Fundies and Quants: Why you need both

Les Finemore

Imbue Capital

In recent years, two main approaches have evolved in the asset management industry: discretionary (think of the traditional 'fundie') and systematic (think of a quantitative fund). Here we look at their similarities and differences and make the case that there is a place for both in a portfolio.

These two styles of investing share a unique rivalry and I should know. I’ve sat on both sides of the fence in my time as a fundamental analyst and trader diving deep in to the world of global commodity markets.

In many ways, the two ‘tribes’ remind me of the old 'Ford vs Holden' rivalry in the Bathurst 2000..... You’re either one of us, or You're one of them!

The truth is that these two groups within the asset management industry are much more alike than many would have you believe.

I’ll be the first to admit that systematic managers have historically done a poor job at communicating their investment approach which has led to these misconceptions. In this wire, I’ll explore the common misconceptions, and why it makes sense to diversify across high-quality managers using both systematic and discretionary approaches to achieve long-term investment success. First, it’s worthwhile defining what each type of investment approach is.

What exactly is 'discretionary' and 'systematic'?

A discretionary approach involves detailed analysis that can rely on information and decision making that is not always easily explained. For many, decision making is based off experience, recognising that the current decision that is being deliberated on looks like ‘another one of those’.

For example, a typical approach for active discretionary managers in equities is to dive deep into the accounting statements to understand if a company may be trading above or below its true intrinsic value. Warren Buffett, Peter Lynch, and Ben Graham are examples of the subsector of discretionary manager known as value investors.

A systematic approach generally applies a more repeatable and consistent approach driven by data.

Within the ‘quant’ sector there is a myriad of different practitioners that range from employing basic statistical modelling, through to the use of the more innovative machine learning and artificial intelligence technology.

The active management industry primarily consists of discretionary managers with systematic investors making up a smaller amount of money managed by asset managers.

But this minority is growing in size. According to HFR, a hedge fund database provider, the quantitative hedge fund industry is on the brink of surpassing $1tn of assets under management in 2018 – nearly double the level of 2010.

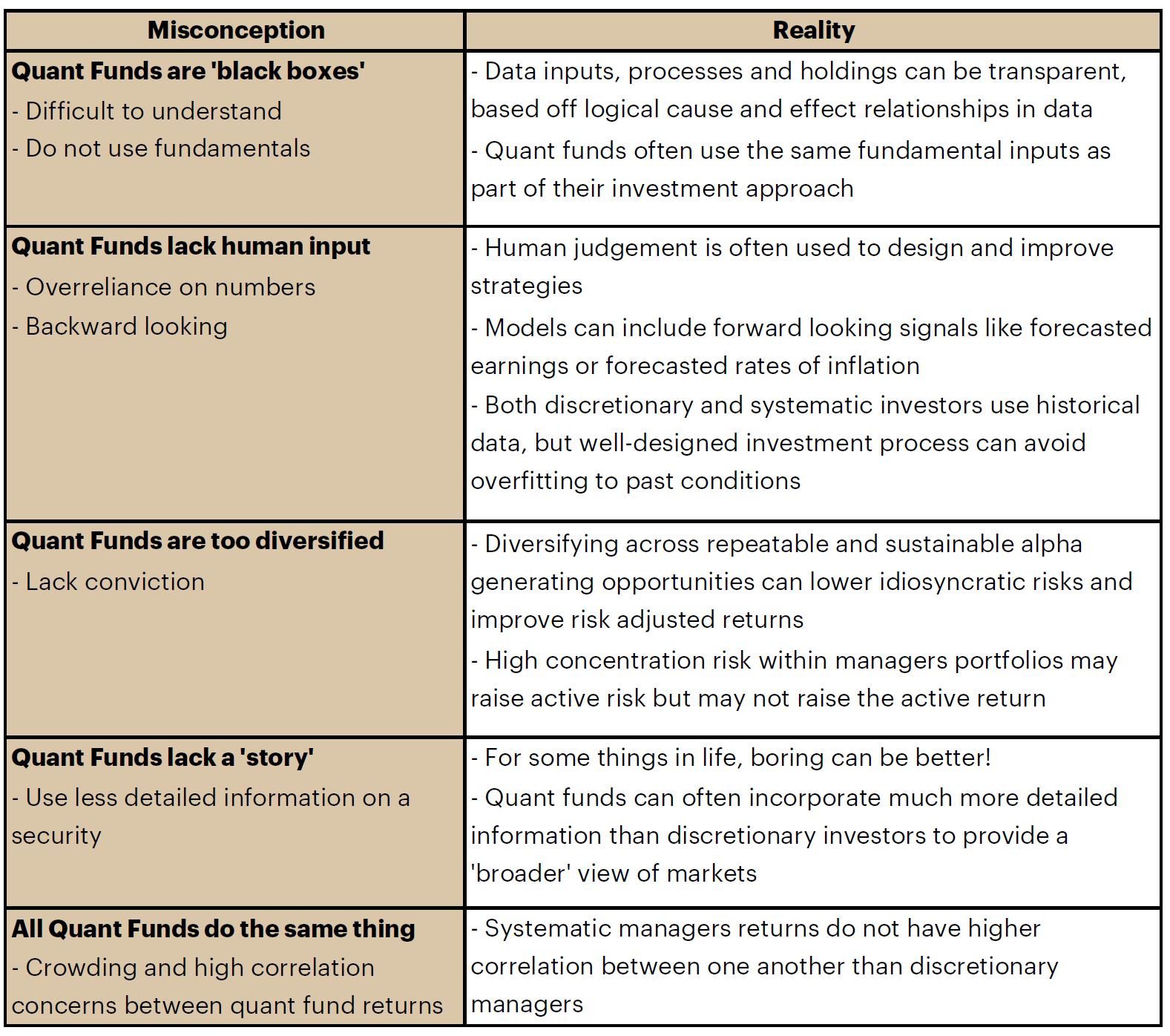

Debunking the myths

Despite the increasing popularity of quantitative strategies, there remain many misconceptions among investors. The major misconceptions being:

- Systematic managers simply deploy a ‘black box’ investment approach that lacks any insights from a human,

- That they lack diversification, and

- All quantitative asset managers are simply deploying the same strategy, such as risk parity or statistical arbitrage.

This table summarises these and other misconceptions and seeks to debunk them.

While there are differences between the two investment approaches, there are similarities. The way that I think about our AI focused investment approach is that we are exploring the complex correlations in data inputs much like a human discretionary trader who may call it ‘experience’.

The difference is that we are exploring these complex correlations at an immense scale that could never be completed by a human.

We do this in a very logical and rational way based on mathematical algorithms using thousands of data points that range from fundamental and event-driven, through to the more alternative (think satellite data and news article sentiment).

This is opposed to a human discretionary trader that may focus on perhaps hundreds of key data points. In my experience analysing such large volumes of data provides an asymmetric information edge or in plain English a broader, more complete picture of what’s driving global financial markets.

Not so very different

While systematic and discretionary managers may differ in the amount of data or at times, the type of data that is utilised, there is common ground that is shared between the two groups.

Often we’re saying the same thing but the use of lexicon is slightly different. While a fundamental manager might invest in a stock that has a 'catalyst', the systematic investor may call that 'momentum'.

Another common term favoured by fundamental investors is the theme of not fighting strong sentiment in a stock. We do this by ascertaining real-time sentiment in news articles and Twitter tweets, using Natural Language Processing machine learning algorithms to quantify this sentiment.

These examples are just a few of the commonalities that highlight how systematic investors can actually build trading strategies based off fundamental inputs, and completely refute the ‘black box’ label that is often applied to quantitative funds.

What is the performance and risk like?

Not only are systematic investors not a ‘black box’, but it also turns out that while systematic and discretionary investment approaches on average have produced similar historical performance figures, that systematic managers tend to have lower risk.

That notion was confirmed by the early academic work of Lakonishok and Swaminathan (2010). Generally, systematic managers employ greater diversification which can result in lower risk than discretionary managers.

The 2017 work completed by McQuiston et al highlighted two key points through their analysis of the eVestment database. The first being that while discretionary managers earn higher returns on average at the cost of higher risk, they found that systematic managers’ returns are less sensitive to market conditions.

The best of both worlds

While there are slight differences between the two approaches in terms of returns, the point is that they both have merit and when they’re both included in an investor's portfolio they can complement one another to provide higher risk-adjusted returns for an investor.

That is particularly the case if you can assemble a stream of returns from a variety of systematic and discretionary managers that have low correlations to one another.

References

- Lakonishok, Josef and B. Swaminathan (2010), “Quantitative vs. Fundamental,” Canadian Investment Review

- McQuiston, Karen, H. Parikh and S. Zhi (2017), “The Impact of Market Conditions on Active Equity Management,” PGIM Institutional Advisory & Solutions

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Les Finemore cofounded the artificial intelligence focused hedge fund Imbue Capital in 2017. Les brings a unique perspective on global markets that is shaped by his scientific and research background.

Les Finemore

CIO

Imbue Capital

Les Finemore cofounded the artificial intelligence focused hedge fund Imbue Capital in 2017. Les brings a unique perspective on global markets that is shaped by his scientific and research background.

Les Finemore

CIO

Imbue Capital

Les Finemore cofounded the artificial intelligence focused hedge fund Imbue Capital in 2017. Les brings a unique perspective on global markets that is shaped by his scientific and research background.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

High conviction: What we’re backing for the long term

Livewire Markets