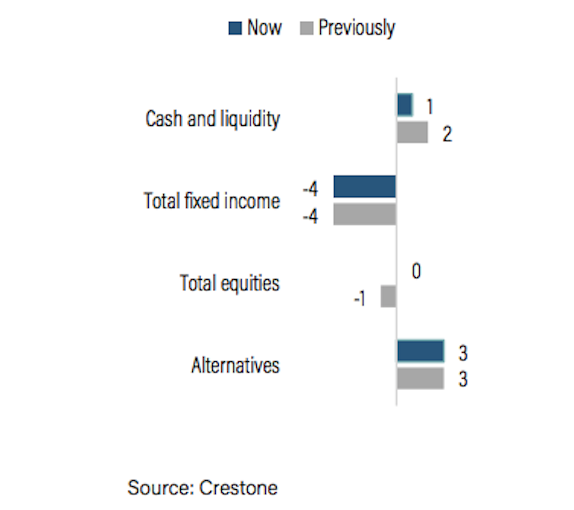

Going into 2019: how we are allocated

We have passed the peak in the global growth cycle. But conditions for an imminent sharp slowdown in activity are not yet in place. Growth is expected to be solid ahead, with further gradual increases in interest rates. Amid ongoing elevated volatility—but an expectation that a number of recent risk headwinds are fading—we are upgrading equities to neutral as we enter 2019. We are also remaining underweight fixed income (particularly credit) and continue to accumulate alternative, uncorrelated assets as we transition the later stages of the cycle.

2018 has been a challenging year for investors

After strong growth in the first half of 2018 accompanied by a pick-up in inflation, growth became less synchronised and slowed as the year unfolded. This led to concerns about rising interest rates, mostly in the US which, together with the negative impact of a strong US dollar on emerging economies, threatened the longevity of the cycle. Risk events, particularly the US-China trade dispute and Brexit deliberations, also frequently dented sentiment. These significant bouts of volatility, particularly at the start and end of the year, saw a material de-rating of risk assets, delivering more moderate returns than 2017 (much as we anticipated). For the year to end-November, global equities fell around 1%, but returned 6% in Australian dollars, outperforming domestic equities which fell 3%. Fixed income returns were largely flat as losses in credit were offset by bonds.

For 2019, global growth is expected to slow, but not enough to avoid further moves by central banks to reverse past years of abundant liquidity. After accelerating in 2018, growth in US and Australia is expected to slow below 3%. Better momentum is expected in Europe and Japan, while China is expected to ease policy to stabilise growth. A number of factors underpin our cautious optimism for an extension of the growth cycle for at least another year. In particular, the failure of inflation to challenge central bank targets will likely see the US Federal Reserve (Fed) signal a less hawkish stance ahead. This could stabilise an otherwise strong US dollar and provide some relief for emerging economies. Further, while geo-political risks and a maturing cycle will foster ongoing volatility, we take the view that risks around Brexit and the Italian budget are on the cusp of easing, while a further material escalation in the US-China trade dispute is relatively low.

Portfolio construction is likely to stay challenging in 2019

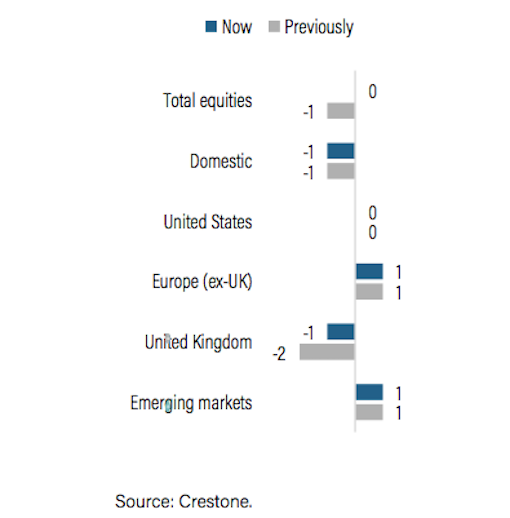

We are entering the year with a neutral attitude to risk. Indeed, it is not uncommon to be ‘sitting on the fence’ in regard to risk as the cycle matures. Notwithstanding our neutral equities position, we retain our recent preference for ‘value’ relative to growth, while also preferring international relative to domestic equities as growth slows and political risk rises. We remain modestly overweight Europe (better growth) and emerging markets (medium-term ‘value’), neutral the US, and underweight UK (though less so on improving visibility around Brexit). We are staying underweight fixed income, reflected most materially through credit (with a preference for bonds in Australia relative to international).

We are moving back to neutral for equities and maintaining a strong overweight to alternatives

Moderate global growth and rising inflation to persist in 2019

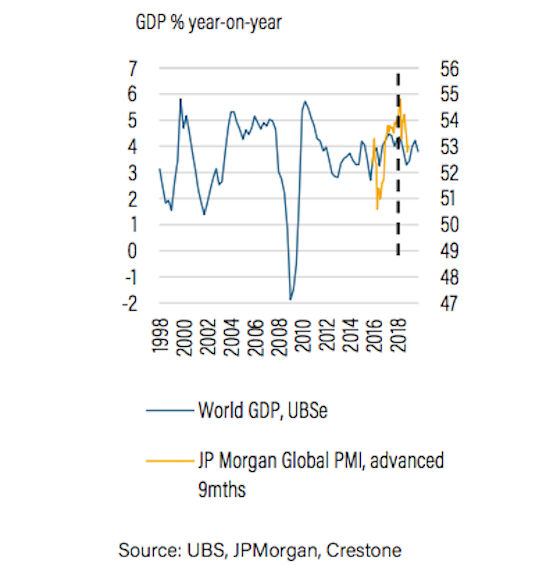

Looking ahead, most forecasts continue to flag a robust growth environment. Importantly, as we exit 2018, signals are scarce that a US recession—or sharp drop in global growth—is imminent. While job markets are tightening almost universally, and median global unemployment is at its lowest level since 1980, inflation (helped by the recent collapse in the oil price) looks set to rise only moderately during 2019. This reduces the risk that restrictive policy will terminate the growth cycle. Similarly, there is no evidence of excessive credit growth or a financial crisis, key signals the cycle may end imminently.

According to UBS, global growth is seen slowing from 4.0% mid-2018 to 3.6% in 2019, before stabilising at 3.7% in 2020. In its latest November update, the Organisation for Economic Co-operation and Development (OECD) similarly sees growth of 3.5% in both 2019 and 2020. Growth in the major economies is expected to be modestly above trend, led by a rebound in Japan and a modest acceleration in Europe from its late 2018 woes. In contrast, emerging market growth is expected to be modestly below trend, as China slows from 6.5% in 2018 to 6.0% in 2019 and 2020—albeit a strong post-election rebound is expected for Brazil in 2019.

Global growth is forecast to remain moderate until 2020

For policy, near-solo tightening of Fed policy in 2018 is likely to give way to more convergence in central bank rates ahead. The European Central Bank (ECB) is likely to end its bond-buying at the end of 2018 and tentatively lift rates late 2019, while moves to tighten policy in Japan and Australia will gather momentum as 2019 progresses. Modest rate hikes are expected in Canada, the UK and parts of the emerging markets by the end of 2020. This is likely to underpin further rises in international bond yields (especially in Europe and Japan), and present significant challenges for credit markets. For fiscal policy, according to UBS, the global impulse is “largely flat”, as US fiscal stimulus fades but China eases to offset any trade war impact on exports.

Positively, after a year of rapidly rising geo-political risks, we see 2019 as a year where volatility remains elevated, but the ‘clouds of crisis’ show signs of clearing. In particular, we expect more market-friendly developments around Brexit and the European Union (EU)-Italian budget dispute, while further escalation in US-China trade tensions are not expected. Further, as we have flagged for some time, we expect some softening in the Fed’s hawkish mid-2018 tone, which would provide some support for markets after the recent correction. Together, this should allow global equities to grind higher in line with moderate 8-9% earnings expectations (albeit Australia is half this pace).

Key risks to our outlook centre on Fed belligerence and a third-round escalation in the US-China trade dispute. US policy-makers may over-tighten despite recent signs that competitive secular trends continue to moderate inflation’s rise. An unexpected jump in global inflation would deliver a similar negative impact for both equity and fixed income markets. Another escalation in the US-China trade dispute that shunts the global growth cycle prematurely weaker and unanticipated signs of an impending US recession would be similarly problematic for equities—although in this case, defensive international bonds would outperform.

Asset class outlook

Modestly underweight domestic equities—slower earnings, rising political risk

Domestic equities have a less compelling earnings outlook compared with offshore markets, which offer greater exposure to faster growing secular trends (such as technology and healthcare). Moreover, while growth is only likely to slow toward trend, there are risks of a sharper downturn as the housing market corrects. A looming federal election, and likely change in government mid-May, could see uncertainty weigh on a broad range of equity sectors, including health insurance, property, banking and utilities.

Perhaps the biggest investment decision in 2019 will be whether the sharp ‘growth’ sell-off in late 2018 is a buying opportunity, or presages a change in market leadership. The most recent drawdown of growth-stocks was a fourstandard deviation event, exacerbated by crowded positioning and stretched valuations. In fact, although the broader market is trading in line with long-term averages, it masks a large divergence between high and low price-to-earnings (P/E) stocks, a gap that is at its widest since the GFC.

Growth stocks still have P/Es that are around one third above long-run averages. Investors will need to be cognisant of several factors that make certain growth stocks more susceptible than others over the course of 2019—namely, weaker price and earnings momentum, large share issuance, high gearing, large goodwill balances, lower levels of profitability and valuation.

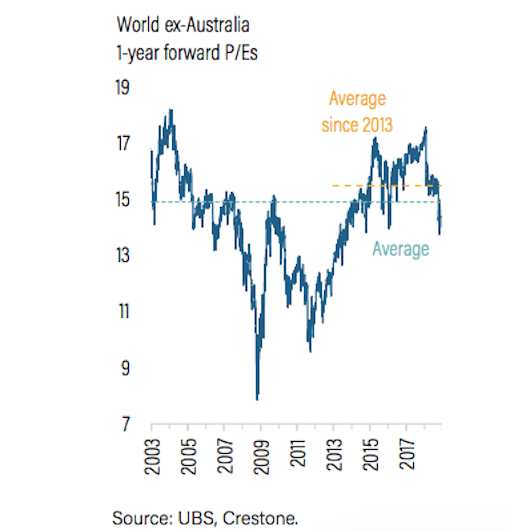

World equity market valuations are now less demanding

International equities—grinding higher on modest earnings

For the US, perhaps one of the over-arching factors governing equity markets in 2019 will be that, for the first time in many years, cash will be a competitive, alternative asset class. Earnings per share (EPS) growth is expected to fall sharply from around 24% to mid-to-high single digits. This is in line with the rest of the world, reducing the US’s competitive position in a global context.

After posting its fifth best year ever in 2017, the Asia-Pacific region is posting its sixth worst year in its 31-year history in 2018, down 15% in US dollar terms. There is valuation support, with Asia ex-Japan trading on a price-to-book (P/B) value of 1.28x (just 5% above the 2016 lows) and investor capitulation now greater than it was at the 2016 lows. Emerging markets will need a catalyst beyond valuation and this is likely to come from the evolution of macro and geo-political events. These include the outcome of the US-China trade dispute; whether China’s recent fiscal, monetary and macro-prudential easing measures can cushion any macro slowdown; and what trajectory the Fed funds rate takes from here, as well as the impact on the US dollar.

Sell-side STOXX Europe 600 index targets for the end of 2019 are approximately where they were 20 years ago. The 12-month forward P/E sits below its 30-year average and has de-rated by around 25% since quantitative easing (QE) began in April 2015. This is unusual in the context of the US— more so when you consider that in Europe a 4% cash yield is still vastly in excess of the yield on sovereign and corporate bonds.

Our modest overweight in global equities is concentrated in both Europe (deep value with improving macro prospects) and emerging markets. The potential de-escalation of global trade tensions, and a less hawkish Fed that stalls the US dollar’s upward trend, are factors likely to benefit these markets.

We remain overweight European and emerging equities, favouring global over domestic

We expect to be underweight most international fixed income asset classes

The gradual rise in interest rates is likely to persist as global central banks look towards monetary policy normalisation in 2019 and 2020. The tug of war between growth and inflation is likely to persist throughout the coming year creating some volatility in interest rates. The end of QE in Europe is likely to add fuel to widening credit spreads.

Domestically, with limited signs of wage pressure despite low unemployment, and the momentum of weakening housing market, the Reserve Bank of Australia (RBA) is expected to remain on hold until at least late 2019. There will be particular concern the domestic banking environment will put pressure on funding levels across capital structures. The uncertainty of policies in the political environment pre and post elections, and further uncertainty in the regulatory environment to determine how banks will be required to raise further loss-absorbing capital. This is likely to put pressure on wholesale funding levels and widening spreads in both financial and corporate bonds.

We are likely to be neutral on duration while the RBA remains on hold, noting that Australian government bond yields are likely to outperform global counterparts and offer a defensive asset class in volatile markets.

We expect the Australian dollar to drift higher through 2019

The Australian dollar has trended lower through 2018, from around USD 0.81 in January to around USD 0.72 in the last quarter. The currency may face some additional downward pressure over coming months, as the Fed continues to hike rates and the RBA remains firmly on hold. However, we expect some recovery in the Australian dollar toward USD 0.75, most likely in late 2019. This should reflect peaking US policy tightening, as the RBA turns its attention to normalisation; a return of domestic core inflation to the bottom of the RBA’s inflation target; stabilising expectations about the outlook for global growth; and increasing signs of stabilising China growth on the back of policy easing. A sharper-than-expected slowdown in Chinese growth below 6%, a sharper-than-expected moderation in commodity prices or more aggressive tightening from the Fed could undermine an expected rise in the Australian dollar.

This article was a collaboration between Scott Haslem, Chief Investment Officer; Rob Holder, Assset Allocation and Portfolio Analyst; Todd Hoare, Global Equities Specialist and James Williams, Head of Capital Markets and Fixed Income

Further Insight

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

Comments

Comments

Sign In or Join Free to comment