Global Valuations: Everything is Expensive

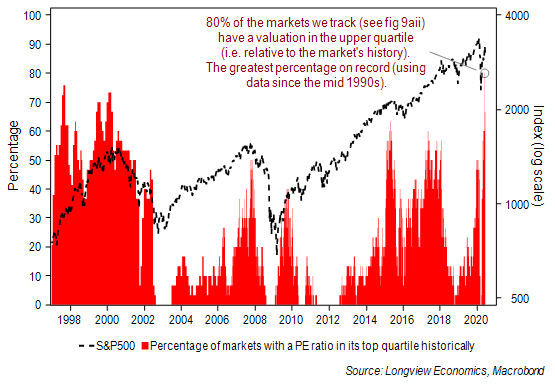

Following the fastest S&P500 bear market on record in March, the response from policymakers has been unprecedented, causing markets to rally aggressively. The S&P500 is up 42% from its March lows, despite earnings estimates being revised lower. This has resulted in the most expensive US equity market valuation since the dotcom bubble (21.4x forward earnings).

The bulls argue that this is justified by ongoing central bank largesse. As we have illustrated previously with our liquidity model, the primary driver of the PE rerating is, indeed, plentiful liquidity. The bulls also argue that ‘there is no alternative’ to equities, i.e. ‘TINA’, and that market participants are looking through 2020 earnings, and thinking about the market on 2021 or even 2022’s expected EPS.

Fig 1: Share

of global equity markets with a top quartile PE ratio* vs.

S&P500

*Using 12 month rolling forward consensus EPS for 30 country/regional equity markets.

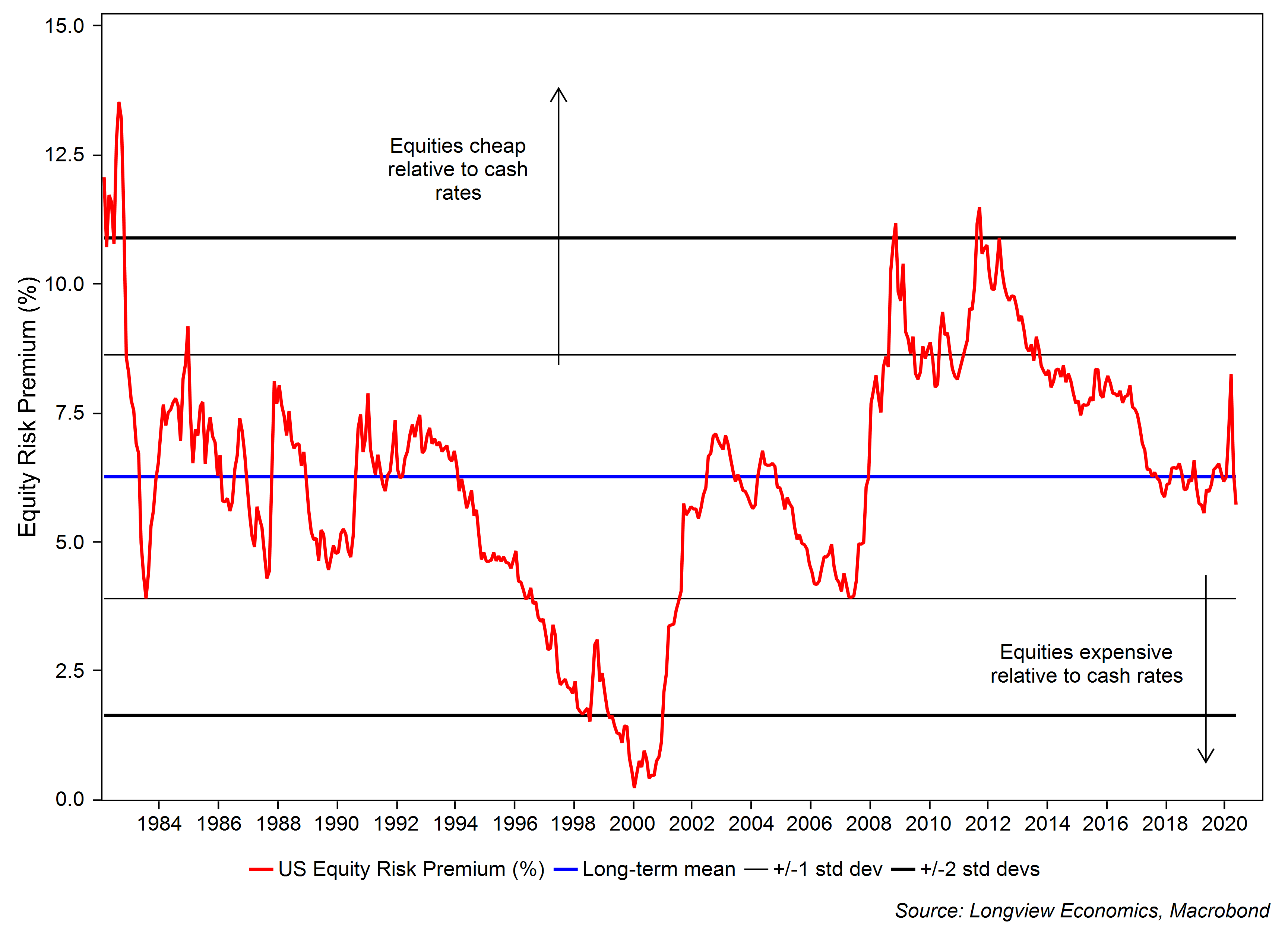

On the surface that argument is attractive. Cash rates are at/close to zero, or even negative, while real yields are at their lowest since 2013 (i.e. the last period of Fed QE).

On a closer inspection, however, the ‘TINA’ argument isn’t strong: Across a range of various risk premia, comparing equities to other asset classes, US equities are typically in line with, or even, below long term averages – that is, equities aren’t especially attractive on relative valuation metrics.

Measuring the S&P500’s risk premium using real yields, for example, shows that it’s at its lowest since 2009, and below its historical average; measured relative to real cash rates, the ERP is also below its long term mean (fig 2 below); against investment grade and high yield corporate bonds, the message is broadly similar. In Europe, the ERP has also fallen sharply and is now at its lowest since the GFC.

Fig 2: US Equity Risk Premium (earnings yield less real cash rates)

In our quarterly valuation analysis we look further into the detail to assess how expensive equities are across the different levels of market prices globally, i.e. at an index, sector, and single stock level. The full piece is available HERE.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

21 ASX stocks that should be on your radar

Livewire Markets

Equities

Wisetech tanks 17% on earnings miss but margins shine

Livewire Markets