Extreme caution warranted for markets ‘high flyers’

Over the last three months, stock markets have continued to rally strongly as economic activity started to recover from the depths of the COVID-induced recession. As a result of the lockdowns that have been put in place to control the spread of the virus, there have been significant changes in spending and working patterns across economies.

These changes, together with rapid and large increases in money supply, have unleashed a speculative mania in ‘high growth' companies and other beneficiaries of the changing environment, while the balance of the market remains mired in a traditional bear market. We believe extreme caution is warranted in regards to the market's current 'high flyers', while opportunities abound elsewhere.

Not all changes in spending patterns will be sustained.

Many changes in our patterns of behaviour make entire sense given the circumstances. Faced with being either unable or not wanting to leave the house to shop, many consumers have taken to ordering groceries online for the first time. In many locations there is evidence of new adopters continuing to use such services, even as restrictions have eased. There are numerous examples that fit into this category, including video streaming services, such as Netflix or video conferencing products, such as Zoom.

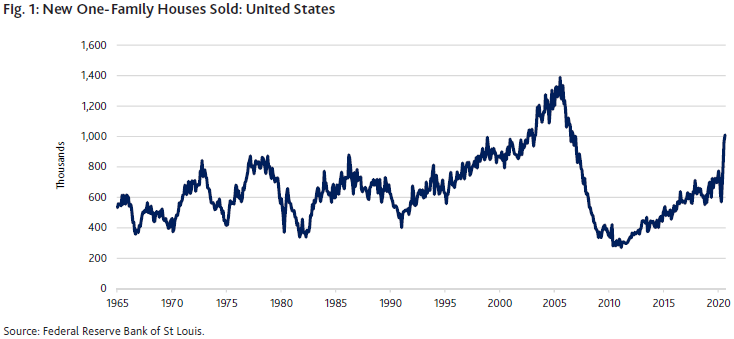

Other changes have perhaps been somewhat more surprising. For example, in the US, we have seen extraordinarily strong new home sales (see Fig. 1). In one sense, the lift in home sales is understandable, as people opt for a different location and type of residence in an era of more flexible working arrangements, particularly the ability to work from home. The cost of financing major purchases, such as homes and cars, has fallen with lower interest rates. However, for households to be taking on such major financial commitments in the midst of a deep recession and extraordinary uncertainty is concerning.

What is often overlooked when observing these changing spending patterns is that they have been funded by the collapse in spending elsewhere, such as travel and restaurants. In a post-COVID environment, when people can once again spend money on such activities, the boost in spending in other areas will likely wane. For some areas, where activity has simply transferred from offline to online, such as grocery shopping, this may hold up, but even here, growth rates are likely to fade, as these businesses will have moved closer to maturity.

One area of changed spending that will likely persist for some time, is government spending. However, the emphasis of government spending will likely shift from shorter-term support measures, such as the JobKeeper Payment scheme in Australia, to longer-term projects, such as infrastructure and incentives for investment. Environmental initiatives to reduce the use of fossil fuels and plastics for instance, are likely to be an ongoing part of government spending in much of the world.

Changes in spending patterns have often reinforced investors’ views of different sectors held prior to the pandemic.

Businesses that have benefited from changes in consumer behaviour were in many cases ones that were already growing quickly. Examples include most forms of e-commerce from online shopping to food delivery services, online computer games, and video streaming services. Other favoured investments prior to the pandemic included defensive investments, such as consumer staples, that have seen sales grow not only from stocking up pantries as the lockdowns came into effect, but from greater consumption as people spent more time at home. On the other side, more cyclical businesses that were already struggling as a result of the US-China trade war and low growth, such as commodity producers, have suffered even further due to the collapse in economic activity.

Over the last two years, we have discussed on numerous occasions how investors, faced with low interest rates, have sought better returns from asset classes that they might otherwise have avoided, such as equities. As this has come at a time when there was already great uncertainty, such as rising geopolitical tensions and with many traditional businesses disrupted by e-commerce and other technology, investors have shown a strong preference for perceived ‘low-risk’ businesses. Predominantly, these were in high- growth areas (i.e. e-commerce, payment systems and software as a service), as well as defensive businesses (i.e. consumer staples, real estate, utilities and infrastructure). At the same time, investors were avoiding businesses with any degree of uncertainty or cyclicality.

While some businesses (e.g. those in the travel-related sector including infrastructure such as airports, real estate such as CBD offices and shopping malls) have changed sides from being in the loved ‘high growth and certainty’ grouping to the neglected ‘cyclical and uncertainty’ grouping, by and large the economic impacts of the pandemic have reinforced investors’ pre-existing views and preferences.

This is a particularly dangerous environment for investors as our cognitive biases come to the fore.

It is well documented that our cognitive biases(1) play a major role in our decision making, and when it comes to investing we are deeply exposed to the role these biases play. Our short summary is that investors tend to over-emphasise and over-extrapolate the short-term trends and events - both the good and the bad.

This makes the current moment in time particularly worrisome. Prior to the pandemic, investors already held enthusiastic views of the prospects of many of the fast-growing companies. These views have now been reinforced even further by the additional boost to revenues they have received. As share prices move rapidly higher, this further reinforces the idea that these companies make great investments.

Ultimately, the value of a business is determined by the entirety of its future profits, for 10 years and beyond. The question is whether the boost to the short-term picture justifies the significant share price rises that have occurred? In some cases, it may well do. We have seen some companies that were expected to be lossmaking for a number of years turn profitable far sooner. However, there is plenty of complexity in assessing the prospects of fast-growing companies, especially when one must make assessments of revenues and profits into the distant future.

The role of excess money creation provides an alternate story for why share prices of growth stocks are running hard.

While there is much discussion around the potential of the ‘new economy’ at the moment, the other factor at play in the rebound in markets is the rapid growth in money supply. As we discussed in our last quarterly update,(2) this increase in money circulating in the economy reflects the way governments have funded their monetary and fiscal policy initiatives. When the growth in money supply exceeds economic output, it will necessarily result in inflation. Although inflation has not yet appeared in goods and services (or the consumer price index), it has appeared in asset prices, such as bonds and some parts of the stock market. Is it the bright prospects of the growth stocks that have driven markets or the inflationary effects of the printing presses?

We would answer this question by looking at valuations. What we see across many of the much-loved stocks of the moment are valuations that are hard to justify no matter how bright their prospects are. As one example, the market value of Tesla today is around US$400 billion and the company is expected to sell in the order of 480,000 vehicles this year. This compares with Toyota, which is valued at just under US$200 billion and will likely sell around 9.5 million vehicles i.e. around 20 times more than Tesla.(3)

Of course, this simple comparison doesn’t do justice to Tesla’s achievements in leading the electric vehicle revolution and the developments they are driving in battery technology. Still it could be argued that Toyota, having launched the first hybrid electric vehicle, the Prius, in 1997, knows a thing or two about making and selling electric cars. The prospects for Tesla are most certainly bright in our view and ultimately, they may achieve enough to justify this lofty valuation. However, the company must still jump a huge hurdle just to meet current market expectations.

The run-up in the market is not just about the valuations of one or two hot stocks that are inconsequential in size. There are many stocks, and in aggregate the market capitalisations of these high flyers readily run into hundreds of billions, even trillions of dollars. This phenomenon is of course well understood and splashed across the front pages of the financial press, and yet it continues. Perhaps equally disturbing, is that the safe and comfortable option to invest in growth has been in companies such as Microsoft, Facebook, Alphabet and Apple. These are fine companies with good prospects (ignoring any anti-trust concerns), however, they have steadily revalued over time and now trade at generous valuations, though nowhere near as challenging as Tesla.

This brings us back to the question of money printing. If it is the inflationary effects of money printing that has driven stocks to these lofty levels, then it probably needs to continue to keep the market rally going. At the time of writing, additional stimulus measures are being debated in the US. Whether there is an agreement before the 3 November US election or not, it is probably a reasonable assumption that over the course of the next 18 months, governments around the world will continue to increase their spending, and it will probably be funded by borrowing from the banking system. However, as economies start growing again, the excess of money creation over economic output will most likely reduce.

The risk for investors in equity markets today is the highly valued growth stocks. The opportunity is in companies that will benefit as we move into the post-COVID environment.

There is much discussion about a new world for investing, or a new paradigm if you will, marked by interest rates at or around zero for the foreseeable future and the never-ending march of new technology continually changing the business landscape. This new environment renders all the old rules of investing null and void. Perhaps? Or is this just another version of the four most expensive words in investing: This time is different? Alternatively, it may just be a good old-fashioned bull market, driven by a great story and excess money supply, reinforced by our cognitive biases that lead us to emphasise recent events and trends.

There are plenty of warning signs to suggest what we have here is simply a speculative mania:

- A buoyant market for new listings with companies often debuting on the market at prices as high as 50% or more above their issue price.

- High levels of retail investor activity, not just in shares but also in the options market.

- The stories of fortunes made and lost overnight by small investors that are regularly shared on internet blogs and even in the traditional financial press.

- And every good bull market needs an innovative financing vehicle and this time we have Special Purpose Acquisition Companies (SPACs). The premise here is that investors invest their cash in a SPAC and the promoters will find a great company to buy from the private markets with the funds. For those who have been around long enough, it sounds very similar to the 'cash box' listings in the bull market of the 1980s, and most of these didn’t end well for investors.

What brings it to an end and when that happens are the great unanswerable questions, as has been the case in past speculative markets. One thing we do know though, is that manias tend to end suddenly and abruptly. The significant bull markets of the last 40 years have come to an end when monetary conditions tightened. Typically, this has been marked by rising interest rates, which for the moment seems inconceivable. Perhaps a slowing of money creation at a time when economic activity is rising will represent the tightening in liquidity, even if interest rates do not budge significantly. Perhaps it will simply be when we are clear of the lockdowns and restrictions and the level of permanent business closures and job losses is much greater than thought and prospects for listed companies are much bleaker than expected.

Despite these unusual times, it is important to remain committed to our long-standing and consistent investment approach. We will focus on companies that others prefer to avoid, assess their potential over the medium term, and buy where their stock price implies an attractive return.

Never miss an update

In a world awash with news and information, true insights remain hard to come by. Stay up to date with all of my latest content by hitting the follow button below.

Footnotes

(1) Cognitive biases are the systematic ways in which we frame and process information, which can lead to irrational judgements and decision making. For a comprehensive read on the topic, please see Daniel Kahneman’s Thinking Fast and Slow. Or for a much briefer overview, see our publication Curious Investor Behaviour as well as various other articles and materials at: (VIEW LINK).

(2) (VIEW LINK)

(3) Source: FactSet Research Systems, company reports, Platinum Investment Management Limited.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew joined Platinum as a founding member in 1994 in the capacity of director and Deputy Chief Investment Officer. Previously he was a Vice President of Bankers Trust Australia covering Asian equities and managing the BT Select Market Trust - Pacific Basin Fund.

In May 2013 Andrew was appointed Chief Investment Officer (CIO). Andrew was the portfolio manager for the Platinum Asia Fund until December 2014 and is co-manager of the Platinum International Fund. In July 2018 Andrew was appointed CEO (General Manager) of the Platinum Group. Andrew assumes this role in addition to his CIO role and portfolio management responsibility for the flagship fund, the Platinum International Fund and other global equity funds and mandates.

........

This article has been prepared by Platinum Investment Management Limited ABN 25 063 565 006, AFSL 221935, trading as Platinum Asset Management (“Platinum”). This information is general in nature and does not take into account your specific needs or circumstances. You should consider your own financial position, objectives and requirements and seek professional financial advice before making any financial decisions. The commentary reflects Platinum’s views and beliefs at the time of preparation, which are subject to change without notice. No representations or warranties are made by Platinum as to their accuracy or reliability. To the extent permitted by law, no liability is accepted by Platinum for any loss or damage as a result of any reliance on this information.

Andrew joined Platinum as a founding member in 1994 in the capacity of director and Deputy Chief Investment Officer. Previously he was a Vice President of Bankers Trust Australia covering Asian equities and managing the BT Select Market Trust -...

Expertise

Andrew joined Platinum as a founding member in 1994 in the capacity of director and Deputy Chief Investment Officer. Previously he was a Vice President of Bankers Trust Australia covering Asian equities and managing the BT Select Market Trust -...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Commodities

Central banks are doubling down on gold - should you?

Livewire Markets