Home market bias for fixed income: Not such an irrational idea

Despite some claims that ‘home market biases’ are ‘irrational’, several theories have been put forward to explain the observed bias. For fixed income investors, one theory relating to the management of Real Exchange Rate (‘RER’) risk may assist investors to further optimise their investment outcomes.

Background

The financial literature often refers to the home market biases of investors especially in relation to smaller countries. The home market bias is where investors maintain a disproportionately large allocation to domestic assets versus offshore markets. Such biases are most notable for investors from countries with relatively small financial markets. This bias is sometimes portrayed as misinformed behavioural biases or put more bluntly ‘simply irrational’. There is however the potential for a more rational justification for such a bias when considering the impact of volatility in RERs on investor behaviour.

What is the Objective of Investing?

Often investors view the decision to allocate from domestic to global fixed income securities as a case of gaining additional diversification within their portfolios. Unfortunately, such a perspective risks overlooking the risk that their fixed income investments may not provide protection against domestic inflation. To see why this is important consider that fundamentally the objective of an investor is to generate a return in line with increases in the opportunity cost of foregoing consumption; i.e. domestic inflation. On top of this an additional return premium is required that compensates for the risk associated with the uncertainty of the returns in the actual investment; i.e. risk premium. This is particularly relevant for investors in fixed income securities as the return on such securities is more closely linked to inflation and can in turn be considered as comprising:

Fixed Income Return = Constant Risk Premium + Inflation

As the returns on domestic assets are more closely related to the local inflation cycle, it is reasonable to expect that domestic assets fully cover an investor for local inflation. Therefore, the logical starting point is to initially be fully allocated within domestic assets to provide the requisite protection against domestic inflation.

The next step is deciding on how much to allocate to other offshore asset classes which involves assessing benefits as well as costs. The prime benefit in allocating from domestic to global fixed income is that it increases the level of diversification to both issuers and economic/inflation cycles. But with this additional diversification also comes a potential sting in the tail. As returns in offshore markets are a function of local inflation in their respective economy there is also the increased potential that the investment in offshore fixed income assets may not generate a return sufficient to cover domestic inflation. This risk is most evident in portfolios unhedged for currency exposures as, while theoretically such inflation differentials should be compensated for by changes in the exchange rate via purchasing power parity, in practice this may not always be the case thereby exposing the investor to RER risk; i.e. the risk that exchange rate movements do not fully compensate for inflation differentials between countries.

The same underlying logic applies when dealing with portfolios hedged for currency risk only now the investors need to consider the impact from the interest rate differential; i.e. the ‘forward rate bias’ on the currency hedge. This is particularly relevant for global fixed income as portfolios are normally fully hedged with respect to currency risk.

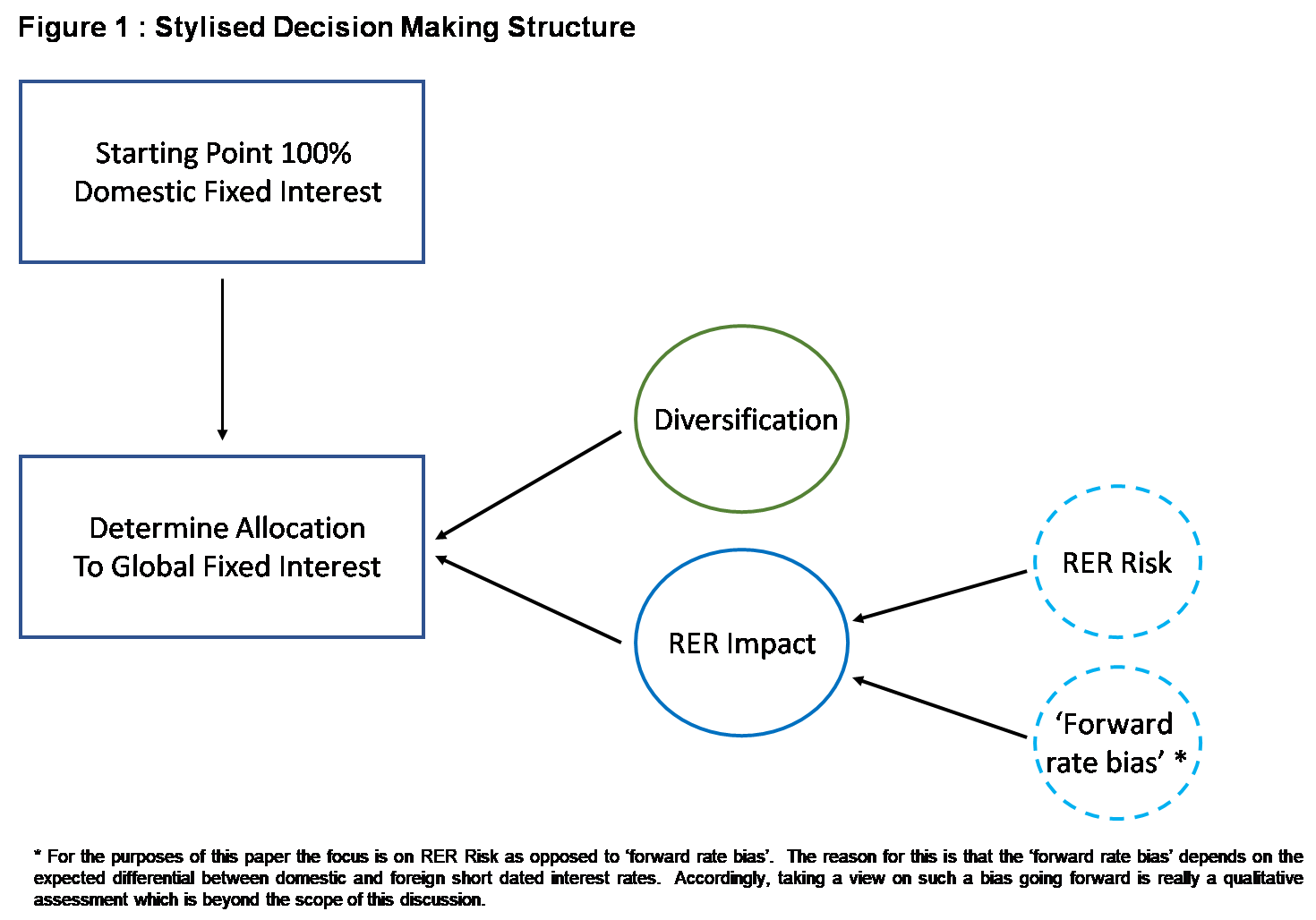

Bringing the return framework and RER risk together implies that in a world where the ‘forward rate bias’ always equals the difference in inflation rates then, all else being equal, an investor will be indifferent to investing in local or offshore markets; i.e. has no home market bias. In practice, unfortunately, the ‘forward rate bias’ does not always offset inflation differentials which can result in a gap between the real returns earned from local and offshore fixed income markets. It is the volatility in the magnitude of these deviations which is the additional risk assumed by investors once they decide to allocate funds from domestic to offshore markets. It follows that within a fully hedged fixed income portfolio the extent to which investors maintain a home market bias will be determined by their sensitivity to the trade-off associated with benefits arising from increased diversification versus and the impact associated with assuming a greater level of RER exposure *. The impact from taking on RER exposure can itself be broken down into risk and return factors or more appropriately higher volatility in real returns associated with RER risk (Risk) and the return from the ‘forward rate bias’ (Return). A stylised schematic of the decision process for an investor is shown in Figure 1:

Is RER Risk Material?

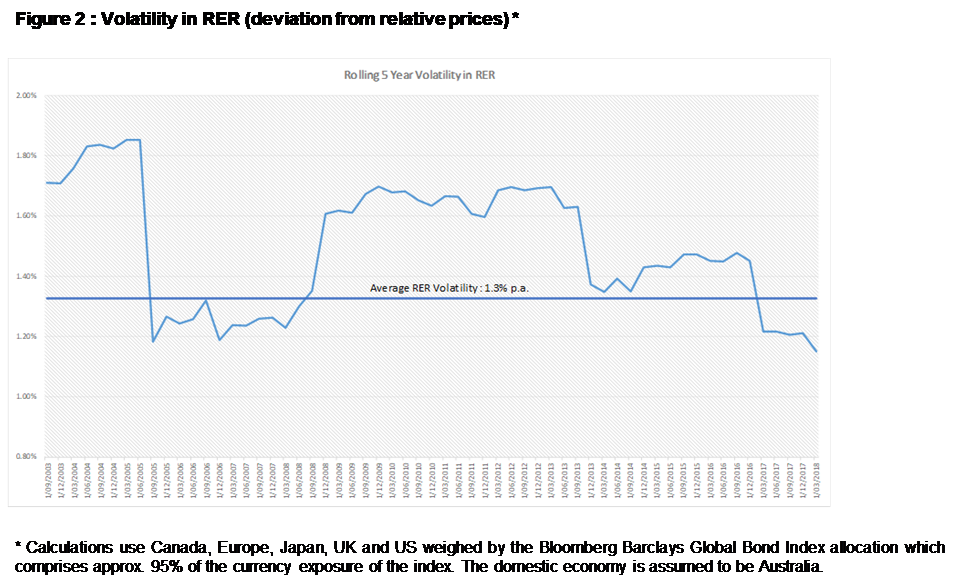

The important point for an investor to assess is the level of risk assumed with respect to RER; i.e. the level of additional volatility resulting from deviations from equality. Taking calculations of interest rate differentials using central bank official cash rates and adjusting for price differences highlights that the volatility in deviations for the AUD have the potential to be quite material.

Overall, for the period from 2003 to 2018 the RER volatility for the weighted average of the major economies versus Australia was around 1.30% p.a. with a rolling 5 year volatility range of 1.80%-1.20%. Whether such levels of volatility are material will of course depend on the perspective of the investor.

Moving Beyond Broad-Based Indices to Portfolio Construction

Several implications follow when assessing whether the potential increase in volatility associated with RER risk is material. The most relevant are that all else being equal, where there is lower volatility in fixed interest returns and/or higher volatility in RER the more material the potential impact. Therefore, the lower the return volatility of a domestic fixed interest investment the stronger the case for a home market bias.

This linkage between the materiality of RER impacts and volatility of the underlying domestic fixed income securities also has implications for optimising portfolio construction. Fixed income markets comprise a wide range of sub classes of assets each of which may exhibit materially different risk characteristics and hence return volatilities. It follows that an investor has the potential to achieve a more optimal outcome by separating such broad-based fixed income allocations into their constituent sub classes based upon return volatility. As return volatility differs between sub classes of fixed income securities this in turn impacts on the materiality of RER volatility and the extent to which it is desirable for an investor to have a home market bias within each fixed income sub class.

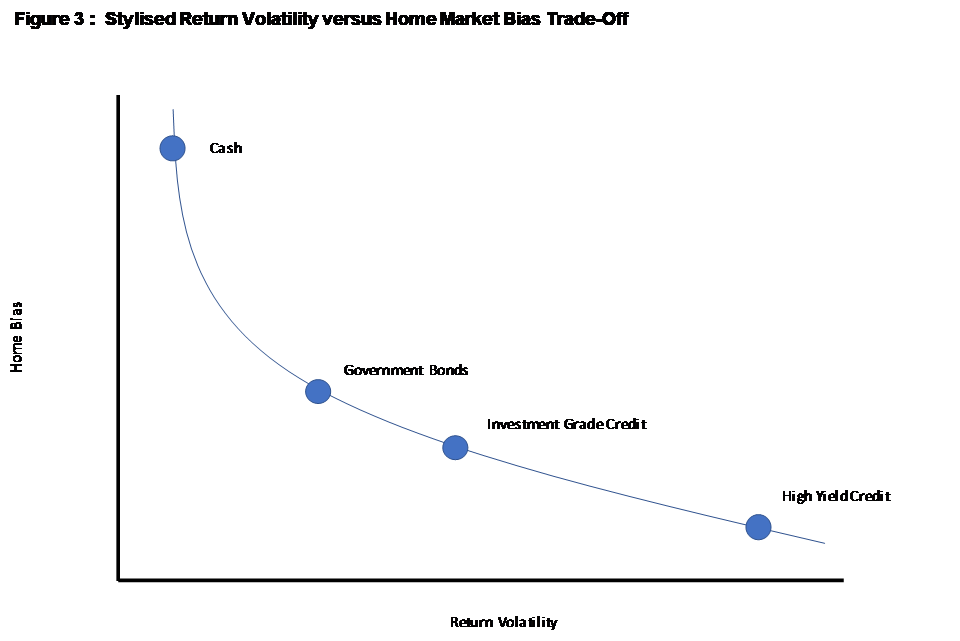

A stylised example of such a decomposition into sub classes based on return volatility is illustrated in Figure 3. The resulting trade-off is that, for any given level of RER volatility, the desirable level of home market bias should differ based on the relative return volatility characteristics of the relevant fixed income sub class.

More Granularity Can Improve Outcomes

Depending on the return volatility of the fixed income sub classes being invested in, a home market bias for bonds may not be such an irrational idea. Within the framework outlined there are still clear advantages from investing globally in terms of increased diversification but the overall case is now less clear cut. The extent to which the advantages of higher diversification will offset any additional volatility associated with RER will now vary between fixed income sub classes. For investors adopting a more granular approach to determine the appropriate level of home market bias within a fixed income portfolio this has the potential to achieve a return outcome more in line with their longer-term objectives.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets