Entering reporting season with caution

Elevated earnings expectations this reporting season, and an ever-increasing amount of capital engaged in momentum-style investment strategies (i.e. those that seek to aggressively own businesses in earnings upgrade or upward price momentum cycles) undoubtedly sets the stage for some likely disappointments.

Indeed, the continued strong performance of a number of businesses across the small-cap growth spectrum has led some to conclude that the outperformance of higher-quality, higher-growth businesses has reached its peak and market leadership across the small-cap space will likely rotate to lower-quality, value-type companies from here.

ASX Small Ordinaries ‘Growth’ Performance Relative to ‘Value’

If share price performances through July are any indication, the market has begun to position for this somewhat, with smaller-cap “growth” businesses seemingly underperforming the value end of the market this month for the first occasion since the beginning of the year (albeit the bulk of this underperformance likely came in response to the significant price declines experienced by a number of the high-growth US-listed technology names that were aggressively sold off this month after failing to meet lofty market estimates – see Facebook, Netflix, Twitter et al).

While we certainly share the concerns of the market that valuations (and/or market expectations) for certain companies and sectors within the smaller cap space have become increasingly stretched, we would caution against implementing a wholesale rotation within portfolios toward cheaper, lower-quality businesses at the current stage of the cycle, primarily for two key reasons:

1) Remember it’s often not earnings that miss estimates, but estimates that miss earnings.

High-quality businesses often fall victims to their own success – elevated growth numbers, high operating margins and new product or territory rollouts understandably create excitement and invariably market expectations grow overly optimistic about the prospect for a company’s near-term earnings as a result.

This is a natural part of later-cycle market activity, although it often creates the detrimental effect of creating exceptionally high earnings hurdles for a company management team to deliver (and equally significant near-term earnings risks for investors within the company). The end result is often manifested in a business delivering strong overall results in an absolute sense (be it versus their competitor set or their own historical financial results), but succumbing to significant share price declines in the short term as the results are deemed a ‘miss’ versus consensus analyst estimates.

In such cases, there is rarely anything wrong with the underlying business itself, other than underlying expectations becoming too elevated resulting in short-term/ momentum-style capital promptly exiting the register following the earnings ‘disappointment’. While certainly not a pleasant experience in the short term for holders, it is hard to argue that such events are synonymous with the ‘end of the growth cycle’ but are rather a necessary adjustment in some cases to overly elevated expectations.

Ultimately, we continue to believe that in a low-growth environment, it will be the businesses that can generate meaningful earnings growth regardless of the underlying cycle that will continue to provide meaningful shareholder returns over the long term. While we have taken the decision in recent months to lighten positions in some higher-growth businesses where we feel the risk of missing elevated market expectations is high:

We’re ultimately hopeful that any resultant share price sell-off may provide compelling opportunities to redeploy this capital back into these companies at a time when valuations rebase and the risk/reward equation is more favourably tilted in our favour

2) Traditional value stocks are not currently that cheap

Historically speaking, the best time to aggressively own a large amount of beaten-up, low quality and cyclical-style businesses is generally at the absolute bottom of an economic cycle, when valuations are excessively low (on both relative and absolute measures), balance sheets are impaired and any improvement in underlying fundamentals has the ability to significantly re-rate valuations from their depressed state.

It has long been our belief that it is difficult to generate consistent long-term returns through an economic cycle by continually investing in low-quality businesses. Granted, there are opportunities through the cycle where the downside risk of owning lower-quality companies is negated by the sizeable returns on offer, however, it is difficult to see how this opportunity currently exists on a wholesale level across Australian industrial small caps.

Rather than finding ourselves at the beginning of a cyclical recovery, equity markets in Australia instead sit at 10-year highs, the global economic growth recovery is now maturing and balance sheets, as a whole, are in good condition. In our own minds, the economic requirements needed to drive a valuation re-rate in lower-quality and cyclical businesses ultimately looks hard to identify at this point.

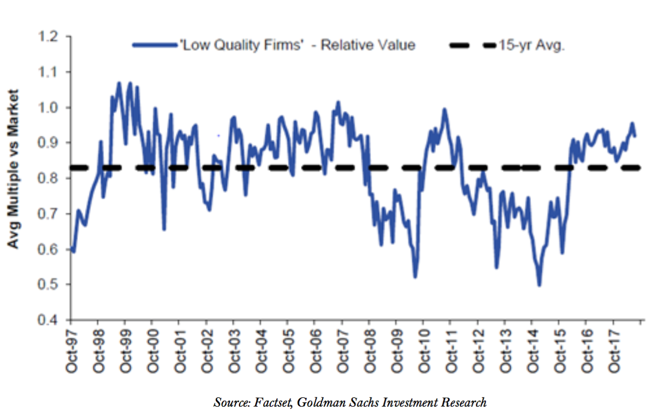

Perhaps a greater headwind to a re-rate of earnings multiples across the value end of the market is the fact that cyclical and lower-quality businesses also don’t currently present as being overly cheap. Businesses identified as ‘Low Quality’ (as measured by 12-month forward PE, EV/EBITDA and Price/Book metrics) currently trade at a premium to their 15-year historical averages and towards the top end of their average valuation trading range.

Discount to the Market of ‘Low Quality’ Stocks

Ultimately, investors always have a natural affinity toward deploying capital into companies with lower relative valuations (particularly when considering the significant premiums at which higher-growth businesses currently trade), however one needs to be careful to avoid the classic ‘value-trap’ scenario: most often occurring when capital is deployed into mediocre businesses based solely on appealing relative valuations rather than an identified catalyst for an increase in future earnings growth or valuation multiple.

Cheap shares can stay cheap for a long time, and the opportunity cost of having capital tied up in a lower-quality business (which, by their nature, have an elevated tendency to deliver any number of value-destructive outcomes) can provide a significant drag on overall portfolio earnings.

This presents a conundrum that the vast bulk of Australian equity market participants are currently attempting to solve – high-quality businesses trading at stretched multiples, whilst lower-quality businesses don’t immediately screen as being overly attractive either. Our own response (as regular readers of these letters will be aware) has been to selectively reduce or exit positions in companies where we feel valuations are stretched, earnings risk is elevated and near-term catalysts for a further re-rating are hard to identify. In some cases, we have been happy to rotate this capital into businesses that trade closer to average market multiples and where we remain highly confident in their ability to deliver on earnings.

In the absence of conviction that the current cycle presents a compelling opportunity to add a material amount of cheaper, lower-quality businesses into the portfolios, for now we are just as happy to retain any proceeds from realised investments in cash until a suitable opportunity presents itself. With reporting season starting shortly and expectations high, we are certainly looking forward to exploiting any potential opportunities that may present themselves through the period and we look forward to providing an update on this front next month.

This is an excerpt from the July 2018 Ophir letter to Investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment