Evaluating oil & gas lease acreage in the United States (Approved community submission)

As a politically stable and developed nation with mature infrastructure, large pipeline networks and rail transport in place for the transportation of oil and gas, the United States provides one of the most attractive environments for oil and gas companies in the world. The US oil and gas scene is a particularly favourable environment for small operators, thanks to a peculiar system of property rights in the USA. 1 (See "Federal, State and Fee Leases" section below) Given this, it is unsurprising to find that a number of listed Australian energy companies have gravitated towards the onshore oil and gas fields of the US.

Patrick Fresne

Goldandrevolution.com

The depressed energy prices over the past couple of years have adversely impacted sentiment towards the oil and gas sector, and Australian oil and gas companies operating in the US have not been immune. The share prices of most of these companies are currently sitting near multi-year lows.

In recent months, however, there have been some indications which suggest that mood towards this sector is improving.

Two Australian energy companies based in the US -American Patriot Oil & Gas (AOW) and Sundance Energy (SEA) - have become takeover targets this year.

It is also worth noting the July debut of Australis Oil and Gas (ATS) onto the ASX, the first new Australian company to enter the North American oil space in two years.

Now could be the time to pay closer attention to energy companies focused on this region.

Below I examine several Australian stocks operating in the United States, with the focus primarily on the undeveloped lease acreage controlled by these companies, as the value of this acreage may not be fully reflected in the share price of these stocks.

There is also some reason to believe that large lease acreage positions may become increasingly difficult to acquire in the US, for reasons to do with the current political environment.

Federal, State and Fee Leases

In the United States, ownership of mineral rights can be held by private individuals or State and Federal governments. Oil and gas companies identify the owners of the minerals and negotiate a lease to allow the companies the right to explore for oil and gas.

The most significant owner in the US is the Bureau of Land Management (‘BLM’), which manages almost 700 million acres of sub-surface mineral estate, more than any other government agency.

Lease auctions are periodically held by the BLM on un-leased ground, with the successful bidder entitled to extract mineral resources over the time frame of the lease (ten years for Federal lands, although if a company has a well capable of producing on the lease at the time of expiry it is said to be ‘Held by Production’ and does not expire until the well is no longer producing.)

In addition to Federal leases, there are also State Leases and Fee Leases (privately owned). With Fee Leases, the company negotiates directly with the individual landholder, and as such Fee Leases generally have fewer environmental restrictions than Federal or State Leases.

Fee Leases predominate in the Eagle Ford and the Permian Basin of Texas, whereas most of Niobrara and the Bakken are covered by State and Federal leases.

Keep it in the ground? Politics and Shale Oil

By law, all public lands in the United States available for oil and gas leasing must first be offered in a competitive lease auction, with the successful bidders gaining the right to explore and exploit the oil and gas deposits that they find over the term of the lease. 2

Over recent years, political forces have served to increasingly restrict the release of land available for oil and gas exploration and extraction, a trend largely driven by rising environmental awareness.

Across the US, concerns are widespread about the impact on the environment of the hydraulic fracturing techniques (‘fracking’) employed by many shale or tight oil companies, centred particularly on the potential impact of these techniques on groundwater. The controversial technique has also been blamed on an increase in seismic activity in parts of the US in recent years, such as the recent powerful earthquake in Oklahoma. 3

Unsurprisingly, the fracking issue regularly dominates local politics and media in the United States. The subject has come up in the current US election campaign. Donald Trump has broken with many state Republicans and the oil industry, suggesting during a recent interview that local communities that are against fracking should have a say in the matter.

Hillary Clinton has also argued in favour of tighter regulations on hydraulic fracturing, a position which in many respects simply reflects a continuation of the stance of the current US administration. 4

Over the past two years, the Obama administration has been holding back drilling on Federal land, seemingly by tangling the process in red tape. The Bureau of Land Management has cancelled 34 out of 64 lease auctions since 2014. 5

The table below shows the number of acres offered at lease sale auctions and the number of acres sold by the BLM from 2012 to 2015.

[IMG5.PNG]

Above: The total acreage on offer by the BLM has fallen sharply in recent years, from over 6 million acres to just over 2 million in 2015 6

Around 11% of the gas and 5% of the oil produced in the United States is from Federal onshore oil and gas wells 7, so the recent drop in lease acreage release by the BLM is likely to put a dent in future oil and gas production in the United States.

The tardy release of acreage by the BLM for oil exploitation in recent years reflects the pro-renewable energy stance of the US Democratic Party. Low energy prices have served to hinder the shift away from fossil fuels (for example, sales of plug-in electric vehicle flat lined in the US after the oil price crash 8) and so paradoxically, in the short term higher oil prices are as much in the interest of the US Democrats as it is for smaller US oil companies.

In practice, the relationship between the Democrats and the US oil industry is an ambiguous one: President Obama has presided over the largest increase in oil production in US history9, which has reduced the dependence of the US on foreign oil and helped boost the US economy after the GFC. Given the importance of the local oil and gas industry, it would appear that Obama and Clinton have adopted a ‘grandfathering’ approach to fracking, limiting the spread of the technique into new areas rather than enacting broad-brush restrictions.

Thus, in the short to medium term, the controversy over fracking may actually be a positive for companies currently holding oil and gas lease acreage in the US.

The restriction on the land releases by the BLM may help pave the way for a ‘choke’ in future oil supply in the United States, and so it is plausible that companies controlling oil lease acreage may find that they are sitting on an increasingly scarce and valuable asset in the event of a sustained oil price recovery.

Australian companies holding US oil & gas lease acreage

The table below shows the size of the lease position of US focused ASX listed Australian oil and gas companies, as well the approximate Australian dollar-per-acre value of the lease holdings for each stock.

Each dollar-per-acre figure has been determined by calculating the enterprise value of the company divided by the total number of acres held by the company, using the figures from the most recent financial reports (the dollar-acre values have been rounded to the nearest $5).

[IMG2.PNG]

The table above is not comprehensive: two companies not included here are Red Sky Energy (ROG) and Black Star Petroleum (BSP) due to the extreme illiquidity of these two companies.

One thing that stands out in this table is the significant divergence between the per-acre valuations of the companies focused on Niobrara or the Bakken and those controlling acreage in the Eagle Ford in Texas or Oklahoma.

There are a few reasons that could explain the disparity: one factor is that the northern oil regions at Niobrara and the Bakken are more distant from the important oil hub at Cushing in Oklahoma, resulting in higher transportation costs and thereby adding several dollars more to the cost of production of each barrel of oil. 10

Given the current low oil price environment, that fistful of dollars saved in per barrel production costs by the operators in Texas and Oklahoma could make all the difference, and it would appear that investors are willing to pay a premium for the companies in the low-cost areas.

The value of lease acreage in the US can thus vary widely, depending on the location, the lease type, and how well developed the land is, to name a few variables.

In some cases, companies will helpfully make these details available to prospective and current investors: AusTex Oil and Gas (AOK), for example, provided some detail on the value of their oil land in Kay County, northern Oklahoma in their June quarterly activities report:

‘Leasing in the area now occurs at $100-$150 per acre versus 2014 levels of $300 to $350.’ 11

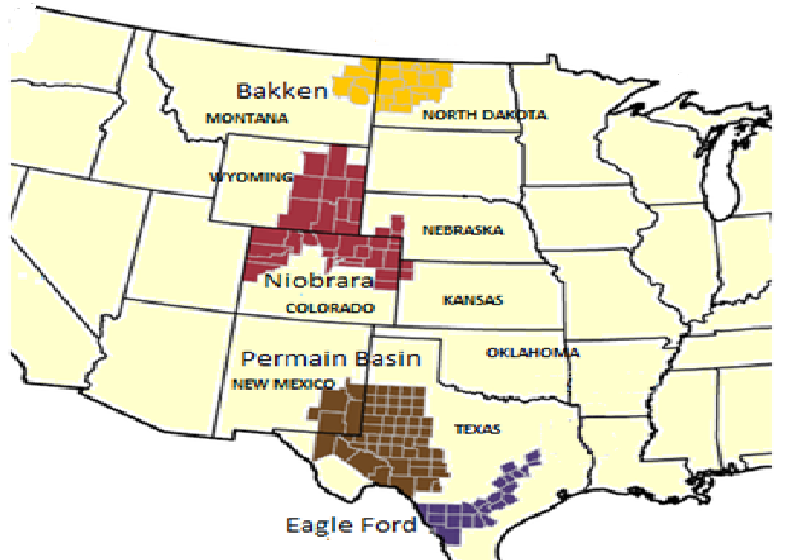

Above: US oil and gas regions mentioned in this article.

For purposes of comparison, I’ve included below the most recent available data on lease valuations from the BLM website (up to September 2015). In the table below, I’ve calculated the US dollar per acre paid for each transaction in each location (rounded to the nearest dollar). There is a wide range here, from as low as $4 per acre to $2843 per acre. The average is $498 per acre, although given the wide range the average figure would only be relatable to a company with acreage spread across various locations such as American Patriot.

[IMG4.PNG] 12

It is a reasonable supposition that the acreage held by the listed Australian companies would typically be worth more than the dollar-per-acre bids at a BLM auction, as Australian companies in the US would only be targeting the most promising locations.

The recent takeover bid for American Patriot by Running Foxes Petroleum supports this assumption. The offer was for 22c per share, which would put the AUD dollar value of the company acreage at around $1100, or just above $800 USD at the current exchange rate.

In the recent AUD, $0.185 per share offer for Sundance Energy the bidder was also willing to pay substantially more for the lease position of this company than is currently priced into the stock. 13

Both of these takeover offers suggest that the current share price of most of the US focused oil and gas stocks may not be accurately reflecting the true market value of their leasehold acreage positions.

On the hunt: Australis and American Patriot

One of the greatest success stories of the Australian oil and gas operators in the US was Aurora Oil & Gas. The entry and eventual takeover of this company by Canada’s Baytex Energy seemed perfectly timed to coincide with the boom years for oil (2005-2014). The Baytex takeover offer valued the Aurora lease position at over $100,000 an acre. 14

Given this, it is intriguing to note that some of the executives behind Aurora have now gotten behind a new project, Australis Oil and Gas, which listed in late July.

Considering how underappreciated the US focused oil and gas stocks appear to be at present, it is not particularly surprising to learn from the company Prospectus that Australis has an aggressive strategy, aiming to:

...provide shareholders value and growth opportunities through the acquisition and accumulation of quality onshore assets within emerging and established unconventional fields in the United States of America and other jurisdictions... 15

Australis is not the only company on the prowl: American Patriot, after knocking back the Running Foxes takeover bid, has decided instead to enter into a joint venture with the Foxes, the aim being to acquire undervalued oil & gas assets. 16

Alexis Clark, the MD of American Patriot, was formerly an oil and gas research analyst, and so would be well acquainted with the assets of the Australian companies operating in the US. It would thus not be unreasonable to consider that some of the local Australian oil and gas stocks based in the US could become targets.

Note: this is a general overview of the subject examined above rather than an in-depth financial analysis, and so as always, do your own investigation into these stocks before committing to any course of action.

Disclosure: the author owns shares in Entek Energy

Sources

1) American Patriot Oil & Gas Prospectus, pg 19, 08/7/14

2) Bureau of Land Management website: (VIEW LINK)

3) Live Science: ‘Man-made earthquake hotspot revealed: Oklahoma’, 28/3/16: (VIEW LINK)

4) The New York Times, ‘Colorado activists submit petitions,' 8/8/2016: (VIEW LINK)

5) The Washington Times, ‘Obama’s bureaucratic tar pit,' 11/8/2016: (VIEW LINK)

6) Bureau of Land Management website: (VIEW LINK)

7) Bureau of Land Management website: (VIEW LINK)

8) Bloomberg, ‘Plug-in electric autos left behind in record US year,' 7/1/2016: (VIEW LINK)

9) CNN Money, ‘America’s biggest oil boom came under Obama’ 21/7/2016: (VIEW LINK)

10) AusTex presentation, pg 5, 31/5/16

11) AusTex quarterly activities report, pg 5, 29/4/16

12) Bureau of Land Management website

13) Canaccord Genuity research update, 19/7/16 ‘Sundance Energy is in play.'

14) American Patriot Oil & Gas, investor presentation, 21/7/14.

15) Australis Oil and Gas Prospectus, pg 9, 21/7/16.

16) American Patriot Oil & Gas announcement, pg 1, 29/7/16.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

1 topic

3 stocks mentioned

Patrick Fresne

Researcher

Goldandrevolution.com

Expertise

No areas of expertise

Patrick Fresne

Researcher

Goldandrevolution.com

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment