Five signals we’re watching in 2019

Peering in the rear-view mirror, 2018 could be characterised by slowing global growth; central bank policy tightening; and escalating geo-political risk. These are not features typical of a strong performance in risk markets. Yet for most of last year, markets climbed this wall of worry.

But as these features crystallised in Q4—a quarter we spent predominantly underweight equities—volatility and ‘risk-off’ sentiment took hold. Worries about slowing global growth, the US-China trade war and Brexit cemented a ‘worry wall’ too high for markets to scale. This culminated in a difficult end for risk markets in 2018. Most major global equity indexes experienced double-digit falls in December. In contrast, more defensive government bonds rallied strongly, providing some portfolio protection.

Looking ahead, 2019 may well be another difficult year. While partial relief arrived in the first few weeks of the new year (with equities up 6% in January) volatility remains elevated, a cautious attitude to risk is needed, and portfolio diversification (as always) will be key. The sharper-than-expected slowing in global growth as 2018 drew to a close, and the lagged nature of economic data, suggest the next few months are likely to provide little further relief. Data on trade and activity, for some months to come, are likely to be disappointing across both advanced and emerging economies.

Key will be the extent to which central banks’ withdrawal from further tightening— as well as renewed China stimulus—can elongate the later stages of this macro cycle, both drivers behind our recent return to a more neutral risk stance. Assuming some calming in global geo-political tensions, H2 2019 may prove a better backdrop for moderate equity gains. For Australia, transitioning a mid-year federal election may also provide a better backdrop.

This month, we canvass the issues weighing most on markets and flag our updated set of ‘risk signals’ that we will be monitoring through the year. We also highlight our recent tactical shift to move more overweight international versus domestic equities (as growth expectations deteriorate and political risks escalate in Australia). In particular, we add further to our overweight emerging market equity position (held since September last year) and move back to neutral in the UK (from underweight) and Europe (from overweight).

“The alpha that’s so much in demand today is really the ability to see ahead to things others will see only afterwards….in the rearview mirror.”

Howard Marks American Investor, 2005

The two issues weighing most on markets

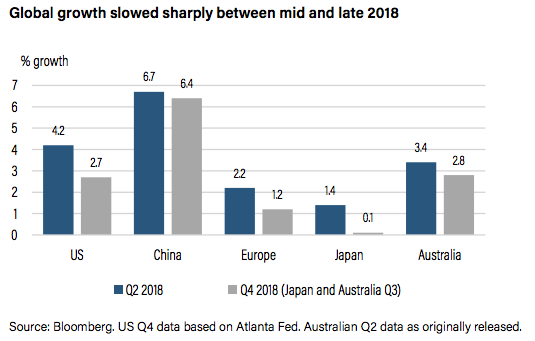

As we settle into 2019, the two issues weighing most heavily on markets are the sharper-than-expected slowing in global growth in late 2018; and the geopolitical flashpoints of the US-China trade war and Brexit. Global growth slowed sharply late 2018, weighing on earnings outlooks

Global growth lost considerable momentum as 2018 drew to a close.

Weak external demand was a common feature across both advanced and emerging economies. Moreover, business surveys pointed to an accelerating slump in business confidence and forward export orders. This is likely to be revealed in poor actual trade and investment data over coming months.

China and Europe attracted much of the attention. European data stalled in Q4 with industrial activity collapsing to its weakest pace in over three years. Indeed, some survey data suggest France has entered a recession. In China, December export growth cratered from around +6% to -4%, with only limited signs China’s recent policy easing was stabilising growth.

Harvard University Professor Rogoff’s comments that China’s slowdown was ’the greatest single threat to the global financial system’ also caught the market’s attention. Growth in Japan also unexpectedly contracted in Q3.

In the US, concern was focused mostly on the US Federal Reserve’s (Fed) still quite upbeat outlook and planned hikes for 2019. Worry that the December hike— the fourth in 2018—would further compromise earnings momentum through 2019 weighed heavily on markets.

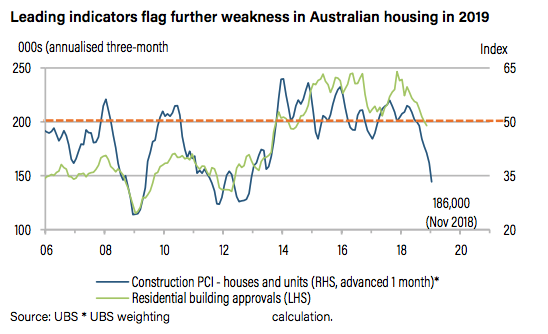

In Australia, data over recent months has also taken on a weaker tone. In Q3, growth unexpectedly dropped to a quarterly pace of just 0.3% from an above trend 0.9% in Q2. This was led by stronger-than-anticipated consumer weakness and flagging business investment. Consumer sentiment and car sales also fell at the end of 2018 and retail sales slowed, likely in part due to the recent acceleration in housing market weakness. UBS has cut its growth outlook for Australia due to “accelerating falls in home loans and prices”. Consensus has moved from expecting the Reserve Bank of Australia (RBA) to lift interest rates at the end of 2019 to speculating about an interest rate cut.

Trade wars, a ‘no-deal’ Brexit and Trump’s wall also weigh on sentiment

Sentiment also suffered in late 2018 as positive expectations from the G20’s November meeting between US President Trump and Chinese President Xi Jinping proved short-lived. Despite a delay in 25% tariffs until 1 March 2019, rhetoric from the US initially provided little hope that a deal could be struck.

Five signposts for a better second half?

A number of developments have underpinned a more positive start to markets in early 2019, with most equity indexes up strongly (around 6% in January) from their late 2018 lows. This raises the question of whether calm can return to markets as 2019 unfolds.

1. Major central banks step back from further tightening—The Fed has recently significantly softened its prior hawkish tone, emphasising ‘patience’ and ‘cross-currents’ to the economic outlook at its late January meeting. In Europe, given recent weak data, there is some likelihood the European Central Bank (ECB) will also delay tightening this year. Market pricing now points to both the Fed and ECB being on hold for the rest of this year.

2. Global growth outlooks trimmed but still solid—Despite the loss of momentum towards the end of 2018, reduced growth forecasts from UBS, the Organisation for Economic Co-operation and Development (OECD) and the International Monetary Fund (IMF) all continue to forecast near-trend growth in both 2019 and 2020. We expect some stabilisation in activity data to unfold after the downdraft in Q4 2018 and some likely further weakness in Q1 2019.

3. Progress by China to appease US trade concerns—China’s decisions around new intellectual property theft laws and the change in senior leadership rhetoric (as well as reduced auto tariffs and US soybean purchases) are being viewed by some as sufficiently ‘reasonable progress’ that President Trump will find it difficult to lift tariffs on 1 March.

4. Increased signs of China stimulus on activity—Data through January 2019 have shown tentative evidence that recent stimulus is having some stabilising impact on China’s growth outlook. Infrastructure activity has recovered modestly, and credit growth has stopped falling. January’s further cut to bank reserve requirements and income tax rates also aided sentiment.

5. Brexit negotiations inch towards a deal—While still highly uncertain, risks of a no-deal Brexit have been reduced. The probability of Prime Minister (PM) May’s Withdrawal Agreement being accepted, or some delay/extension to negotiations (or new elections and another referendum) has increased. Still, the potential for volatility remains as the 29 March deadline approaches.

Continued progress on these developments will be key to whether risk markets can face a more supportive backdrop as 2019 unfolds. If so, this could afford equities room to rise in line with current modest earnings growth outlooks. With central banks likely to be less active in 2019, exchange rate movements may also have less impact on activity and market returns.

For Australia, H1 2019 is likely to carry challenges ranging from uncertainty about the extent of the housing correction to elevated political uncertainty ahead of a federal election. As we noted last year, the potential for a change in government mid-May could see uncertainty weigh on a broad range of equity sectors, including health insurance, property, banking and utilities.

Five signals we are watching in 2019

In 2018, we established five signals we were monitoring in order to ensure it remained sensible to be engaged with risk. We do the same for 2019:

1. Simmering geo-politics—While a US-China trade deal seems unlikely, no sharp escalation in the trade war and no no-deal Brexit will be key.

2. Moderate rise in inflation—With tight jobs markets, inflation is likely to rise. Core measures in major markets staying at or below 2% will be key.

3. Moderate slowing in global growth—Growth is unlikely to return above trend. The global purchasing managers’ index (PMI) staying above 52 is key

4. Earnings continue to rise—Trend economic growth needs to translate into positive earnings growth, even if that growth is slower than last year.

5. China credit growth recovers—Credit growth slowed more than expected. Recent stimulus lifting growth back to around 10-11% will be key.

Adding further to our overweight in emerging markets

We continue to see 2019 as a year to ‘stay cautious, stay engaged’, as we headlined in our 2019 outlook late last year. We are neutral risk, a position adopted in early December 2018 following the equity market correction in October and November—and we have held this position through the December/January market volatility.

For equities, we remain tactically neutral overall. But this month we have increased the intensity of our preference for international over domestic. This reflects a combination of Australia’s recent relative outperformance, a less compelling earnings outlook, heightened concern about a housing correction that may add further downwards pressure to the Australian dollar, as well as rising political risk ahead of an expected federal election in May this year.

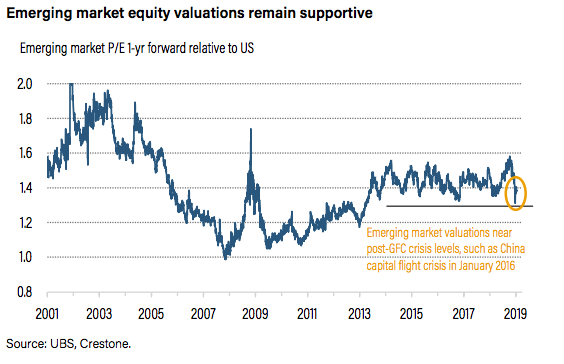

In September last year, we moved overweight emerging markets with a focus on Asia ex-Japan. Emerging markets have outperformed in Australian dollar terms since then. With valuations still attractive (see chart below), and some potential for stabilisation of the economic and geo-political backdrop, we have increased our overweight in emerging market equities this month.

With improved prospects for avoiding a no-deal Brexit, and now supportive valuations, we have also closed our UK underweight. After weak European Union (EU) data, we have also closed our European overweight. A reversal of fortunes for emerging markets would benefit both regions.

For fixed income, we stay tactically underweight. This is focused mostly on credit assets as central bank balance sheet repair (and liquidity withdrawal) is likely to continue for a number of years. Our recent tilt back toward defensive government bonds has proved sensible given the recent and prospective shifts in major central bank rhetoric towards less hawkish tones. We are still modestly underweight global government bonds, particularly for Europe.

Our underweight to fixed income is balanced by our strong overweight to alternative assets. Alternatives proved their worth as a portfolio diversifier in 2018, delivering positive portfolio return in the face of equity weakness. We continue to believe that alternative assets are an attractive prospect in the current environment of relatively low expected returns and high volatility.

Finally, this month’s increased tactical preference for international equities is not inconsistent with our recent review of our longer-term strategic asset allocations. Having reviewed our long-term capital market assumptions, we have made some modest shift towards international equities at the expense of domestic, due to the relative change in return assumptions between the two asset classes.

Never miss an update

Stay up to date with the latest news from Crestone by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Crestone? Hit the 'contact' button to get in touch with us.

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management