Earnings Season Observations

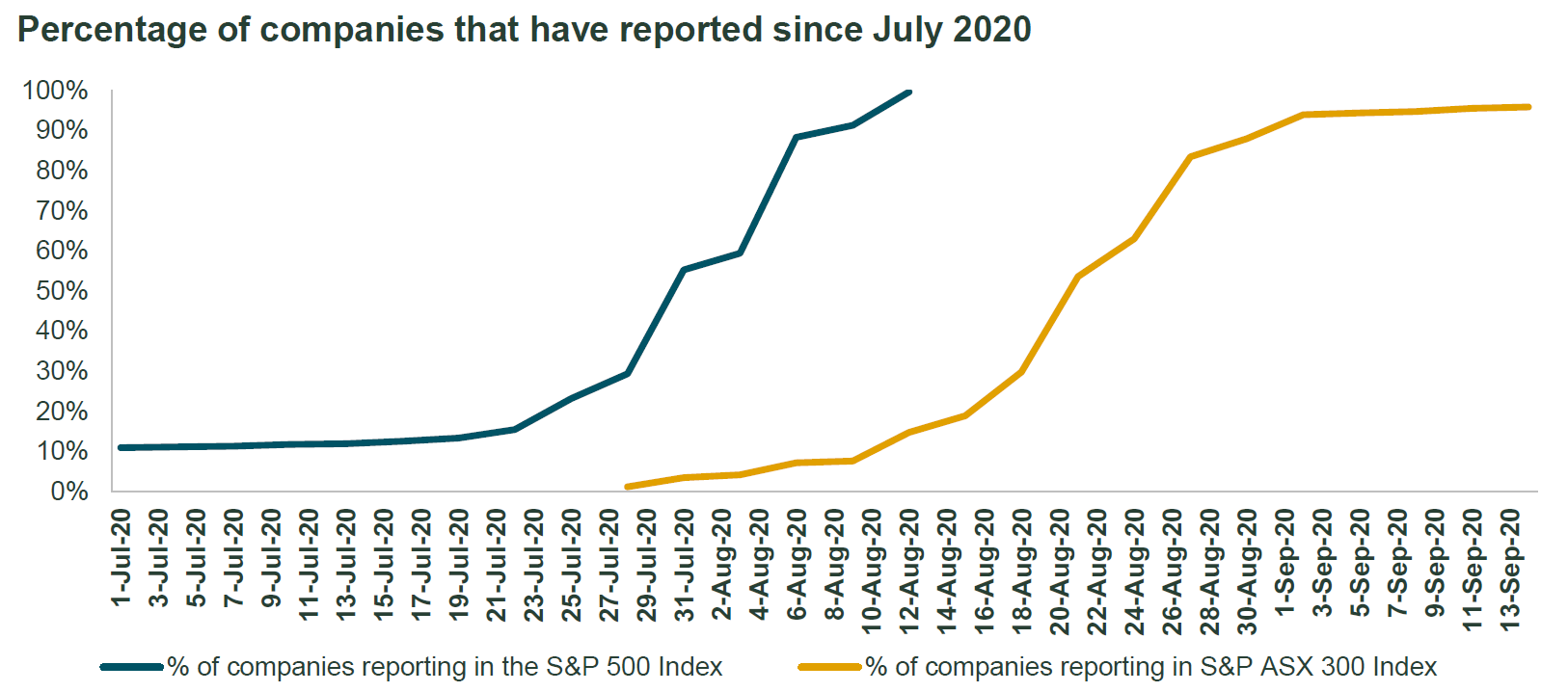

The investment landscape remains particularly uncertain at the moment. We are observing a wide range of economic forecasts and a large degree of earnings uncertainty. Implied volatility remains elevated across the developed and emerging equity markets. Earnings uncertainty remains high with many companies continuing to withhold guidance. US companies have recently completed earnings season and the Australian reporting season is ramping up. In this note we take a closer look at some of the recent earnings trends from the US and Australia.

Figure 1. As the US reporting season finishes the Australian reporting season steps up

US Earnings Trends Offer Signs of Stabilisation

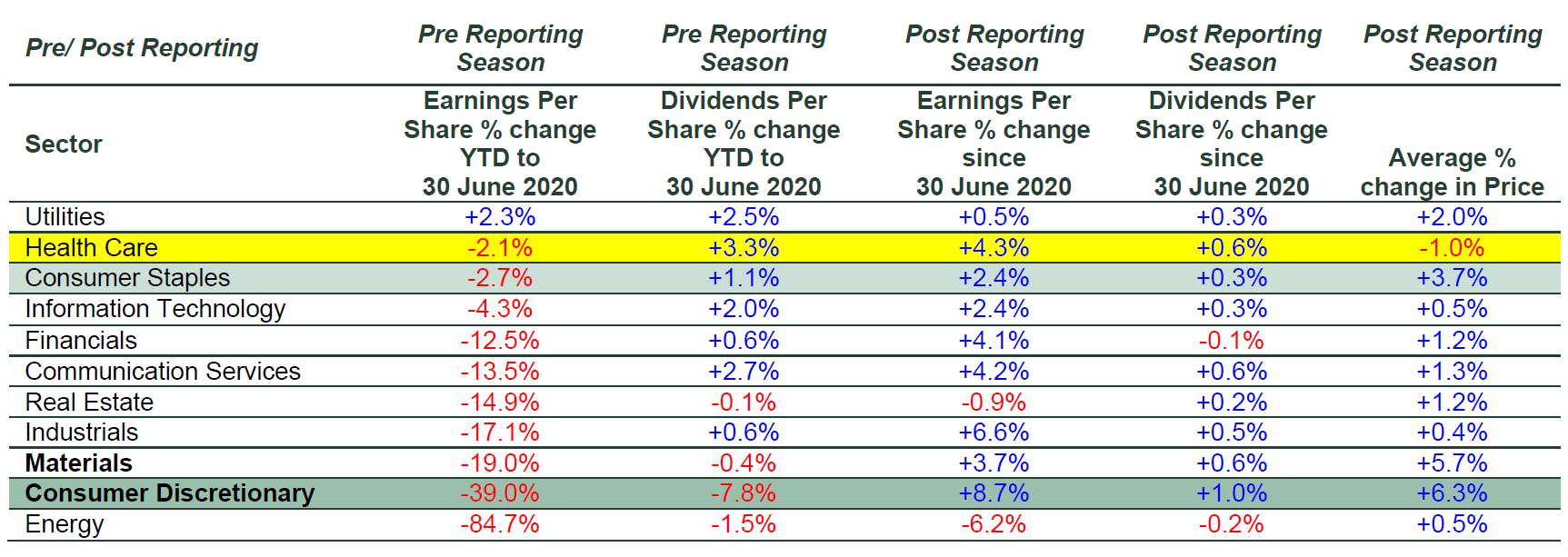

The earnings and dividend trends had been well established coming into the start of the US earnings season. The defensive sectors held up better than the cyclical sectors in terms of earnings and dividends. Reflecting the changes in earnings and dividends we observed payout ratios lift from 32% at the end of 2019 to 47% by 30 June 2020. Fortunately the mostly negative earnings trends prior to earnings season did not deteriorate further as companies updated the market in July and August.

In almost all sectors, earnings forecasts were revised slightly higher post reporting. Whilst this is encouraging it is important to remember the trend year to date remains decidedly negative for the majority of S&P 500 Index companies. Looking at the percentage change in company share prices from the day prior to the results, to three days after the result, we can make a number of observations about how the market reacted to the company updates. The Discretionary and Materials sectors performed the best followed closely by Staples. Health care was probably the most interesting underperforming despite seeing reasonable improvements in future earnings and dividends. Will we see similar trends in Australia?

Figure 2. US Reporting Season Summary

Early Earnings Trends from the Australian Reporting Season

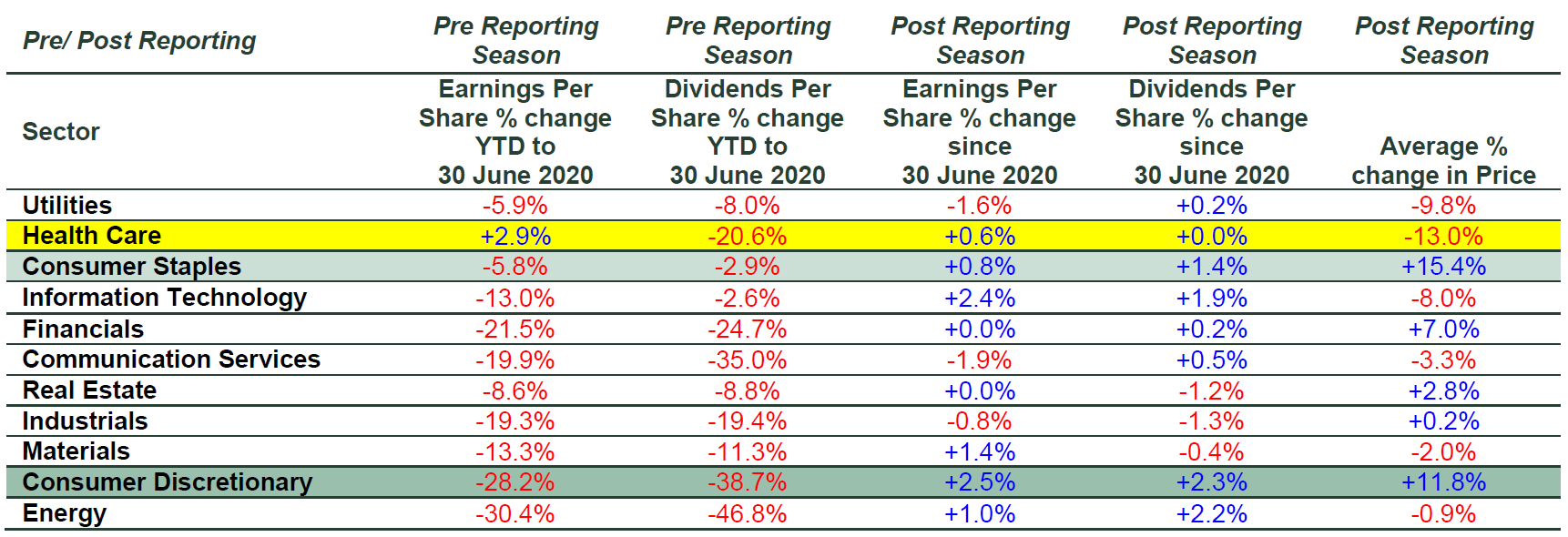

The earnings trends in Australia have shown many similarities to those in the US both leading up to 30 June and since the reporting season has started in Australia.

Across most sectors the negative earnings trends have stabilised.

As in the US, the year to date earnings and dividend trends are still negative for most Australian corporates. In Australia, Healthcare companies have disappointed post earnings and the Consumer companies (both Staples and Discretionary) have surprisingly the greatest change in price post earnings. Interestingly the technology sector has seen some profit-taking post reporting so far this season.

Where the results between the US and Australia are differing the most is on dividend expectations. Australia has seen significant downgrades to dividends compared to the US. Of course most Australian companies are typically much higher dividend payers than those in the US. At the end of 2019 the average payout ratios across the S&P/ASX 300 Index was 59%, compared to the US at 32%, and by 30 June this had moved higher to 65%. The Banks have attracted much attention with respect to dividend cuts but as Figure 3 illustrates, it has been broad based across many Australian companies. Based on recent changes in expectations the negative trends for dividends have so far stabilised for Australian sectors except for Real Estate, Industrials and Materials.

Figure 3. Australian reporting season results so far

The Bottom Line

The Australian earnings season is still at an early stage but it does appear that many of the US trends are being echoed in Australia. The pandemic has increased the correlation of global themes. Earnings expectations do appear to be stabilising for now. As the earnings season continues to unfold, we continue to assess the relative merit of our positions and adjust our portfolios accordingly, always looking for the highest quality companies offering reasonable value with improving growth prospects and acceptable levels of volatility. We remain uninvested in the Australian technology sector as it continues to look unattractive from a risk and return perspective.

The above wire is an extract from our latest monthly report which can be accessed here (including sources).

Learn more

Stay up to date with our latest thoughts by clicking follow below and you'll be notified every time we post content on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

........

Issued by State Street Global Advisors, Australia Services Limited (AFSL Number 274900, ABN 16 108 671 441) (“SSGA, ASL”). Registered office: Level 14, 420 George Street, Sydney, NSW 2000, Australia · Telephone: +612 9240-7600 · Web: www.ssga.com. State Street Global Advisors, Australia, Limited (AFSL Number 238276, ABN 42 003 914 225) (“SSGA Australia”) is the Investment Manager. Investors should read and consider the relevant Product Disclosure Statement (PDS) for a Fund carefully before making an investment decision. A copy of SSGA’s Managed Fund PDSs are available at www.ssga.com.au This general information has been prepared without taking into account your individual objectives, financial situation or needs and you should consider whether it is appropriate for you. You should seek professional advice and consider the product disclosure document, available at ssga.com, before deciding whether to acquire or continue to hold units in the Funds. The views expressed in this material are the views of the SSGA Australian Active Quantitative Equity Team through the period ended 8 April 2020 and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Volatility management techniques may result in periods of loss and underperformance, may limit the Fund's ability to participate in rising markets and may increase transaction costs. Actively managed funds do not seek to replicate the performance of a specified index The fund is actively managed and may underperform its benchmarks. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. Investing in the Fund involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment. Standard & Poor’s and S&P are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and have been licensed for use by S&P Dow Jones Indices LLC and sublicensed by SSGA. The S&P/ASX 300 Index is a product of S&P Dow Jones Indices LLC, and has been licensed by SSGA. SSGA’s Funds are not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC, Dow Jones, S&P, their respective affiliates, and none of S&P Dow Jones Indices LLC, Dow Jones, S&P, nor their respective affiliates make any representation regarding the advisability of investing in such product(s). Investing involves risk including the risk of loss of principal. Risk associated with equity investing includes stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. This material should not be considered a solicitation to apply for interests in the Funds and investors should obtain independent financial and other professional advice before making investment decisions. There is no representation or warranty as to the currency or accuracy of, nor liability for, decisions based on such information. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA Australia’s express written consent.

1 topic

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment