Dissecting the fear-to-fact ratio: A case of irrational markets?

Frank Uhlenbruch

Janus Henderson

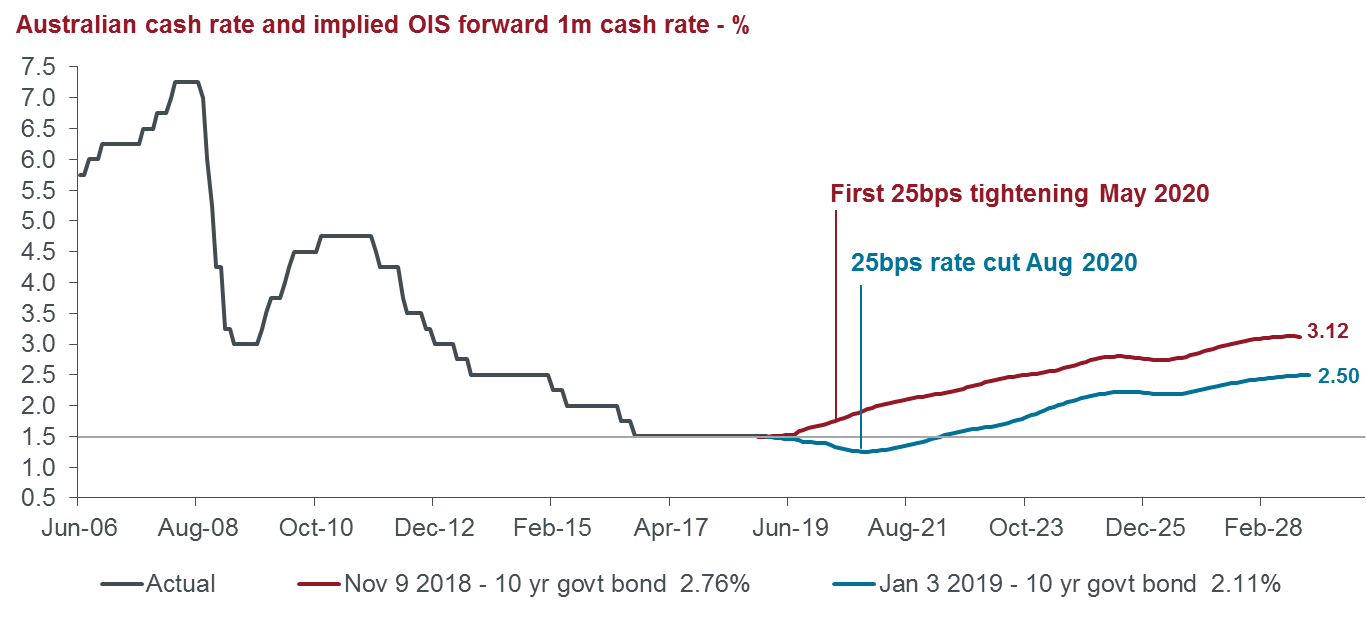

It was only mid-November when the US and Australian 10 year government bond yields nudged 3.24% and 2.76%, respectively, and local markets were pricing in no chance of a rate cut from the Reserve Bank of Australia (RBA) and a rate rise in May 2020.

Yet in early January, the Australian 10 year government bond yield rallied down to as low as 2.11%, (only 30 basis points (bps) above the 2016 generational lows of 1.82%) and markets moved to fully price in an easing by August 2020.

Typically, such large moves are driven by a profound negative economic shock which sees risk appetite decline and markets reassess the path of cash rates. Sometimes markets can over-react to a change in state, with negative sentiment feeding on itself and a temporary loss of confidence, or low seasonal market liquidity conditions, compounding moves in asset prices or yields.

So what’s behind the recent rally? Declining fundamentals, poor sentiment, or a mix of both?

There is no doubt that there was a slowing in global and domestic growth over the latter part of 2018, but it appears the market’s adjustment to this was exaggerated by political dramas and a decline in market depth over the Christmas and New Year period.

We see recent volatility leading to offshore central banks delaying any tightening plans, which in turn, will help stabilise sentiment and activity levels. Our view is that the RBA will respond to recent developments by signalling confidence in the domestic outlook and the stabilising role that it can play by leaving the cash rate unchanged at accommodative levels until it sees signs of wages lifting.

Fundamentals point to a delay and watering down of tightening expectations, fully pricing in an easing reflects excessively bearish sentiment that should unwind as economic outcomes are not as dire as expected.

Source: Bloomberg, Janus Henderson Investors. As at 31 December 2018

You can read further insights and analysis from the team at Janus Henderson here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Frank Uhlenbruch

Janus Henderson

Expertise

Frank Uhlenbruch

Janus Henderson

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets