Extreme valuations aren’t the only sign of exuberance

Central Banks and Government stimulus rescued investors in 2020 and the COVID-19 vaccine progress provided a powerful boost in Q4 2020. The democratic control of the US senate kept the party going as we finished 2020. As shown in Figure 1 below, most asset classes had strong performance in 2020. In this monthly note we take a closer look at what is priced and the biggest risks and opportunities in 2021.

Figure 1. Most asset classes generated strong returns in 2020

Source: Thomson Reuters, State Street Global Advisors as of 31 December 2020. Past performance is not a reliable indicator of future performance. This information should not be considered a recommendation to invest in a particular sector or to buy or sell any security shown. It is not known whether the sectors or securities shown will be profitable in the future.

While broad equity markets are expensive, some parts are particularly expensive, while others offer value.

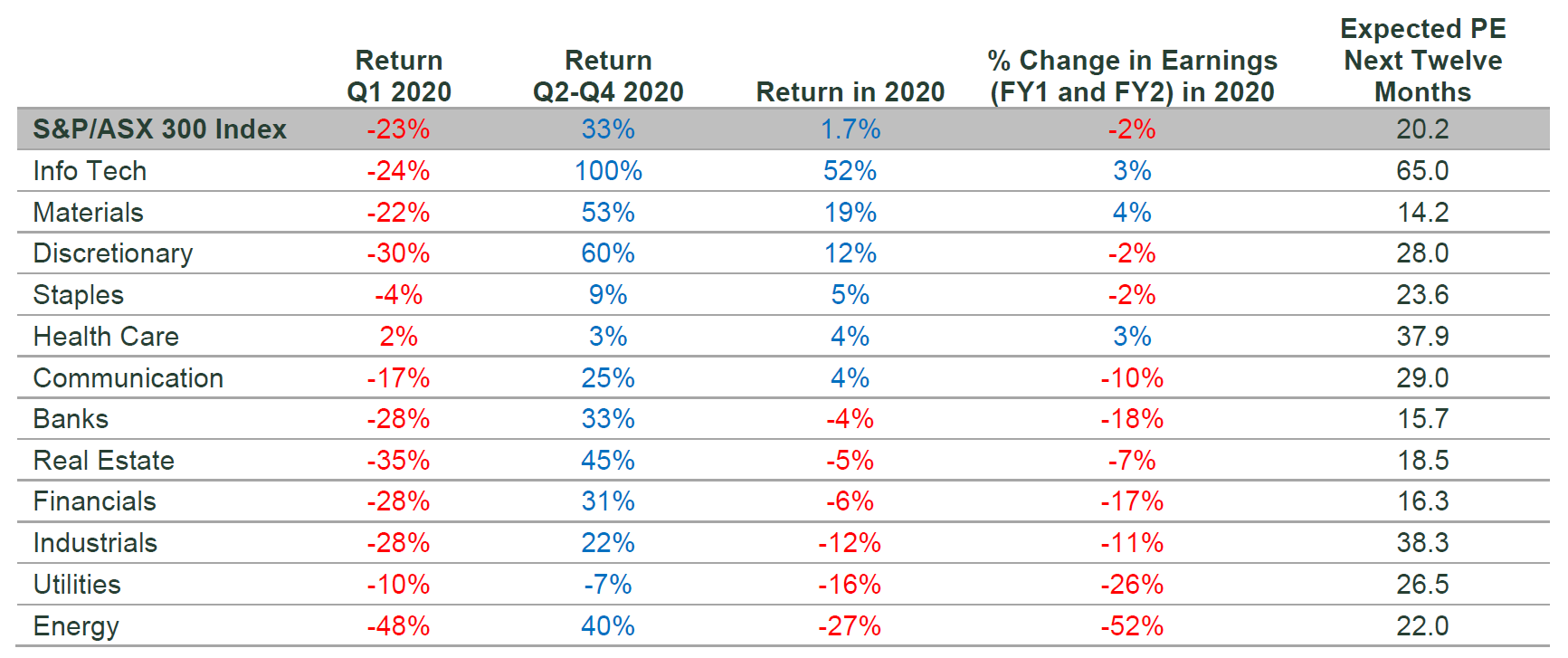

Compared to history, global equity markets are trading at expensive multiples. The massive economic stimulus, the super accommodative central bank policy settings and the potential for a return to normal, thanks to the vaccines, accounts for these lofty multiples. Figure 2 below highlights the expensive valuations we can observe in the S&P/ASX 300 Index and across the S&P/ASX 300 sectors. The market is expensive as a whole but some companies are extremely expensive while others have been neglected and offer compelling value.

The companies that offer the greatest risk for investors in 2021 are somewhat ironically many of the same companies that have provided the greatest return to investors in 2020.

The greatest risk is associated with those companies now priced for perfection in terms of growth, low interest rates, and a world in which investors had very few other growth investment opportunities.

Figure 2. Returns, changes in earnings per share (EPS) expectations and price earnings (PE) valuations at the end of the 2020

Source: Thomson Reuters, State Street Global Advisors as of 31 December 2020. Universe is the S&P/ASX 300 Index. Past performance is not a reliable indicator of future performance. This information should not be considered a recommendation to invest in a particular sector or to buy or sell any security shown. It is not known whether the sectors or securities shown will be profitable in the future.

The information technology sector is now trading at 65 times next year’s earnings. This leaves very little room for disappointment either in terms of growth not materialising or for long-term discount rates to move higher. The lesser talked about risk is if global growth broadens out, improving the prospects for many other companies and reducing the excessive premium investors are willing to pay for the few growth companies. As other companies offer more growth and compelling value, the risk reward shifts and investors rotate. In the later part of 2020 we observed the early stages of this rotation and it will likely continue to be a theme in 2021. Since late August 2020 the US bond market has been pricing an improvement in economic growth and an increased likelihood of eventual inflation suggesting both the assumption of growth not broadening and lower discount rates into perpetuity are not without risk.

Extreme valuations aren’t the only sign of exuberance

Stretched valuations are a sign of increasing risks but there are also many other signs of over exuberance.

- Corporate behavior – huge issuance, including IPO, SPAC’s, M&A, and increasing corporate debt

- The proportion of companies that would not be viable but for ultralow rates and fiscal support

- Exponential price increases – e.g. Tesla or Bitcoin

- Positioning – low cash levels reflecting close to full investment

- Narrow rally – a few mega capitalised stocks driving almost all the index returns

- Speculation – increase in online trading, speculation and leverage (Robin Hood etc.)

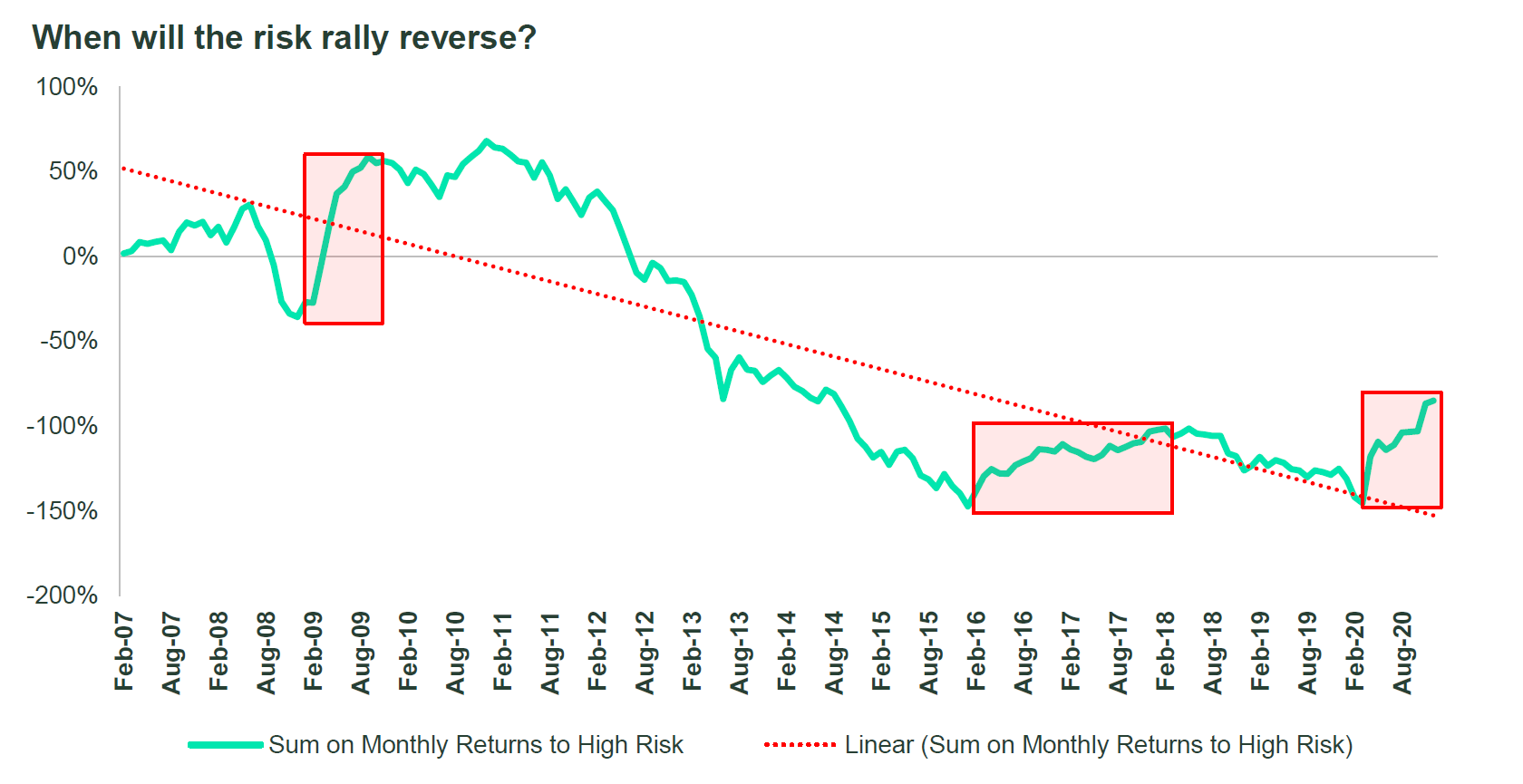

- Risky stocks are outperforming less risky stocks – (see Figure 3 below).

Stay positioned for the reversal of the risk rally

The psychological pressure to join the momentum trade is huge. As prices increase many investors will be more easily swayed by arguments for ever increasing prices. After all millions of people could not be wrong – could they? Stories of your friends and colleagues retiring from their Bitcoin accounts or 100% returns in 2020 will entice many to jump on the trends especially when the prices are moving exponentially. Chasing the momentum trade is especially dangerous in the later stage of the exuberance.

Figure 3 below places some historical context to the risk rally that we have seen since the market bottomed in March 2020. It shows that from time to time higher risk stocks outperform (like since March 2020) but also shows that these periods are usually short lived. Eventually the gains made by the risk trade are reversed. We are currently experiencing one of these episodes and if history is a guide then it will likely dissipate in time.

Figure 3. Short periods of risky stocks outperforming followed by underperformance

When will the risk rally reverse?

Source: State Street Global Advisors as of 31 December 2020.

The Bottom Line: “Be fearful when others are greedy” Warren Buffet

With ultra-low rates, record fiscal stimulus and the COVID-19 vaccine the prospects for global growth and company earnings are significantly better than they were in March 2020. Since this time markets have rallied to above prepandemic levels and have factored in much of this positive story. When we look across the investment landscape we see many signs of over exuberance from corporate behavior to speculative trading and we are reminded of Warren Buffet’s famous phrase “be fearful when others are greedy”.

Never miss an insight

Stay up to date with our latest thoughts by clicking follow below and you'll be notified every time we post content on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets