital, Adrian worked in private equity investment in...

Expertise

Comments

Comments

Sign In or Join Free to comment