Grant me one more boom and I promise not to waste it

Kyle Schlachter

Territory Funds Management

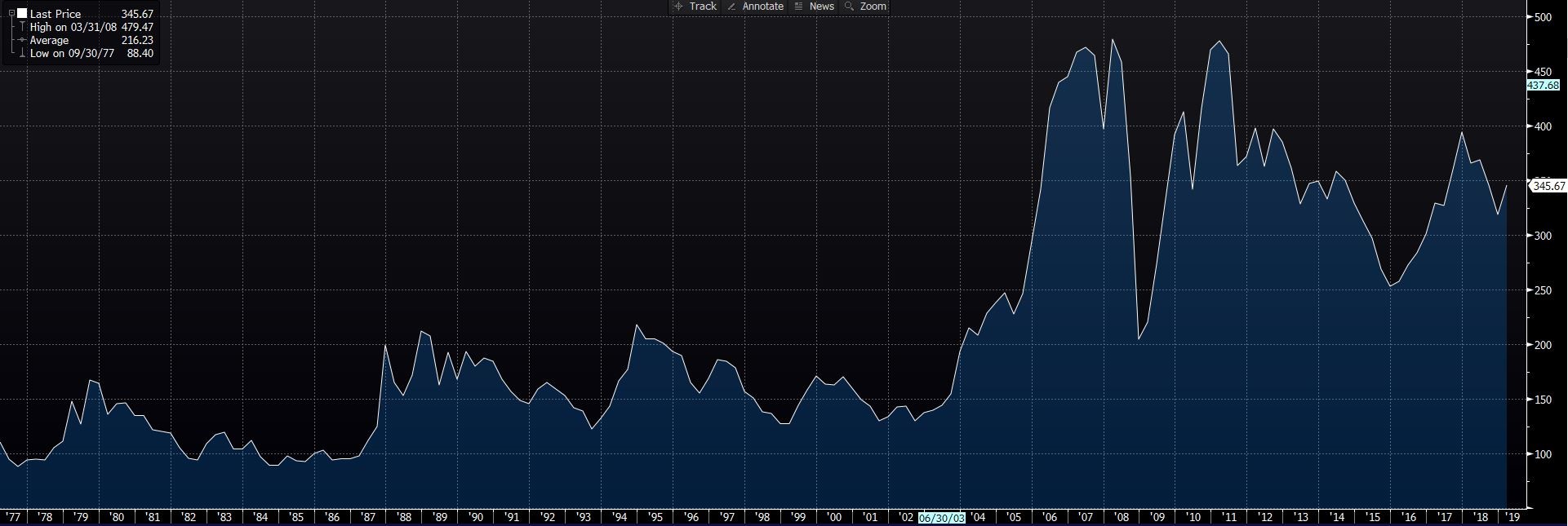

As China ramped up during the noughties (2000-09), commodity prices surged; the super cycle in commodities had begun. Eventually prices took a pause as China shifted gears, but a “new normal” was set for industrial metals, iron ore and coal.

“Grant me one more boom and I promise not to waste it" ~ Anonymous

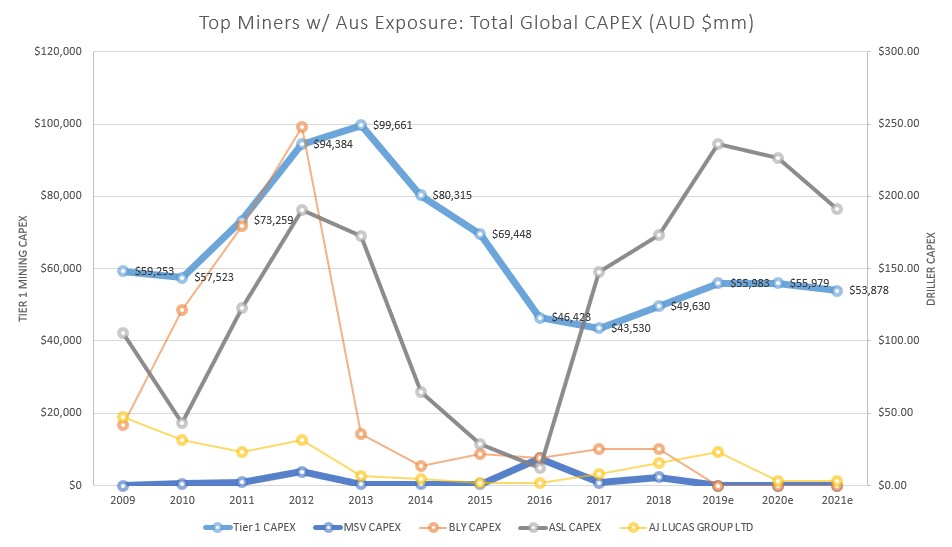

A fall in mining expenditure between 2014 – 2017 trimmed share prices, fleet sizes, and bottom lines for Australia’s mining service companies, with drillers hit hard. Firms that over capitalized during the run up between 2010 – 2013 were punished severely. Share prices fell 60-100% from 2012 peaks to 2015 lows. During the peak of the cycle the top 20 mining companies with Australian exposure were spending $100 billion world wide in 2013. Shortly after BHP announced the cancellation of the Olympic Dam expansion in SA, the fall in spending had begun. By 2016 those same 20 mining companies had trimmed their capex spending to $44 billion across their global portfolios. Less spending means less meters drilled and a whole lot of suffering for anyone plying their trade with a rig.

(Source: Bloomberg)

Today, prices for commodities have rebounded to their new normal level as China continues to expand its infrastructure, and rumours of stimulus spending into the Chinese economy circulate. The S&P Industrial Metals Index, with an underlying of five different commodities (Aluminum, Copper, Zinc, Nickel and Lead) is a good representation of the rise in price that occurred post 2000. Continued global demand bodes well for increased CAPEX spending in the future.

(Source: Bloomberg, S&P)

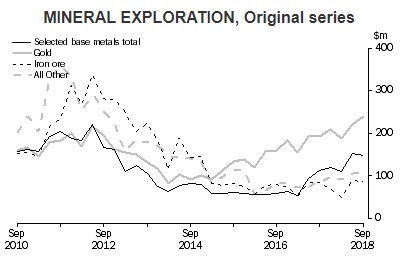

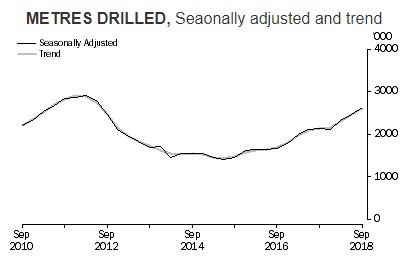

(source: Australian Bureau of Statistics)

Strong commodity prices and the subsequent CAPEX spend has begun to filter through to Australia. Australian miners have responded with increased spending according to the Australian Bureau of Statistics.

In their latest report, released Dec 2018, trends are reversing for the nation’s mining industry as meters drilled rose to +23% pcp in Sep 2018. Total expenditure climbed, with total mineral exploration topping $561m for the latest quarter. The figure was down from the peak of $1b+ in 2012, but a 26% increase on Sep 2017.

The rising tide in mining floats all boats, and the drilling industry is set to benefit as we move through the service cycle. Prices are supporting increased spending and the top mining companies are reciprocating.

The Mining Drilling Industry

The mine specific drilling industry in Australia provides brownfield and greenfield services to the country’s miners. These services are essential to the development of new mine sites, gas drainage in existing mine sites, and the extension of current sites.

There are about 500+ drilling service operators in Australia, providing equipment, human power and expertise to the mining industry. The industry itself is quite fragmented, with most service providers operating a single rig. Larger players in the industry account for 44% of the market, with market share garnered by Boart Longyear (20% - 676 rigs), Ausdrill (9% - 400 rigs) and AJ Lucas (5% - 30 rigs). All three companies engage in international operations, and apart from AJ Lucas (AJL), do not domicile their entire fleets domestically.

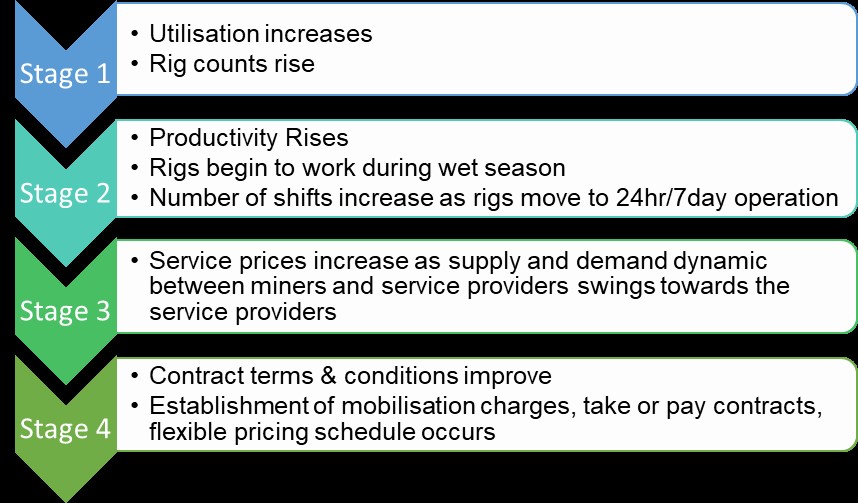

Service Cycle Defined

As activity rises and capital spending increases in the mining industry, we begin to move through the service cycle.

When the cycle eventually reverses, the cycle will retrace its steps as contract terms worsen, service pricing drops, and rig utilisation falls. As things unwind companies that were prudent during the upswing are rewarded.

Recent results for Boart Longyear (BLY), Ausdrill (ASL) and Mitchell Services suggest we are entering stage three of the cycle, as revenues and gross margins have improved.

|

|

Recent Filing* |

Previous Filing* |

|

Gross Margin |

Gross Margin |

|

|

BLY |

18.5% |

15.3% |

|

ASL |

18.1% |

17.8% |

|

MSV |

35.7% |

26.2% |

|

Company |

Revenue (AUD $MM) |

Revenue (AUD $MM) |

|

BLY |

770.2 |

739.1 |

|

ASL |

642.5 |

440.9 |

|

MSV |

63.3 |

33.2 |

*For BLY the full year results were used, for ASL and MSV half year results were used. These were the most recent filing for each company.

As CAPEX budgets continue to drive the service cycle, we will see improved contract pricing, eventually moving towards improved terms. Existing companies in the sector will be able to take advantage of stage three and four of the cycle, as their established relationships through the down cycle, balance sheet management, and access to favourable credit terms act as a tail wind while the market becomes more buoyant.

On the latest investor call from Mitchell Services it was mentioned that the lead times to purchase new rigs were building. Four weeks lead time during the down turn for an underground rig has increased to 14 weeks. Surface rigs have been impacted more, with a new rig taking 6 months to construct. Conditions favour current providers that purchased equipment during the bottom of the cycle for cents on the dollar.

Service Offerings:

With industry spending increasing, miners are moving from a harvest mentality to an expansionary mindset. Operating costs at mine sites have been trimmed for the last few years as existing mines were optimized. This behaviour had an asymmetric impact on the mining service sector driving down margins and pricing.

As mining companies open the purse strings, development and exploration capital has begun to flow again. Service providers with a high drilling exposure will be the first to benefit, as increased development and exploration budgets are set to grow.

|

|

Drilling Types |

||

|

Method |

Description |

Advantage |

Disadvantage |

|

Reverse Circulation* |

Surface: Pneumatic Air Drilling |

Fastest drilling method

|

Cutting samples are poor for geological analysis |

|

Mud Rotary* |

Surface: Rotary Mud Circulation Drilling. |

Balanced approach, provides good rates of penetration and sample quality |

More expensive than air drilling, due to increased rig time |

|

Diamond Drilling |

Surface: A hollow bit returns an intact centre core |

Highest sample quality as an intact geological representation is retrieved |

Expensive (2x RC per metre costs) as coring increases rig time |

|

Underground |

Specialty drilling for development and gas drainage (coal mines) |

Gas drainage is a safety requirement of underground coal operations. Provides a base of work. |

Rigs are specialized and expensive in comparison to surface operations. |

*Universal rigs can provide RC, Mud Rotary and Diamond drilling services.

On the service side of the business there are a few listed options in Australia that let you play the mining drilling sector. It should be noted, not all service providers in the space have equal exposure to drilling, as some offer other service channels, as well as a multitude of drilling services. For example, surface drill fleets cater to a different customer and mine type than underground fleets. These distinctions drive further differences between industry players as the drilling specialities of each company’s fleet are unique.

|

|

Revenue % Drilling / Revenue % Australia |

||

|

Company |

Drilling Revenue % |

Australian Revenue % |

Comment |

|

BLY |

67% |

22%

|

BLY earns a third of their income from equipment sales and tooling. They are well spread geographically with operations in LAM (14%), the US/Canada (46%) and EMEA (18%). Their fleets cover all drilling types. |

|

ASL |

23% |

49% |

ASL despite their name earns most of their revenue from mining services, both surface and underground and not direct drilling. ASL provides a one stop shop model. |

|

MSV |

100% |

100% |

MSV operates 75% of their rigs at surface, with the other 25% dedicated to high margin underground delineation and degasification. All revenue is generated in Australia. |

|

SWK |

100% |

90%+ |

SWK specializes in underground diamond drilling (highest margins). With 90% of its fleet dedicated to underground delineation operations. |

|

AJL |

100% |

100% |

AJL has concentrated on coal degasification with its fleet of surface only rigs in Australia. In addition, it also owns interests in a UK shale gas company exposing the Company to exploration risk |

(Source: Company filings and investor presentations)

Valuations:

When it comes to drilling, we feel metrics that concentrate on a company’s ability to generate high margins, manage their debt position with prudent bottom of cycle equipment purchases and cash generation (EBITDA) outperform when choosing best in class.

|

|

Metrics |

|||||

|

Company |

Operating Margin |

Net Debt / EBITDA |

Min Operating Lease |

EV / EBITDA |

P/E |

Fwd P/E |

|

BLY |

5.05% |

9.27x |

$44.7m |

10.6x |

Neg |

Neg |

|

ASL |

36.52% |

1.42x |

Nil |

4.6x |

3.7x |

10.2x |

|

MSV |

13.50% |

0.25x |

$1.39m |

6.7x |

9.0x |

7.0x |

|

SWK |

4.50% |

1.07x |

$17.0m |

4.0x |

22.0x |

7.3x |

|

AJL |

12.77% |

4.78x |

$3.20m |

11.5x |

Neg |

10.0x |

(Source: Bloomberg and company filings)

In this note we will be highlighting Mitchell Services, as they compare favourably to their peer group and have come out of the downturn in fine position.

“If it can’t be done, we’ll do it”

~ Peter Mitchell, Mitchell Services

Mitchell Services:

Mitchell Services Limited is a Brisbane-based drilling services company, catering to exploration and brownfield clients in the mining sector.

The Company has a proud history in the industry, tracing its roots back to 1969, when founded by Peter Mitchell with a second-hand rig. In his iconic words, “if it can’t be done, we’ll do it”. Until 2008 when the Company was sold to AJ Lucas for $150m, the motto rang true, as the Company was prepared to go wherever there was work.

Operations domestically provided a base for international expansion, completing projects in India, Russia, China, Indonesia, and Africa, Mitchell Services was ready for any challenge the resource sector could throw at it. Post-sale of the domestic operations, a five year non-compete kept Mitchell Services from re-entering the Australian drilling market. At the agreement’s expiry in 2013, Mitchell Services in Australia was reborn through a reverse merger into Drilltorque (DTQ) who needed recapitalisation at the bottom of the market.

We pick up the story today, where the Company has returned to its roots, scooping up second hand equipment at reduced prices to build a fleet of 64 rigs at time of writing.

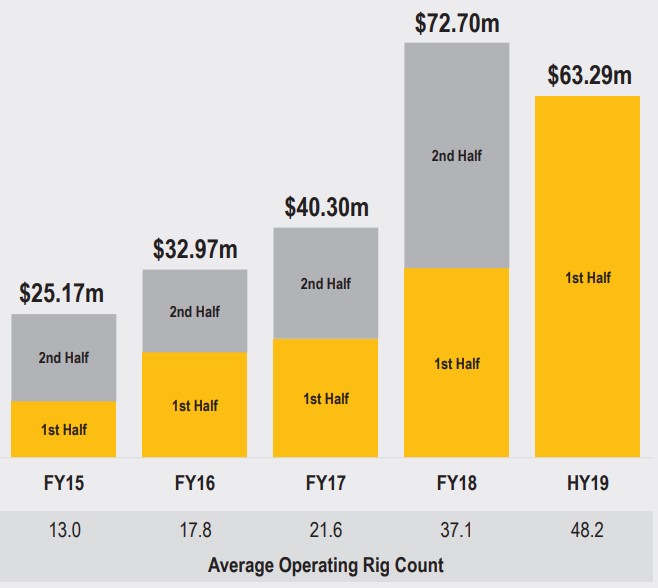

Mitchell recently had their investor call (Feb 26) reporting their 1HY19 financial results. MSV’s P&L swelled as revenues increased 91% pcp and EBITDA rose 431% to $14m for the half. Margins played well with EBITDA margin at 22% and a tidy $12m after tax profit reported, boosted by deferred taxes of $4m. MSV’s strategy of targeting Tier 1 miners and not discounting to win tenders proved fruitful.

The increased revenue allowed MSV to improve their debt position and increase flexibility paying off an $8.5m shareholder loan in Dec 2018, to bring net debt to $2.5m. The Company maintains a $9m working capital facility with NAB, and has a $25m approved equipment finance limit, allowing plenty of headroom above the $6.5m balance. Mitchell’s banking lines offer ample runway, with implied support for the addition of a further 19 rigs; a 30% increase in fleet size. The capital spend for the first half of FY19 was a prudent $3m, with second half spending to rise (FY18: $8m) as management hinted that continued expansion or acquisition was possible, but the metrics would have to be right. Mitchell is no stranger to acquisition, acquiring 11 underground drilling rigs and the associated long-term contracts in a $5.3m acquisition of Radco Drilling in Apr 2018.

In conjunction with the release of their financials, MSV announced a 10% on-market share buyback, to commence March 18 and lasting for a period of 12 months. The Company currently has 1,738.7 million shares outstanding.

For the first time MSV released guidance for their full year results, expecting the usual seasonality, more rain in H2 typically, and continued strong demand. Full year revenue is expected at $110 - $120m, generating $21 to $23m of EBITDA. If continued underlying profit margins are maintained and guidance met, MSV can expect to report an EPS of $0.008/share, before buy back. At a fwd PE of 10x, the forecast EPS returns a share price of $0.08/share, a 38% premium on current pricing.

(Source: Mitchell Services 1HY19 Investor Presentation)

Conclusion

As we enter the service cycle upswing, forward valuations look cheap for the drilling sector on a P/E basis, with positive momentum to rise further. Of the choices, we feel that Mitchell Services (MSV) is best placed, as its experienced management team, balance sheet management, existing relationships, and margins set the Company apart from their peers.

The drilling operators have begun to rise in value after the release of positive half year / full year results by some of the industry’s prominent players. Favourable developments in the mining industry have pushed the service cycle into the late stages where the sector can regain pricing power. The companies that survived the downturn are well placed to reap the benefits as the cycle rises.

“In investing, what is comfortable is rarely profitable.”

Robert Arnott, Research Affiliates, LLC

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Kyle is an Investment Analyst with Territory Funds Management. He has a B.Sc. in Electrical Engineering, earned his CFA charter in 2014 and has 13 years of experience in the Canadian and Australian petroleum industry.

Kyle Schlachter

Analyst

Territory Funds Management

Kyle is an Investment Analyst with Territory Funds Management. He has a B.Sc. in Electrical Engineering, earned his CFA charter in 2014 and has 13 years of experience in the Canadian and Australian petroleum industry.

Expertise

Kyle Schlachter

Analyst

Territory Funds Management

Kyle is an Investment Analyst with Territory Funds Management. He has a B.Sc. in Electrical Engineering, earned his CFA charter in 2014 and has 13 years of experience in the Canadian and Australian petroleum industry.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets