Growth vs. Value Investing. Think Differently.

The terms ‘growth’ and ‘value’ are used in ways that suggest you can divide stocks and investors into two opposing tribes, like Democrats and Republicans or the Montagues and Capulets. We show that as popularly used, these are flawed concepts. We demonstrate why, and offer an alternative.

It is understood that growth stocks will generate faster-than-average earnings growth, and that stocks that trade of low multiples of some variable are cheap. Naturally, Let’s see if these assumptions stand up to scrutiny.

Growth stocks

Growth indexes typically use three variables to select stocks that are expected to generate superior future EPS growth: growth in sales per share over the last three years; growth in EPS over the last three years; and price momentum.

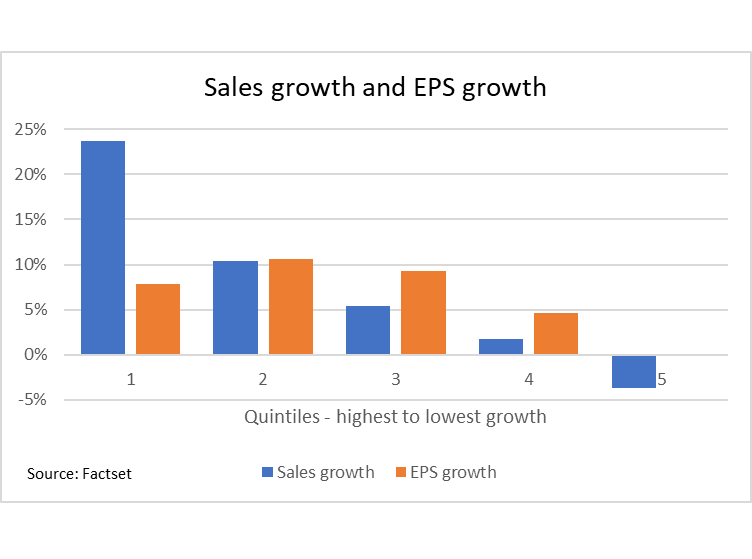

1. Past sales per share

There is no relationship between past sales per share growth and future EPS growth. We took the 733 US companies that have a market capitalisation greater than $5 billion and more than seven years’ history as a listed company. We divided them into five groups ranked by annualised sales growth over 2011 to 2014 and looked at the EPS growth over the following three years (testing over a different three-year period also showed no relationship). 2. Past EPS growth

2. Past EPS growth

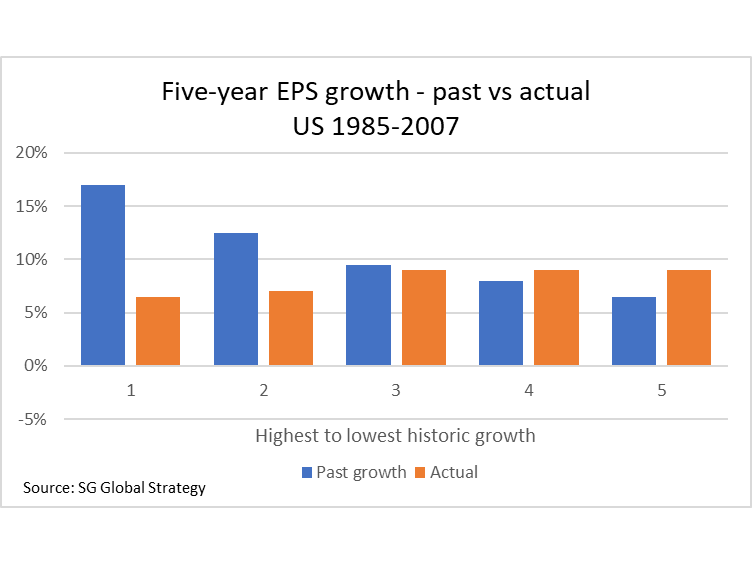

Société Générale’s Global Strategy team examined the relationship between trailing five-year EPS growth and future five-year EPS growth over the 22 years to 2007 (published in Value Investing by James Montier, 2009). They found no positive correlation between past and future growth. In fact, firms with the highest historic EPS growth had, on average, the lowest future growth. 3. Price momentum

3. Price momentum

There is no evidence that we are aware of that suggests superior future EPS growth can be identified through share price momentum.

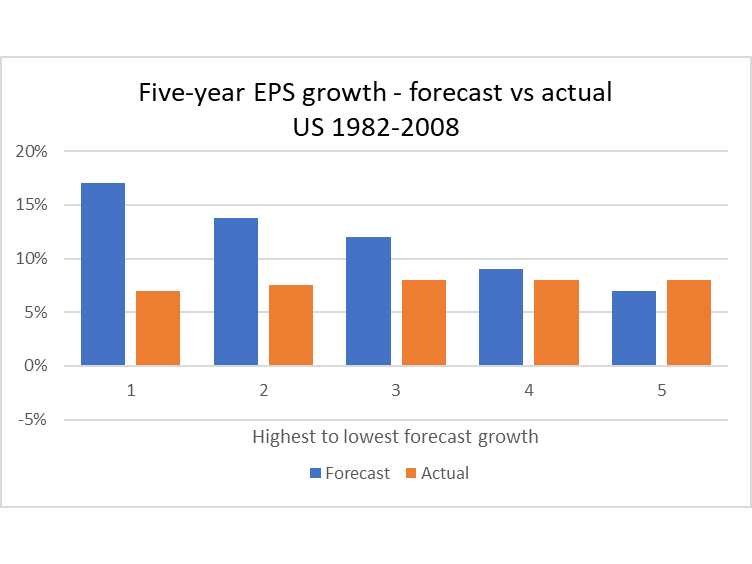

4. Forecasting

If future fast-growers can’t be identified quantitatively, can analyst judgement (on average) do better? The answer, as is clearly demonstrated below, is no. Some companies do indeed grow faster than others. However, they cannot be reliably identified by analysts, on average. Nor can they be identified by standard quantitative tools.

Some companies do indeed grow faster than others. However, they cannot be reliably identified by analysts, on average. Nor can they be identified by standard quantitative tools.

Value

Ranking stocks by measures such as PE, price-to-book or price-to-sales do not identify cheap stocks. They capture whether a stock trades on a high or a low multiple relative to the market. However, they do not capture the essence of value, which is where the stock trades relative to where it should trade. Designating stocks on below-average multiples as cheap, or ‘value’, and above-average multiples as expensive makes an implicit assumption that all stocks should trade on the same multiple. A low multiple does not mean a cheap stock.

Summary

Once you scratch the surface, the labels ‘growth’ and ‘value’, as used in relation to stocks and investment managers, don’t have the meaning that is conventionally attributed to them. Rather than thinking in terms of an artificial, binary distinction of growth or value, our approach is growth in value. Growth in value occurs through companies earning superior returns on invested capital. We look to own those select businesses that become more valuable over time, where we can own them at less than today’s value and where we judge the risk of disappointment to be low.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors.

He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based firm dedicated to a single strategy: a highly selective global equity portfolio.

Since its inception in March 2018 through to the end of April 2025, the Aoris strategy has ranked in the top 5% over 3 years, 5 years, and since inception, relative to a broad peer group of international equity funds (Morningstar). The firm currently manages just under $2 billion in assets.

Prior to founding Aoris in 2017, Stephen was Head of International Equities at Evans & Partners.

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Stephen has been investing in global markets for over 30 years, making him one of Australia’s most experienced international investors. He is the Founder and Chief Investment Officer of Aoris Investment Management, an independent, Sydney-based...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX names built for income

Livewire Markets

Funds

Defensive income with inflation-linked growth

Livewire Markets