Good results see months of buying

I have noticed over the years (and now have the hard evidence) that how the majority of stocks move on day 1 of their results generally determines where it will be 4 months later.

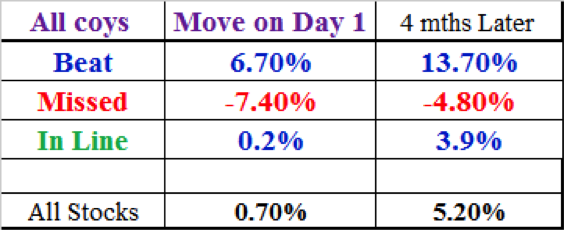

This is something I wrote about on Livewire in the February reporting season, and since then the argument has only got stronger based on data from the February reporting season, shown below:

Source Coppo Report

We can see that the beats were a lot better than the misses. As you’d expect the stocks that “beat” were up on day 1, and were up by +6.7%. Then 4 months later (ie as at 15th June 2018) they were up +13.70%.

In other words, they have rallied another +7% since reporting. The ASX 200 rallied +2.7% over this same time.

The Misses were smacked -7.4 % on the day they reported, but improved by +2.7% to be down just -4.8% 4 months later. But they have been helped by the fact that the ASX 200 rallied +2.7% in the 4 mths since that Feb Reporting season.

Also of interest is that these stocks (misses) had the highest short interest (2.8%), so it looked like the shorts were more correct on these.

The 25 companies that beat expectations so far...

The FNArena Reporting Season Monitor provides a weekly update of the companies that beat/missed expectations. Click here for the latest update.

--

This article is based on excerpts from The Coppo Report contributed to Livewire by Richard Coppleson, Director - Institutional Sales and Trading, Bell Potter. You can find out more by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

Expertise

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Commodities

What ASX rare earths stocks could Trump buy?

Livewire Markets