Defending against uncertain markets

Laura Bottega

Morgan Stanley IM

Explorer Sir Ranulph Fiennes is known to have said, “There is no bad weather, only inappropriate clothing.” This seems particularly apt at the moment as global investors approach us regularly looking for comfort for the year ahead.

It has become fashionable to access global equity markets broadly, passively, synthetically, particularly while markets have continued their upward trajectory. Late cycle investors considering a potentially bumpier ride for markets ahead, and a more complicated corporate and geo-political landscape, may wish to revisit the attractions of truly active investing to bridge any potential yawning chasms or gorges ahead. Benchmarks, in our view, are inherently risky; simply seeking to match index performance creates a false complacency. Active investing, particularly in the hands of disciplined and experienced managers, offers the chance to be prepared, to identify earnings resilience, and achieve meaningful long-term outperformance.

The essence of active investing

The escalation of trade tensions between the US and China and political tensions with Iran, Brexit uncertainty, an impeachment in an election year, and more recently the coronavirus have all contributed to volatility over the last year.

Active investing is essential in a market with peak earnings and multiples.

We cannot influence or even predict the macroeconomic or political environment, but we can aim to ensure that the stocks we hold are the most robust we can find. Our investment team is focused on selecting high quality stocks that will grow capital over the long term and seek to minimise the chance of any permanent loss of capital. We call such well-managed high and sustainable return on operating capital companies with growth potential and resilient earnings, “compounders.”

These companies are fairly rare so, when we buy them, our conviction is reflected in meaningful position sizes, up to 10% of a portfolio, and an active share for a portfolio of greater than 90%. The advantage of a portfolio of such stable compounders is evidenced by the Global Franchise strategy’s 24-year track record of long-term capital appreciation at lower long-term volatility than that of broad benchmarks.

Engaging with sustainable compounders in a more complex world

Our investment strategy has always centred on capital light companies with strong intangible assets, such as brands or networks, which enable pricing power and steadily growing revenues, robust profits, strong free cash flows, and a steady dividend.

As active investors, we are ever vigilant to the changing consumer and competitor landscape and mindful of potential risks to the sustainability of long-term returns on capital. This includes material ESG risks as well as material opportunities ESG can present to the companies we own. Our portfolio managers analyse material ESG factors themselves as part of their bottom-up fundamental research. We believe that incorporating ESG is essential to long-term compounding, helpful in identifying sustainable compounders and picking the winners from the losers.

As active investors, we are ever vigilant to the changing consumer and competitor landscape and mindful of potential risks to the sustainability of long-term returns on capital.

How do some of the world’s most famous branded companies continue to dominate mind share and market share in an ever more disruptive world of e-commerce and social media? It is a question on which we have become increasingly focused. The answer for consumer goods companies lies in staying relevant to the consumer’s changing preferences and values, for example the use of natural or organic ingredients or more environmentally friendly packaging. Consumer goods companies that stay relevant can gain market share and maintain pricing power over competitors who do not. This often results in rising long-term returns as a consequence. Further, governance structure really matters – we typically prefer agile and decentralised management teams that can react to local market conditions, choose to invest in their franchises and do not squander free cash flow on low return acquisitions.

Not all strong franchise companies are consumer brands. Recurring revenues from networks can also mean compelling stability of earnings, even more so with the shift to the cloud. For the software and IT services companies in which we choose to invest, staying relevant means supporting other businesses in their changing digital needs and being cautious with the use of data. Medical technology has also offered new ground for us to identify robust recurring revenues in areas such as medical equipment. life sciences and diagnostics.

Importantly, we do not analyse companies from a distance. Portfolio managers handle proxy voting directly, meeting regularly with the senior management, board members and remuneration committees of companies we own, and engage where we must. Often that means focusing on incentive structures, which in our view can be critical to the decisions of management, or checking management’s awareness and agility on their company’s environmental or social footprint or the shifting tide of opinion from regulators and consumers on data protection and antitrust.

An active portfolio to defend against today’s uncertain markets

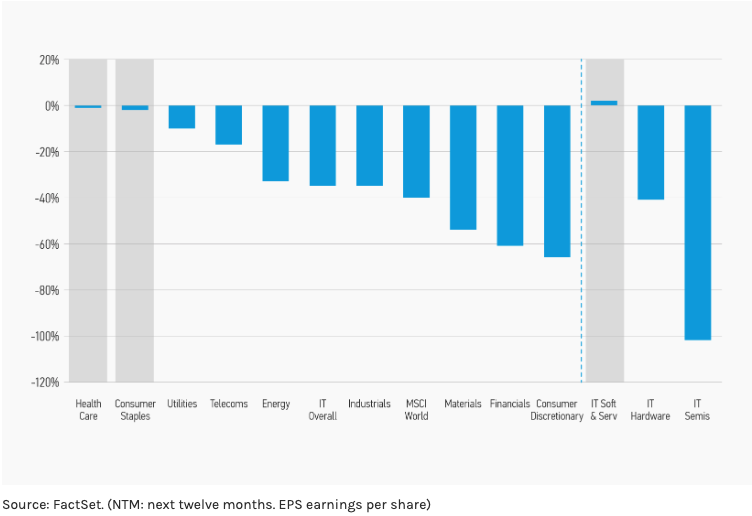

High quality companies are by their nature less exposed to potential adverse events, as demonstrated by our strategy’s history of relative outperformance in down markets. Even more interesting perhaps is a closer look at the sustainability of earnings across different sectors during the last financial crisis. Earnings of software and services companies were up 2% over 18 months, against a 40% fall for the MSCI World Index, while health care and consumer staples were only down marginally (Display 1).

With our portfolio’s primary skew to these high quality defensive sectors, it gives us some comfort going forward that we believe our portfolio earnings are likely to hold up better than the market as a whole.

Political uncertainty, increasing regulatory scrutiny, climate change and rapid advances in technology – the conditions for companies’ continued success are ever more complex. In this changing world, global equity investors should be looking for companies that are robust and for disciplined and engaged portfolio management teams that can help them conquer their fear of falling.

Seek long-term outperformance

At Morgan Stanley Investment Management we strive to deliver distinct, innovative strategies that can mitigate risk during market downturns.

Hit the FOLLOW button below to be notified by email as soon as I publish my next wire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Laura is the lead portfolio specialist for the Global Franchise, Global Quality and Global Sustain strategies and a member of the International Equity team. She joined Morgan Stanley in 2006 and has 21 years of investment experience.

Featuring

Laura Bottega,

Morgan Stanley IM

Laura is the lead portfolio specialist for the Global Franchise, Global Quality and Global Sustain strategies and a member of the International Equity team. She joined Morgan Stanley in 2006 and has 21 years of investment experience.

1 topic

Laura Bottega

Lead Portfolio Specialist

Morgan Stanley IM

Laura is the lead portfolio specialist for the Global Franchise, Global Quality and Global Sustain strategies and a member of the International Equity team. She joined Morgan Stanley in 2006 and has 21 years of investment experience.

Expertise

Comments

Comments

Sign In or Join Free to comment