Does the Chinese banking system reduce or increase systemic risk?

There has been a material amount of discussion regarding private debt levels in China and the potential risks that these may pose to the financial system. Determining the risk is complicated by the Chinese banking system differing materially from that operating within many developed countries. But do these structural differences increase or decrease the level of systemic risk within the Chinese financial system?

How concentrated is banking in China?

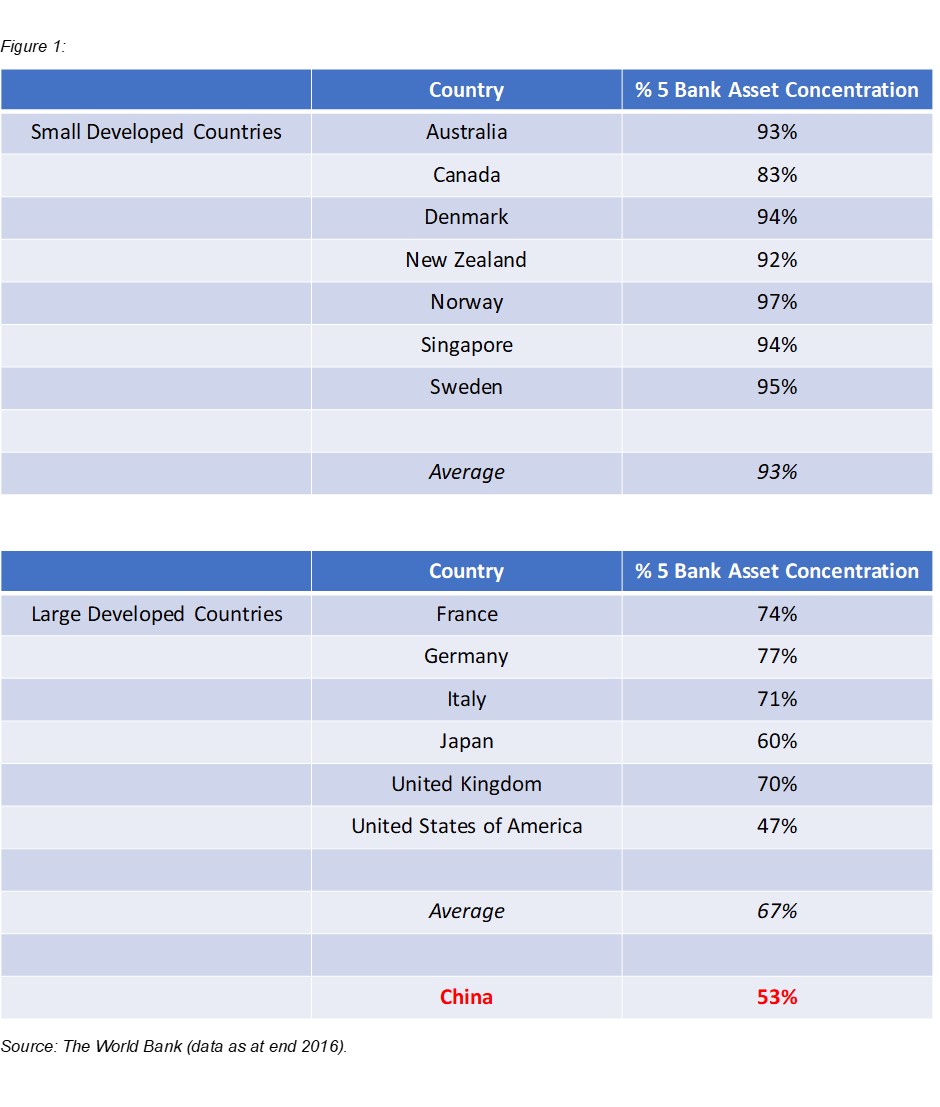

An initial approach to measuring the level of systemic risk within a country’s banking system is the level of asset concentration; i.e. all else being equal, the more concentrated the banking system the greater the level of systemic risk. This can be measured by using the % 5 Bank Asset Concentration data collected by the World Bank. As the level of bank asset concentration will vary depending by:

(a) size of the country

(b) its level of ‘development’

the table sets out the results for a selection of small and large developed countries.

Cross sectional comparisons demonstrate that the level of asset concentration tends to be materially higher in smaller developed countries versus their larger developed peers. Comparing China to the average subset of large developed countries highlights that the level of bank asset concentration is materially lower. This metric suggests that the level of systemic risk in China should be lower than the average developed country.

Structure of the banking system within China

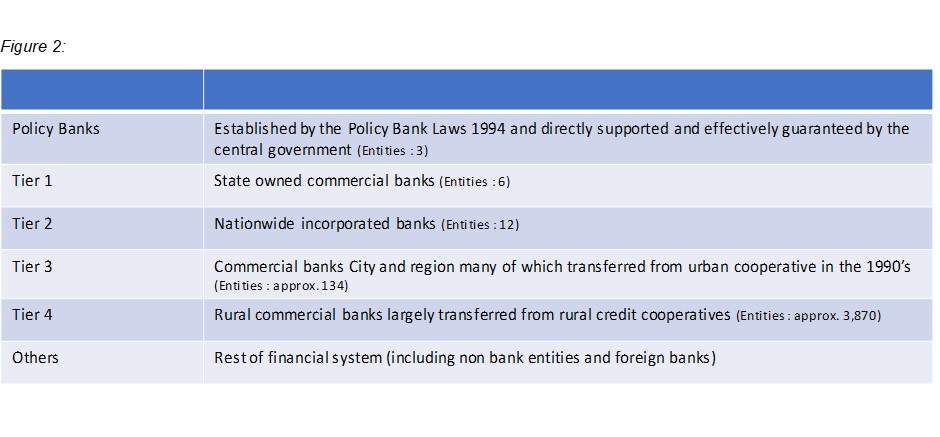

Though a useful guide, asset concentration is only part of the answer. It’s also necessary to take a closer look at the structure of the Chinese banking system to better appreciate the drivers of systemic risk. To understand the Chinese banking system, one needs to recognise that the current structure is the by-product of the economy’s evolution from a centralised command economy to one incorporating the needs of a growing private sector. Given this evolution, the Chinese banking system is best considered in terms of ‘Tiers’. The main ‘Tiers’ are:

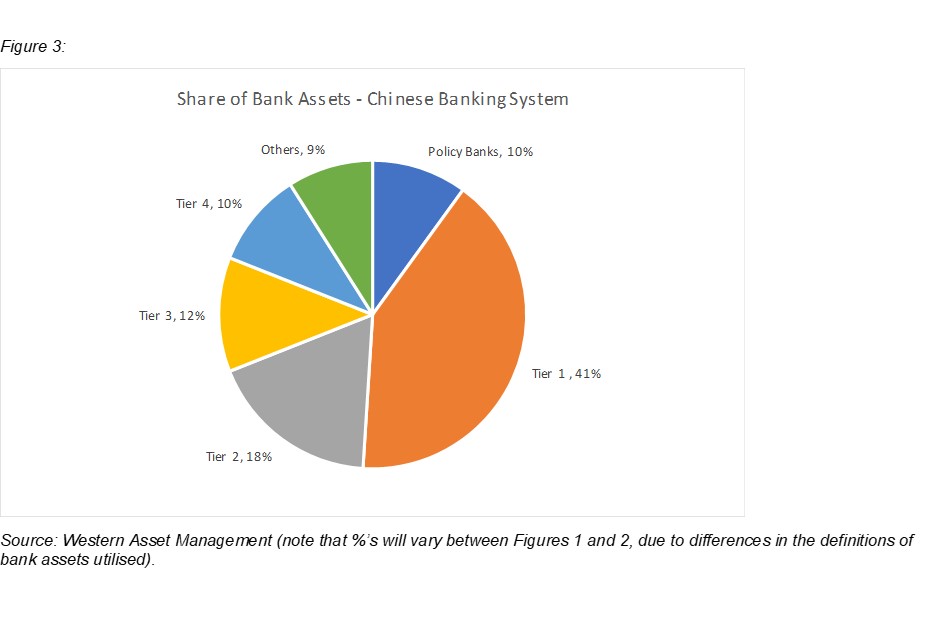

The proportion of banks assets controlled by each Tier, and its relative importance at a macro level, is set out in Figure 3.

Taking the data at face value the top three banking Tiers control nearly 70% of bank assets. This can be misleading given that unlike banking systems in many developed countries the different Tiers of Chinese banks are more specialised in the form of lending they undertake. This difference in structure is due to the way that the Chinese banking system has evolved over time. Tier 1 and Tier 2 banks predominantly focus on providing finance to the local governments and state-owned enterprises. When they do lend to the private sector it’s generally only to larger higher-quality borrowers. This historical bias is due to the evolution of the state-owned banks to service what was basically a state-controlled economy. By contrast lending to the private sector evolved within a more regionally fragmented framework based upon city and rural cooperatives. These co-operatives developed the ‘grass roots’ knowledge of the local borrowers and developed the associated infrastructure to be in a position to extend credit within the region they covered. Over time these cooperatives were converted into banks becoming Tier 3 and Tier 4 banks. Given the fragmented nature of the Chinese regions these banks have tended to maintain their regional biases.

There is one final piece to the Chinese banking structure which is important to understand to help appreciate the level of systemic risk and that is the provision of liquidity. It may appear that Tier 1 and Tier 2 banks do not have a large exposure to private sector lending, however this is somewhat misleading. It is misleading in that Tier 3 and Tier 4 banks rely quite heavily on the domestic money markets to provide funding. The major providers of funding to these banks via the domestic money markets are the Tier 1 and Tier 2 banks. The overall result is a banking system where a large part of the market is controlled by the top Tier banks making relatively low risk loans and providing liquidity to the lower Tier banks where the higher risk private sector loans are concentrated. As a result of this evolutionary path the different Tiers of banking compliment, rather than compete, with each other’s lending activities; i.e. each Tier is quite specialised in the form of lending and services it provides.

Does this structure make the Chinese banking system more, or less, vulnerable to shocks?

Making a categorical conclusion regarding the level of systemic risk is problematic for any banking system. There are reasons for believing that the Chinese banking system may be less exposed to systemic risk compared to its developed market peers. Within developed market banking systems the banks compete with each other and consequently encompass a broad range of exposures to a wide spectrum of borrowers. This free market approach to competition also means that the exposures within the loan book of each major bank will tend to mirror the borrowing requirements of the overall private sector with a similar mix of exposures existing for each major bank. This increases the risk that a material liquidity event in one major bank, whether associated with an increase in defaults or not, will signal a broader issue facing the entire banking system. For developed governments trying to manage systemic risk, this increases the risk of needing to provide across the board support for the entire banking system. The increased scale of support the government will be required to provide, and the commensurate strains on public finances, may in turn result in the market questioning whether the government has the facilities to maintain such ongoing liquidity support; i.e. the breadth of public support required may undermine perceived credibility or sustainability of the promised support.

By contrast the more segmented nature of the Chinese banking system makes it easier for the central government to ‘quarantine’ liquidity events within the financial system. Issues within the riskier private sector loan market are concentrated within the lower Tier banks. Any liquidity issues faced by these banks will only occur if the top tier banks cannot provide ongoing funding. The top tier banks, having lower risk loan books, are less likely to face their own liquidity constraints thereby reducing the risk of contagion from any issues facing the lower tier banks. Though it could be argued that the large number of lower tier banks makes managing risk more difficult even here the exposures are diversified. Given their more regional focus, the issues are more likely to be localised with respect to default risk and therefore less likely to represent broad based systemic issues. The more segmented nature of the Chinese banking system reduces the risk of issues within a single bank spreading to create a more broadly-based systemic event within the financial system. Even if there is a material increase in private sector defaults, the structure of the banking system reduces the risk that this will spread to become a more broadly-based systemic event, which is beyond the capabilities of the central government to manage.

Though there have been concerns over private sector debt levels within China, the nature of the Chinese banking system helps reduce the risk of systemic risk within the financial system. With a more segmented bank loan market, liquidity/default events are easier for the government to quarantine and isolate, reducing the threat of them becoming more systemic in nature. Such a structure gives the Chinese central government greater flexibility to deal with shocks to the banking system arising from the private sector, compared to developed countries where the larger overlap of banking activities increases the risk of events within one major bank flowing onto other major banks. This is not to say that there are no potential risks to the Chinese banking system. Rather, given its structure and unlike the banking system in most developed countries, any shocks which are large enough to create systemic risk within the Chinese banking system are more likely to emanate from the government itself rather than the private sector.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment