Good news stories buried in reporting season

IT consulting group Empired (EPD) and brand design, distribution and retail player PAS Group (PGR) were two small companies that appeared not to receive the acclaim they deserved for their earnings results and guidance last month.

Equitable Investors Dragonfly Fund owns both these stocks.

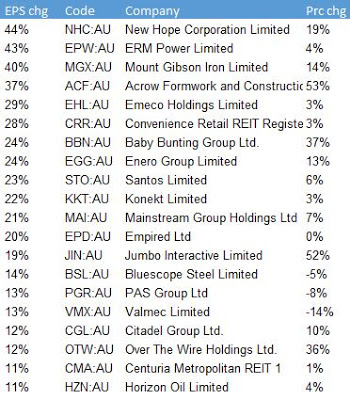

At the conclusion of reporting season we reviewed changes in analysts' earnings expectations and found that while EPD and PGR were receipients of some of the largest Earnings Per Share (EPS) upgrades by analysts, their share prices were stagnant.

Figure 1: Biggest FY19f consensus EPS upgrades over month of August 2018 & price changes that month

Source: Sentieo, Equitable Investors

Seeing double digits

In the case of EPD, an IT services provider with over 1,000 staff and an ~$85m market cap, the company had already provided detailed guidance and there were no surprises with its FY18 results.

Importantly, EPD reiterated FY19 guidance of double digit growth in EBITDA, NPAT and EPS. Management said the outlook was underpinned by a strong exposure to digital solutions and an expected solid recovery in its New Zealand business, which had struggled during FY18 as government spending was curtailed for a federal election campaign (EPD has this week announced a new $NZ10m, two-year contract in NZ for the Department of Internal Affairs).

EPD has historically faced questions from some investors over its ability to generate cash and has promised strong cash generation in FY19 as it continues to tightly manage working capital and capital expenditure requirments decline. From a point a couple of years ago where EPD was considered by some investors to have too much debt on balance sheet, it is now "approaching" a net cash position at the end of FY19. That will position EPD well to look at earnings-accretive acquisitions in the following year.

On consensus numbers, EPD is now priced on a Price-to-Earnings (PE) multiple of 10.8x and an Enterprise Value-to-EBITDA (EV/EBITDA) multiple of 4.7x. Analysts are estimating EPS growth of 63% this year and 18% next year.

Out of fashion but going places

While fashion retailers Specialty Fashion Group (SFH) and Noni B (NBL) have experienced significant re-ratings on the sharemarket over the past 12 months, PGR has flown under the radar.

PGR (debt free other than a $732k overdraft) has a market cap of only $42m. It operates 256 retail stores under the Review, Jets swimwear, Black Pepper, Yarra Trail and White Runway labels. Its loyalty program has swollen 25% in FY18 to 943,000.

Unlike SFH & NBL, PGR is not just a retail operation. It has a significant wholesale design and distribution business, Designworks, that licences a host of well-known brands like Disney, Star Wars and Sesame Street. Designworks has also been busy building a significant leisurewear offering encompassing Everlast, Russell Athletic, Lonsdale, Slazenger and Dunlop.

Last week PGR furthered its sporting agenda when it announced that Dunlop had been appointed as the official ball partner of Tennis Australia, meaning PGR's licensed product (Japanese corporation Sumitomo owns the Dunlop brand) will displace Wilson tennis balls at the Australian Open.

Group revenue in FY18 was $256m. PGR has stated that it is "is well placed to deliver sales growth" with $35m to $40m in new business for delivery by Designworks in FY19 and beyond.

PGR reported $11.2m EBITDA for FY18, within its guidance range of $10m to $13m in a year that was depressed by continued declines in sales out of concession stores within Myer and the addition of costs ahead of the ramp-up of new contract wins. A reported net loss of $2.9m was the result of a $5.5m impairment charge against White Runway, a bridesmaid and bridal chain that has proven less scalable than intended.

Taylor Collison, the one broker with coverage of PGR, has it priced on a PE multiple of 7x for FY19 with adjusted EPS more than doubling in FY19 then growing another 15% in FY20.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

2 stocks mentioned

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

Expertise

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

Expertise

Comments

Comments

Sign In or Join Free to comment