Dirty poker

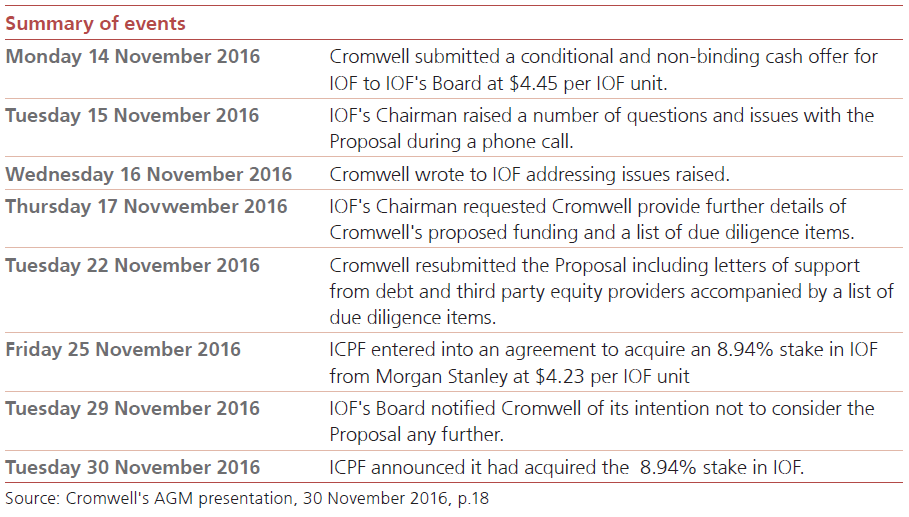

In April 2016, I wrote about Dexus's (DXS) bid to acquire the Investa Office Fund (IOF) and how rival Cromwell (CMW) acquired a 9.8% stake in IOF (at $4.24 per share) that assisted in defeating the proposal. Fast forward to December and CMW revealed they had approached the Board of IOF to purchase the Fund with an all-cash offer of $4.45. Interestingly, this announcement did not come from IOF but rather from CMW, two weeks after it first approached the Board and after a related but separate party of IOF had purchased an 8.9% stake at the materially lower price of $4.23.

Pat Barrett

UBS Asset Management

In simple terms the timeline went like this:

IOF’s Board dismissed the A$4.45 all-cash offer as not attractive or compelling and questioned CMW's ability to finance this deal, thus the Board chose not to disclose it. Whilst it was highly conditional and non-binding, as a unitholder I believe it would have been prudent to tell the market. It's not as if the bid came from a private equity firm (recall the infamous David Jones's $1.6bn takeover bid in 2012), but rather from a listed and respected ASX rival. I wouldn’t be too happy if I had sold a major stake below the proposed offer. Expect many questions to the Board about IOF’s corporate governance and why investors should now support their mooted plans to internalise.

Written by Pat Barrett, Property Analyst, UBS Australia: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

1 topic

2 stocks mentioned

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

Ross vs the AI hype: her shocking prediction revisited

Livewire Markets