High Priced Shares

Earlier this week Macquarie Bank’s share price almost touched $100 after releasing a solid set of profit results and there was speculation in the press that Macquarie Bank would join Cochlear, Blackmores and CSL in having a three-figure share price. In this week’s piece we are going to look at over-valuation and reverse engineering the share price of two high flying stocks on the ASX; Macquarie Bank and A2M milk.

Price versus Value

Historically Australian investors have greatly preferred to invest in companies that have share prices below $10-20. My impression is that this is based on the logic that a 20c move in the share price has a bigger proportional impact, and that investors get more shares in the company when they invest. Fundamentally the actual dollar price per share means very little when deciding whether to buy or sell a stock. The decision is most often made by comparing a stock’s price with the expected profits and, ultimately, the dividends that you can expect as an owner of a fraction of the company. These expected cash flows are then discounted for both their timing and the risk of the company. This analysis derives a valuation that guides an investment decision. A $120 per share company could be much better value than one priced at $12 per share, if the expected dividends discounted for risk and inflation are higher than the price being quoted on the ASX.

Share price momentum

Often when a share price is rising in response to unexpected good news, underlying valuations tend to be ignored and risks glossed over. Analysts at both fund managers and the investment banks (including the author in his younger days) will tweak their valuations to justify why a strong performing stock is still worth buying, thus pushing the price higher.

Additionally, a range of quantitatively managed funds use momentum as a key factor in their investment strategy. Momentum investing is based on the principle that stocks that have been rising (or falling) in the past will continue to do so in the future. This strategy has nothing to do with the fundamentals of a company, but rather with the human propensity to extrapolate trends into the future. Active fund managers can also fall into the momentum trap, as good performance from owning these high flyers attracts inflows from investors that tend to be re-invested in these same stocks, creating a circular loop.

Momentum tends to work well as an investment strategy until it abruptly stops working. Like Icarus flying towards the sun, when these high-flying share prices melt there is often little valuation support.

What does the current share price imply?

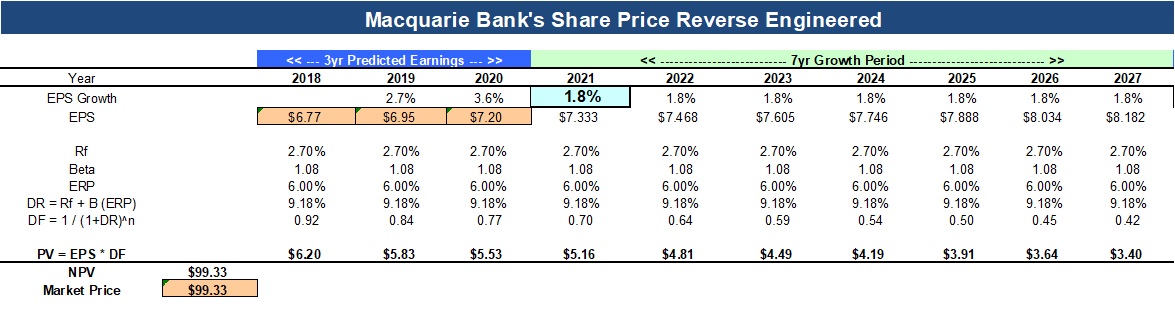

One of the best methods I have used over the years to analyse expensive companies like Macquarie is to back-solve the earnings growth that the current $99-dollar share price implies. In other words, we reverse engineer the share price .

This model uses consensus earnings drawn from sell side analysts’ estimations of company earnings for the next three years. Whilst we recognise that broker earnings are inevitably too optimistic, they provide something of a base estimation of a company’s earnings power. Similarly, we use a terminal growth value of 2.5% in line with the estimated long-term growth rate of the economy.

Logically Macquarie Bank cannot grow towards infinity at 4% if the economy grows at 2.5%, otherwise as a matter of mathematical necessity it will become 99.9% of the Australian economy. Perhaps this would involve consumers buying Silver Doughnut branded cars, breakfast spreads, bread and beer, all funded by a Macquarie Bank mortgage. A chilling thought to most outside of Macquarie Bank’s Beaux-Arts revivalist-style Headquarters in 50 Martin Palace.

The above model suggests that Macquarie Bank’s profit growth needs to maintain a growth rate of just under 2% from 2021 to 2027 to justify the current share price. This is not unfeasible for Macquarie Bank. However, even if it executes well and expands its current A$482 billion assets under management, earnings are likely to be buffeted by external shocks over the next decade.

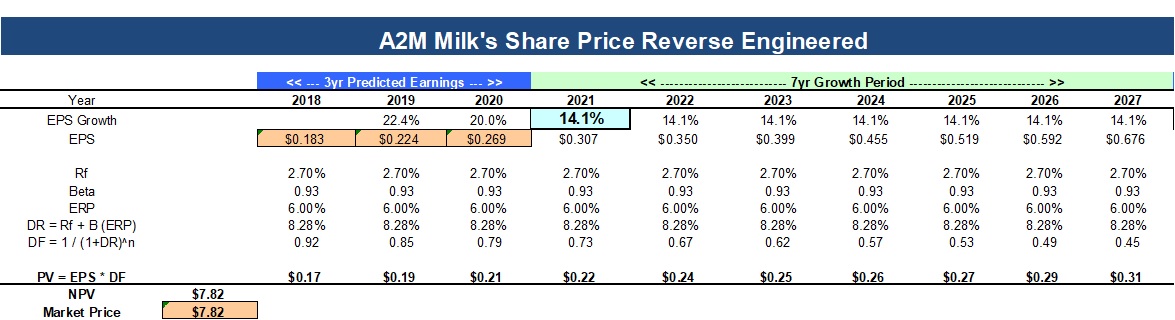

Milk and yogurt company A2M is a favourite holding of many fund managers and its share price is up a staggering 1,542% since listing in 2015. Currently the market sees such upside in the demand for A2M’s milk products that the company is trading on 41 times next year’s earnings per share. A2M is a company with a very solid growth prospects, however using the same model as we used for Macquarie Bank, A2M’s current share price requires a profit growth rate of over 20% for the next three years followed by 14% for the rest of the decade. Whilst it is far easier for a smaller company to achieve these compound growth rates, the current share price does not appear to allow for issues such as Chinese import restrictions or future manufacturing problems.

Our take

The growth implied by the current share price is a good sanity measure for investors. While even the best companies can deliver high earnings growth for a short amount of time, inevitably this growth falters either due to new competitors, management hubris or even the mathematics of compounding growth. Even for the most wonderful company it is becomes progressively harder to grow those earnings at a high compounded rate, as the addressable market for a company’s products is always finite.

The last company to achieve a compounded growth rate of 10% over a 10-year period was Microsoft in the period ending 2004. Here the company benefited from the launch of Windows, Microsoft Office, Windows 95 and the global demand for computers spurred by a desire to access the Internet. Whilst A2M’s milk is gaining market share, it is hard to make the case that it will have as big an impact as Microsoft Excel.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment