How hard is it to time the market?

In the years since the Global Financial Crisis, the world economy has experienced a significant period of expansion, driven in part by a wave of stimulus from major central banks. As this stimulus is gradually removed and we reach record territory for the length of the economic expansion, at least in the US, it’s hard to argue that the cycle is not maturing.

A key question we hear posed more and more frequently is whether investors should be significantly adjusting their portfolios or whether they should delay investing new money.

This sentiment essentially represents a desire to attempt to pick the peak in the market. Historically, this has proved notoriously difficult to do.

We can turn to history to try and respond to such questions. We look at past market conditions and establish what investors may need to do if they are to effectively time the market and end up with a superior result to a buy-and-hold investor. We find that there is a very narrow window of time to make the market exit and re-entry call, suggesting that market timing, while not impossible, is very difficult. We also highlight additional considerations, such as the time and effort involved, and the emotional repercussions of deviating away from a disciplined strategic asset allocation approach.

Why is it coming up more frequently?

After such a long run of strong market returns, it is only natural that investors’ attention starts to move toward when that run might end, and as each day passes, we move closer to the end of the cycle.

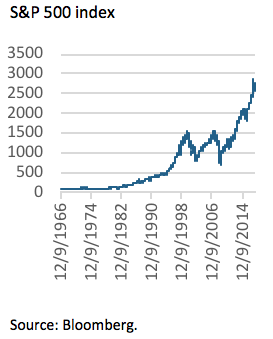

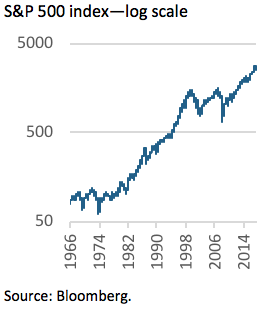

Charts such as the one below left, which shows the performance of the S&P 500 index over the last 30 years, provide a confronting image to many. Are markets in ‘bubble territory’ and set for a correction? However, using a log scale that gives an idea of the rate of growth rather than absolute level (below right) provides a more meaningful and less dramatic picture.

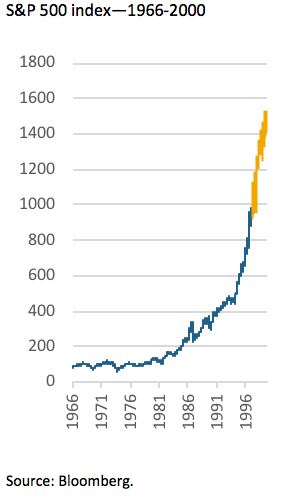

Human nature makes it tempting to look at the S&P 500 index chart opposite and predict the imminent peak of the market. But history reveals that it is actually very difficult to predict this. If we look at the same data in late 1997 (where the blue line terminates on the chart below), we are challenged by a similar situation, and are similarly vulnerable to ‘calling the top’ of the market. Yet, in that instance, an investor who exited at that point would have been too early, missing out on an additional 57% return over the following three years (as the orange line reveals).

The message here is that it’s difficult to predict the future. How an investor behaved through the ensuing dot com bust of the early 2000s would have been equally as important as when they called the top of the market. This is a very important point —timing the market involves making two correct decisions: when to get out and when to get back in again. Getting either decision wrong materially reduces the potential upside from perfectly timing the market, particularly given pre- and post-crash markets are typically very strong.

The key question is, how right does an investor have to be to beat a buy-and-hold investor who stays invested in the market over the long term?

Can it be done?

Various studies have shown that timing the market is not an easy endeavour.

- Recent analysis from UBS (based on the S&P 500 index) found that since 1928, an investor who was able to consistently exit the market 10 months prior to the peak, and then buy back in 10 months after the trough, was no better off than an investor who had simply stayed the course, and that doesn’t factor in trading costs and tax implications.

- These findings were echoed by our own analysis which investigated S&P 500 market corrections over the last 30 years. We found that an accuracy of better than 10 months in every cycle would be required to turn a profit from exiting and re-entering the market.

- Firetrail Managing Director, Patrick Hodgens, also recently noted that (excluding the Global Financial Crisis) there had been 16 other episodes in the past 25 years where Australian equities experienced more than a 7% drawdown. According to Hodgens, although it is lucrative to time exit and re-entry to the day, it is also near impossible. Moreover, being one month early and re-entering one month late delivered the same result as being fully invested during the period.

The idea of exiting the market entirely and re-entering at a (hopefully) more attractive price point is extreme, but dollar cost averaging is another commonly discussed form of market timing. This strategy involves staggering entry in to a particular market over a period of time, rather than investing as soon as the funds are available.

We have compared two investment strategies using Crestone’s growth strategic asset allocation (SAA). The first sees an investor implement his or her entire portfolio on day one, while the second strategy sees an investor implement the portfolio in 12 equal tranches over the course of a year. Using rolling 10-year periods starting in January 1990 and ending in the 10 years to 30 June 2018, we found that, on average, the investor who implemented the portfolio immediately was 0.2% per annum ahead of the investor who employed the dollar cost averaging strategy. Furthermore, the dollar cost averaging strategy was worse off approximately 70% of the time. Similarly, in 2012, Vanguard Investments also found that “on average…a lump sum investing approach has outperformed a dollar cost averaging approach approximately two thirds of the time, even when results are adjusted for the higher volatility of a stock/bond portfolio versus cash investments”.

The above findings are intuitive since investment markets have outperformed cash over time. Assuming an investor expects this trend to continue and is comfortable with their SAA, the most sensible strategy is to be invested as soon as practically possible.

The importance of strategic asset allocation

Timing the market is difficult. And the merits of dollar cost averaging, another form of market timing, are less certain. Further, market timing (in contrast to dynamic tactical asset allocation), stands at odds with one of the most important tools for long-term investors, that being the discipline provided by SAA. In establishing an appropriate SAA, we take a step away from the pitfalls of behavioural investing and are in effect pushed towards maintaining a diversified portfolio that trims profitable positions and tops up the underperformers. In effect, we are buying low and selling high. It also allows the interaction of typically inversely correlated asset classes (such as equities and bonds or alternative assets) to provide the buffer in returns when risk appetite dissipates, and vice versa.

Without this structure, the emotions involved in making buy and sell decisions, particularly at times of market dislocation, are both uncomfortable and also unwelcome, and often lead to sub-optimal portfolio positioning.

In summary

Markets have undoubtedly been on a strong run, with many asset classes delivering positive returns in unison. As a result, we are seeing investors become increasingly nervous that a correction could be imminent and asking whether now is the right time to significantly adjust their portfolios more defensively or delay investing new money. A look at past market corrections suggests that it is very difficult to profit from attempts to time the market. The requirement to pick both the peak and trough with greater than 10-month accuracy every cycle, and an even narrower window once trading costs and tax implications are considered, remains challenging. Dollar cost averaging is another form of market timing, and we again find that an investor has been better placed to be invested as soon as practically possible rather than spread the investment over time. Over the long term, we believe that a disciplined buy and hold approach, provided by an appropriate SAA, will best serve investors looking to achieve optimal risk adjusted returns.

Further Insight

Crestone Wealth Management provides wealth advice and portfolio management services to high-net-worth clients and family offices, not-for-profit organisations and financial institutions. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

Comments

Comments

Sign In or Join Free to comment