Gold surge draws wider interest

Kate Howitt

Fidelity International

Gold often glitters at its brightest when other risk assets lose their sheen. So far, the metal has largely proven an effective hedge against recent market volatility amid the global Covid-19 coronavirus outbreak, with prices topping US$1,600 per ounce in recent weeks. Looking ahead, we see more potential support for gold as investors price in plans among policymakers to roll out additional fiscal and monetary easing measures.

But it’s not just the metal. Gold miners have also been outshining the broader market and in our view, the higher price of gold is not yet fully baked into share prices.

Australian miners are uniquely positioned within this space as dynamics in the currency market tend to amplify their returns: when global investors shy away from risk, the Australian dollar tends to depreciate, while gold prices rise in US dollar terms. This boosts the gold price, and the miners’ returns, in Australian dollar terms. This dynamic runs counter-cyclical to trends in mining for other metals, which have mostly seen demand plummet due to the impact of the coronavirus outbreak on industrial activity in China.

Golden rules

At current gold prices, exploration has the potential to generate very high returns. With an industry discovery cost of around $50 per ounce, mining companies generally earn more than $1000 per ounce of EBITDA (earnings before interest, tax, depreciation and amortization), when it’s removed from the ground.

How then do we explain why gold miners have tended to underperform gold prices, when they should have outperformed? Quite simply, mines are hard to run well and poor capital allocations are sometimes made.

Historically mining company management teams have been pro-cyclical. In other words, they invest more in their assets when the gold price is high. This however leaves them vulnerable when the gold price falls and investments are more difficult to justify.

Rather than owning a variety of gold miners, investors need to be selective. This means identifying companies with good assets, and management teams that are focused on creating value rather than volume. Basically, companies with a track record of making savvy acquisitions and then knowing how to maximise their cashflow streams.

Digging deeper

Many mining companies have implemented learnings from the past and are becoming better operators and capital allocators. Value is also being created through industry reorganisation, consolidating mismanaged assets, and executing turnarounds. The supermergers of Barrick-Randgold and Newmont-Goldcorp for example set the scene for a new form of disciplined capital leadership.

ESG considerations

When it comes to environmental, social and governance (ESG) factors, the mining sector tends to be fraught with risk. One way we seek to navigate this and identify better performers is by looking at company-level initiatives around conservation.

In Australia, for example, a major challenge for gold miners is water usage. A number of mining operations are situated close to population centers and use shared water resources which may be disrupted in times of drought or bushfire. This is a risk that needs to be monitored closely as it may impact or halt production.

Supply and demand

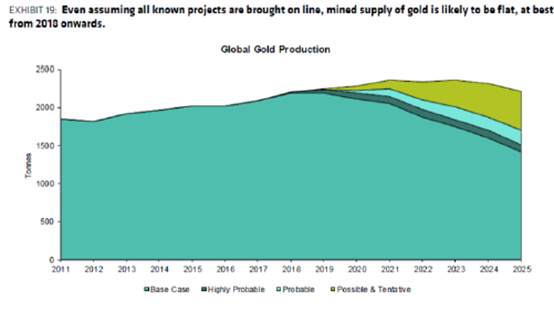

Supply is another factor to be considered. The sector must replace 17 per cent of current supply by 2028 just to keep annual production flat which would require around $5 billion of additional investment each year.

This supply constraint should incentivise greenfield developers (often called junior miners) which at current prices have the potential to earn large profits. Capital for these types of greenfield projects however is often scarce as many investors tend to favour more mature producers.

Valuations still attractive

Unlike many other sectors, current valuations for gold miner’s look quite cheap due in part to current market volatility. Passive exchange-traded funds are a popular way for investors and traders to gain exposure to gold miners and these vehicles own a significant proportion in the small and mid-cap gold sector. Recent market volatility has triggered a sell-off of these ETFs and of the underlying securities and are now trading at large discounts to NAV, which is extremely rare. Underlying gold stocks have also been negatively impacted providing long term fundamental investors with some good buying opportunities.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Kate has sole responsibility for the Fidelity Australian Opportunities Fund. In 2015 she was named Money Management’s Women in Financial Services Investor of the Year, and in 2016 was included in CNBC's "world's top 20 female portfolio managers".

Featuring

Kate Howitt,

Fidelity International

Kate has sole responsibility for the Fidelity Australian Opportunities Fund. In 2015 she was named Money Management’s Women in Financial Services Investor of the Year, and in 2016 was included in CNBC's "world's top 20 female portfolio managers".

1 topic

Kate Howitt

Portfolio Manager, Australian Equities

Fidelity International

Kate has sole responsibility for the Fidelity Australian Opportunities Fund. In 2015 she was named Money Management’s Women in Financial Services Investor of the Year, and in 2016 was included in CNBC's "world's top 20 female portfolio managers".

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

High conviction: What we’re backing for the long term

Livewire Markets