TOL - 13th Nov, 2020

How investors can address low real returns on cash

The dramatic drop in cash and term deposit rates this year has been challenging for investors, particularly retirees who depend on regular, reliable income streams. Cash will continue to play a role in portfolios, but the real return on deposit rates is now negative. As we recently noted, with the cash rate at a historical low and below the rate of inflation, allocating to cash may mean losing purchasing power.

Also, in the short-term funding markets for authorized deposit-taking institutions (ADIs), several factors will likely maintain downward pressure on deposit rates over the medium term, most notably the Term Funding Facility (TFF). However, we believe the dynamics of these short-term funding markets are creating real and significant opportunities in high quality bonds and credit markets.

What is the TFF?

The TFF is open to ADIs to access very cheap funding (currently 0.1% p.a.) for a term of three years directly from the Reserve Bank of Australia (RBA). The amount that each ADI can borrow is based on the level of its credit outstanding to Australian households and businesses. The TFF has recently been extended to June 2021 and expanded in size to approximately AUD 200 billion. ADIs have already accessed around AUD 81 billion and have access to a further AUD 120 billion through to mid-2021.

The TFF is a huge expansion of the RBA’s balance sheet and a powerful tool to lower the cost of borrowing and stimulate lending and investment activity to spur growth in the economy.

How is the TFF affecting deposit rates?

By lowering the cost of funding for banks, the RBA intends to foster lower borrowing costs for businesses and lower mortgage rates for households. This is good news if you are a borrower. But in the case of the TFF, what is good for the borrower is not good for the saver.

The TFF means that banks don’t need to rely on customer deposits as they have a cheap and stable funding source. As a result, term deposit rates have fallen and we expect them to fall further given the extension and expansion of the TFF.

In addition, the rise of precautionary savings by households has seen deposit growth spike higher, so the banks are awash with cash and do not need to offer higher rates to attract deposits.

What does this mean for investors?

There are three key implications for investors:

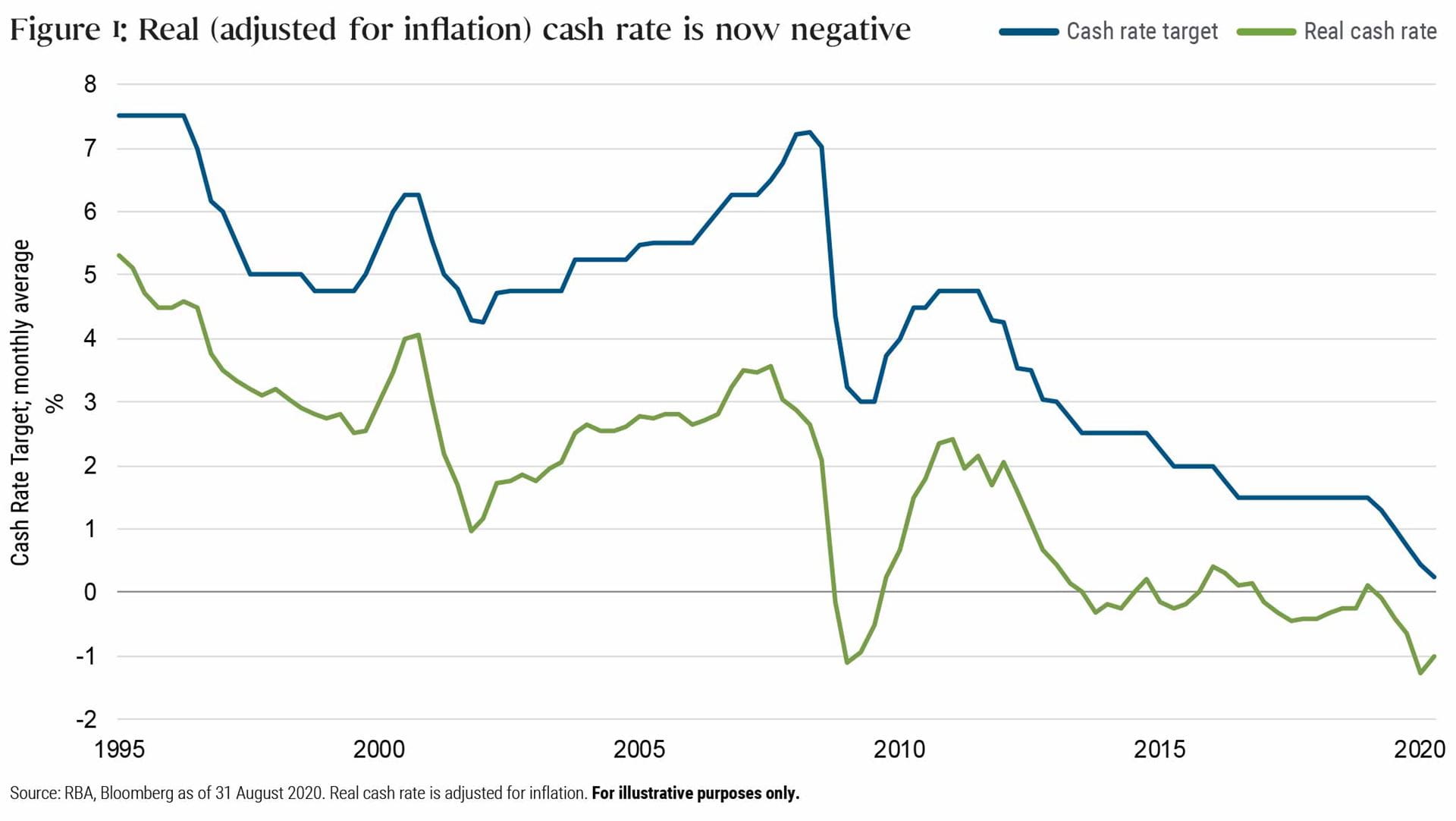

- Negative real cash returns: Deposit and term deposit rates are now well below the rate of inflation, which means cash is losing purchasing power and offers a negative real return (see Figure 1). We don’t envisage that changing, at least not while the TFF remains available to banks and economic growth remains challenged.

- Uplift in the return outlook for quality bank credit exposure: Because the banks can access the cheap TFF funding, they are not issuing much debt. Banks are traditionally a major source of corporate issuance in Australia. Due to the lack of supply of bank paper, credit spreads for banks have fallen dramatically with a corresponding increase in the value of existing bank bonds.

- Uplift in the return outlook for other Australian quality credit: The lack of new issuance by banks is exerting a gravitational pull lower for spreads in other high quality credits due to relative value.

Figure 1: Real (adjusted for inflation) cash rate is now negative

Taking these factors into account, investors may want to reconsider the level of cash exposure they hold in portfolios and potentially allocate more into high quality bonds and credit. These assets offer a potentially greater yield than cash in return for a reasonable uptick in investment risk, as negative real cash rates are driving high levels of demand for bonds and credit. In addition to the RBA providing significant support to bond and credit markets, the large fiscal deficit should underwrite growth over the coming year.

Holding less cash in a portfolio could help investors to preserve purchasing power by earning positive real returns, protect capital via diversification, and produce materially higher levels of income.

Stay protected in times of volatility

We seek to provide all the benefits investors have come to expect from a core bond holding, including consistent income and low volatility, which can help stabilise portfolio returns. Find out more by click 'contact' below, or hit 'follow' to stay up to date with our latest Livewire insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA charterholder.

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA...

Expertise

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA...

Expertise

Comments

Comments

Sign In or Join Free to comment